Investment & Financial Planning

FCNR Deposit Interest Rates in 2026FCNR Deposit Interest Rates in 2026

Written by Hatim Dudhiyawala

Sending money to India from any foreign country can be a task for most NRIs. There are so many methods, and each method has its own pros and cons. Different options and a lack of knowledge make the remittance process very complicated for them.

In this article, we will explore the various methods for remitting money to India and help you find the best way to send money to India. We have also mentioned the RBI and FEMA guidelines, as well as the documents you may require, so you can comply with the process.

There are many reasons why the foreign nationals, Non-Resident Indians (NRIs), Overseas Citizens of India (OCIs), and Persons of Indian Origin (PIOs) send money to India. These reasons can be family maintenance, investment purposes, or self-transfers to their own Indian account for saving. The process of sending money from a foreign country to India is known as an Inward Remittance.

There are various options by which the NRIs can send money to India:

Many banks and fintech companies offer platforms for instant fund transfers worldwide. You can easily transfer money to the recipient bank that provides these services. Account holders at all banks can use these digital platforms.

An international money order is a money transfer service offered by the Indian Postal Network. It is an easy and reliable way to send and receive money across borders. The recipient can redeem the money order at cheque-cashing facilities or deposit it into their bank account.

The NPCI (National Payments Corporation of India) and NIPL (NPCI International Payments Limited) now offer international payments by using the Cross-border UPI. The NRIs can use these facilities to send money to India. Currently, it is available in the India-Singapore corridor and is soon to be expanded to other countries. NRIs can send money to any Indian bank account or UPI, which a local remittance service provider handles.

We file Income Tax Returns for NRIs with 100% accuracy.

An NRI can send FCC/FCDD from an overseas bank in India to an Indian recipient. The beneficiary can deposit FCC/FCDD into their account or take it to the bank and receive the remittance. There may be service changes applicable at the time of the FCDD enhancement. These charges can vary for different banks depending on the amount of the transfer.

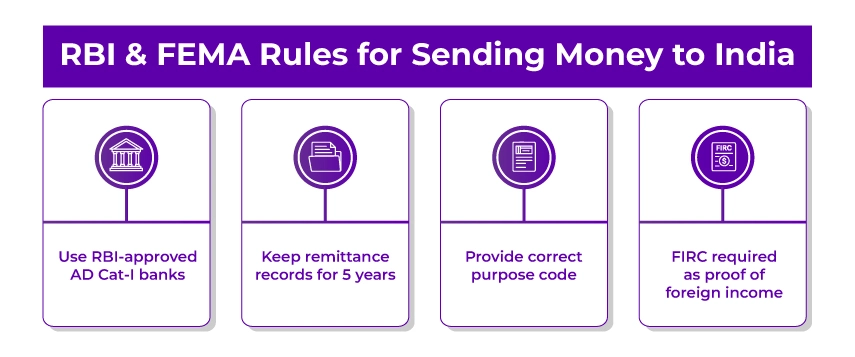

Here are the most important guidelines that come under the FEMA rules for foreign transfer:

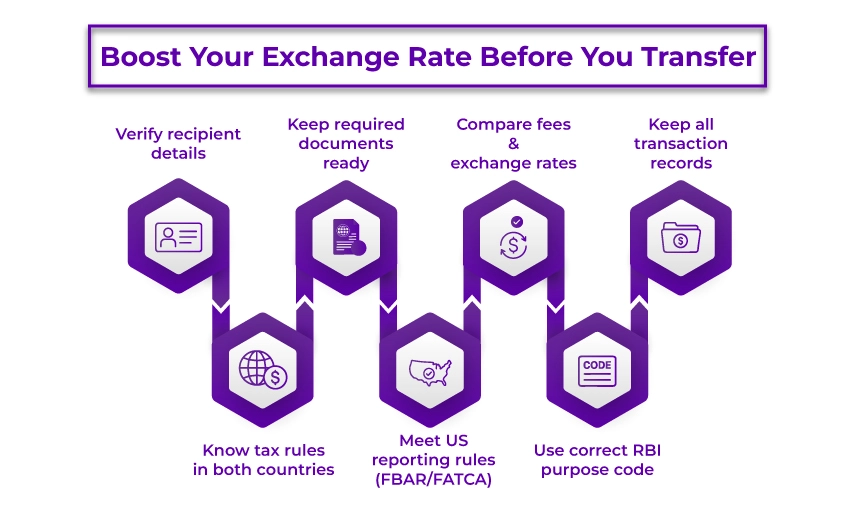

To get the best exchange rates, it is important to properly prepare before sending money to India. It will help in avoiding delays and complications. Here is the list of things that you need to verify and prepare:

The remitter must submit these documents to the authorised service provider or to their overseas bank. Here is the list of all the documents required for an inward remittance.

Get accurate ITRs filed and carry forward your losses by consulting our experts.

For NRIs, the amount they send to India is not taxable. However, there will be tax implications for the recipient who is a resident of India. Taxation will depend on the purpose of the amount transfer, such as:

NOTE: There may be Standard Goods and Services Tax (GST) applied to the service charges (not on the transferred amount), which are payable on remittances.

There are various options by which the NRIs/PIOs/OCIs and foreign nationals can send money to India. These methods are wire transfers, money transfer services, cross-border UPI, IMO, and FCC/FCDD. You can choose your preferred method as per your needs, depending on cost, speed, and comfort. There will be tax implications for the Indian recipient of money. You should also comply with the FEMA guidelines and notify your authorised dealer/bank about the transfers.

Furthermore, if you find this process complicated, getting expert assistance is the best solution. Savetaxs is one such platform for NRI taxation. We have a team of professionals with years of experience to help you feel confident about the tax implications of sending money to India.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Shubham Jain is the Founder of SaveTaxs and has extensive experience in Indian and NRI taxation. He advises individuals, NRIs, and businesses on tax filing, tax planning, capital gains, DTAA benefits, fund repatriation, and compliance matters. He regularly writes about taxation and related financial topics. His focus is on making complex tax concepts easy to understand. Through his articles, he helps taxpayers stay informed, avoid common mistakes, and stay compliant with Indian tax laws. See Full Bio

Want to read more? Explore Blogs

_1781845771869.webp&w=828&q=75)

_1778936280179.webp&w=828&q=75)

_1778936089630.webp&w=828&q=75)