NRI Income Tax & Compliance

Income Tax E-ProceedingsIncome Tax E-Proceedings

Written by Hatim Dudhiyawala

A UK certificate of residence is an authorized document issued by the HMRC confirming that you are a resident of the UK. Primarily, this certificate is used to avoid double taxation and claim tax relief.

The UK has double taxation treaties (DTTs) with over 157 countries; therefore, a certificate of residence is a non-negotiable requirement to avoid double taxation on the same income.

In this blog, we will discuss the key aspects of the UK certificate of residence (CoR), including its eligibility criteria, benefits for NRIs living in the UK, the application process, processing time, and other compliance requirements.

As aforementioned, CoR is an official document issued by HM Revenue & Customs, the UK's tax authority. This certificate serves as proof that the holder, whether an individual or a company, is based in the United Kingdom for tax purposes. In a nutshell, CoR also acts as your tax residency certificate.

CoR is primarily used to avoid double taxation and to claim tax exemptions or reliefs on income earned in India. This document is mandatory for NRIs living in the UK and being tax residents there who also earn revenue from India. The certificate proves that they are obliged to pay taxes in the United Kingdom. This acknowledgment prevents double taxation of the same income source.

Please ensure that CoR is not mandatory for all Non-Resident Indian (NRIs). It is only needed if you are claiming benefits of double taxation treaties in Indian Income. Having the CoR alone does not prevent double taxation. You must also meet the DTAA conditions set in India and file all the required forms as an NRI, such as Form 10F and TRC.

There are several reasons why a UK tax residence certificate from HMRC is important for NRIs.

To Avoid Double Taxation: The primary benefit of having a UK certificate of residency is the ability to use the DTAA tax treaty provisions. This ensures that income earned in one country is not taxed in another.

To Claim Tax Benefits in India: As per the Income Tax Act of 1961, a tax residency certificate (CoR) is mandatory to claim any benefits, tax rates, or relief under a DTAA on income earned in India.

Lower withholding tax (TDS) rates: If an NRI does not have a certificate of residency, then he/she will be subject to higher TDS rates. However, with a valid Indian residency certificate, NRIs can claim lower TDS rates as mandated by the India-UK Double Taxation Avoidance Agreement.

Fund Repatriation: Many Indian banks often require a tax residency certificate to process the repatriation of funds, such as the proceeds from the sale of property in your NRO account to the UK. Having a tax residency certificate simplifies the entire process and ensures compliance.

To get a UK Certificate of Tax Residency, you need to meet certain rules set by HMRC. Such rules are:

Please note that the HMRC will not issue the CoR if you did not meet the tax treatment benefits.

Non-resident Indians living in the United Kingdom can apply for a Certificate of Residency through the HMRC's online portal or by post.

Please note that HMRC may ask you for clarification, such as proof of address. Hence, please respond to such requests promptly, as any delay will prolong your processing time.

As an NRI, to get a tax residence certificate or certificate of residence from the UK, please keep the following documents in order.

The processing time of the UK certificate of residency is as follows.

Online Application: The processing time for online applications is generally four to six weeks, given that all the documents you have provided are correct.

Postal Application: The processing time for a postal application is generally around 6 to 8 weeks (plus additional time that might be expected from the postal service).

Complex Cases: Companies with sophisticated structures or dual registration holders may take around eight to twelve weeks to process.

Hence, to avoid all last-minute complications, please apply well in advance.

Generally, a certificate of residence is valid for a financial year from the date of issue. HMRC cannot provide you with a CoR for the future period.

Hence, you will have to apply for a certificate of residence every year if you are eligible under DTAA.

With the help of CoR, Non-resident Indians can reduce the tax liability on different types of Income earned in India. Such income can be

The DTAA treaty benefits apply to different types of taxes in both countries.

So, the taxes in the United Kingdom under DTAA are:

Taxes under the Indian Tax Category Are:

Apart from these taxes, other taxes are either the same or similar types included in the DTAA.

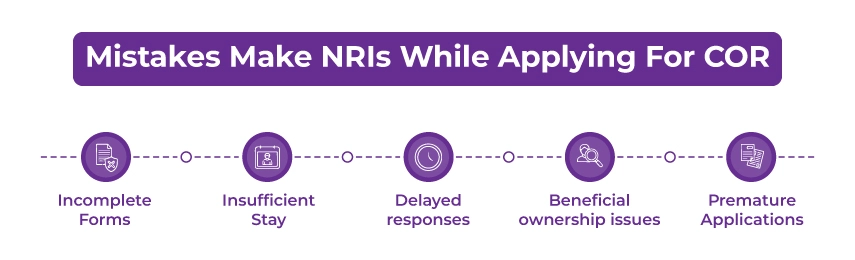

Here is a list of a few common mistakes that NRIs make, which you must avoid if you don't want to delay the processing time of your certificate of residency.

As a non-resident Indian (NRI) earning income in India and wanting to claim the Double Taxation Avoidance Agreement (DTAA) benefits, you must first submit your UK certificate of Residence to the Indian tax authorities along with the required documents.

Here is a step-by-step process for doing it.

Step 1: Get a certificate of residence from the HMRC. Please ensure that the Cor should clearly method the following details.

Step 2: Get a Form 10F. Download Form 10F from the Incoe tax e-filing portal. And fill in all the requested details, such as his name, address, nationality, TIN, residential status period, and more.

Step 3: Provide Certificate of Residence and Form 10F to the Indian Payer. Meaning that you must submit both Form 10F and CoR to the entity that receives your income in India, such as a bank or employer, or the buyer.

Doing so allows the payer to deduct TDS at DTAA rates rather than the higher standard rates.

Step 4: Submit CoR to the Indian Tax Department. Whenever you're filing your income tax return in India, attach Form 10F and a Copy of the certificate of Residence to it.

The UK Certificate of Science is important for UK residents involved in international tax matters. This certification ensures that you avoid duplicate taxation easily and can manage your business operations in India smoothly.

The CoR for NRI is also known as the NRI tax residency certificate in the UK. Please ensure this document is mandatory for NRIs in the UK seeking to claim tax treaty benefits under the India-UK DTAA.

By utilizing Savetaxs high-end, expert-backed services, you can ensure an easy, secure UK Certificate for the tax-residence application process.

Our experts bring more than 30 years of experience in NRI taxation and cross-border tax planning, so you can be assured that we provide each client with a tailored approach to their taxation needs.

The experts will provide end-to-end guidance on how to apply for the UK certificate of residency efficiently and then claim benefits under the India-UK DTAA.

Connect with Savetaxs today—we serve our clients 24/7 across all time zones.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Shubham Jain is the Founder of SaveTaxs and has extensive experience in Indian and NRI taxation. He advises individuals, NRIs, and businesses on tax filing, tax planning, capital gains, DTAA benefits, fund repatriation, and compliance matters. He regularly writes about taxation and related financial topics. His focus is on making complex tax concepts easy to understand. Through his articles, he helps taxpayers stay informed, avoid common mistakes, and stay compliant with Indian tax laws. See Full Bio

Want to read more? Explore Blogs

_1782475363401.webp&w=828&q=75)

The UK certificate of Residence is an official document issued by the HMRC that confirms an individual or a business as a tax resident of the United Kingdom.

It is important for NRIs who earned income in India that a UK CoR is mandatory to claim benefits under the India-UK Double Tax Avoidance Agreement.