Section 195 of Income Tax Act - TDS Applicability for NRI

Read More

Section 194I mandates the deduction of tax on rent payments. The applicable TDS rate is 2% for rent paid towards the use of plant, machinery, or equipment, and 10% for rent paid for the use of land, buildings, furniture, or fittings.

TDS must be deducted when the total rent paid during a financial year exceeds Rs. 2,40,000, which is the current threshold limit under Section 194I of the Income Tax Act.

The provisions of this section apply to individuals and HUFs only if they were liable for tax audit in the preceding financial year, meaning their business turnover exceeded Rs. 1 crore or professional receipts exceeded Rs. 50 lakhs.

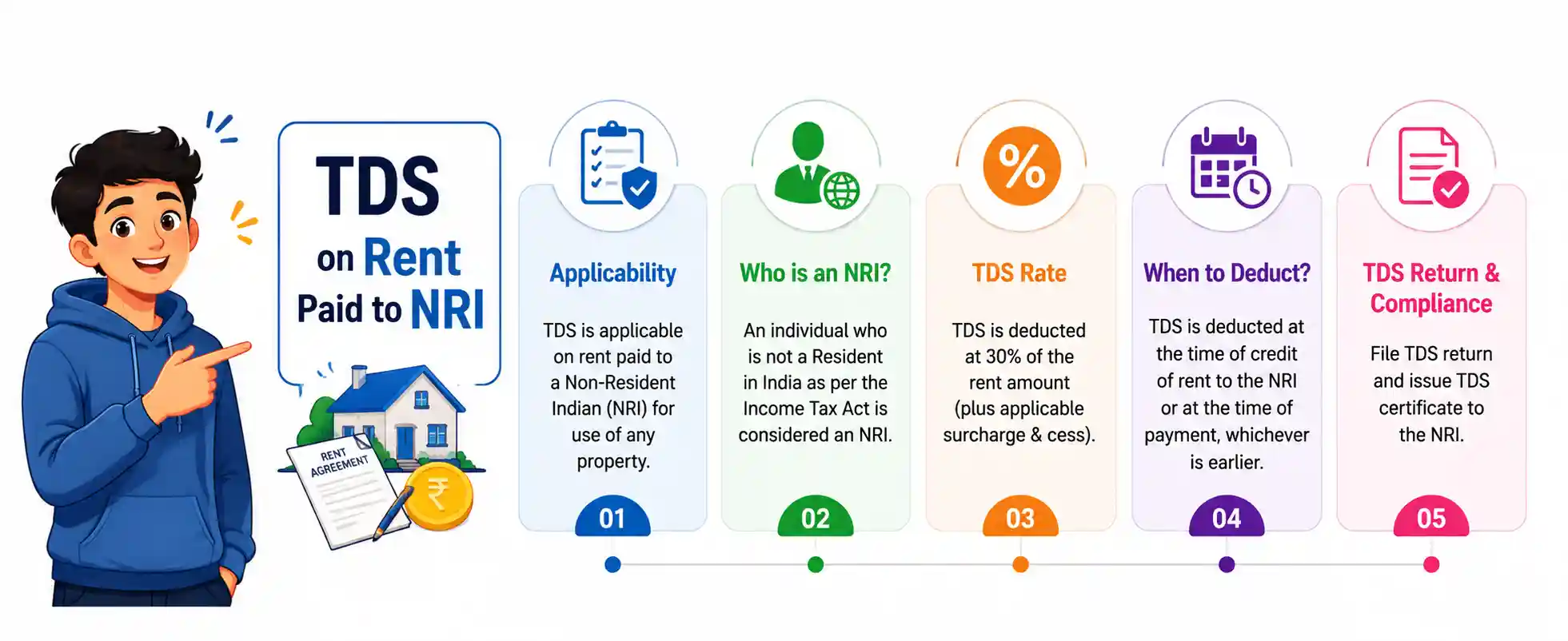

When rent is paid to a Non-Resident Indian (NRI), TDS is deducted under Section 195 instead of Section 194I. In such cases, TDS is generally deducted at 30% plus applicable surcharge and cess, subject to DTAA benefits. Unlike Section 194I, there is no minimum threshold limit for rent paid to an NRI landlord.

Let’s understand Section 194I in detail.

Section 194I of the Income Tax Act requires the deduction of Tax Deducted at Source (TDS) on rent payments. The section applies to rent paid for the use of:

Plant

Machinery

Equipment

Land

Buildings (including factory buildings)

Furniture and fittings

The applicable TDS rates are:

2% for plant, machinery, or equipment

10% for land, building, furniture, or fittings

TDS under Section 194I becomes applicable when the total annual rent paid exceeds Rs. 2,40,000 during the financial year.

The provisions of Section 194I apply to individuals and HUFs only if they were subject to tax audit in the immediately preceding financial year.

Individuals and HUFs not covered under tax audit provisions are generally required to deduct TDS under Section 194IB at 5% if the monthly rent exceeds Rs. 50,000.

Similarly, when rent is paid to an NRI landlord, TDS provisions under Section 195 become applicable instead of Section 194I. In such cases, TDS must be deducted at 30% plus surcharge and cess, subject to DTAA relief.

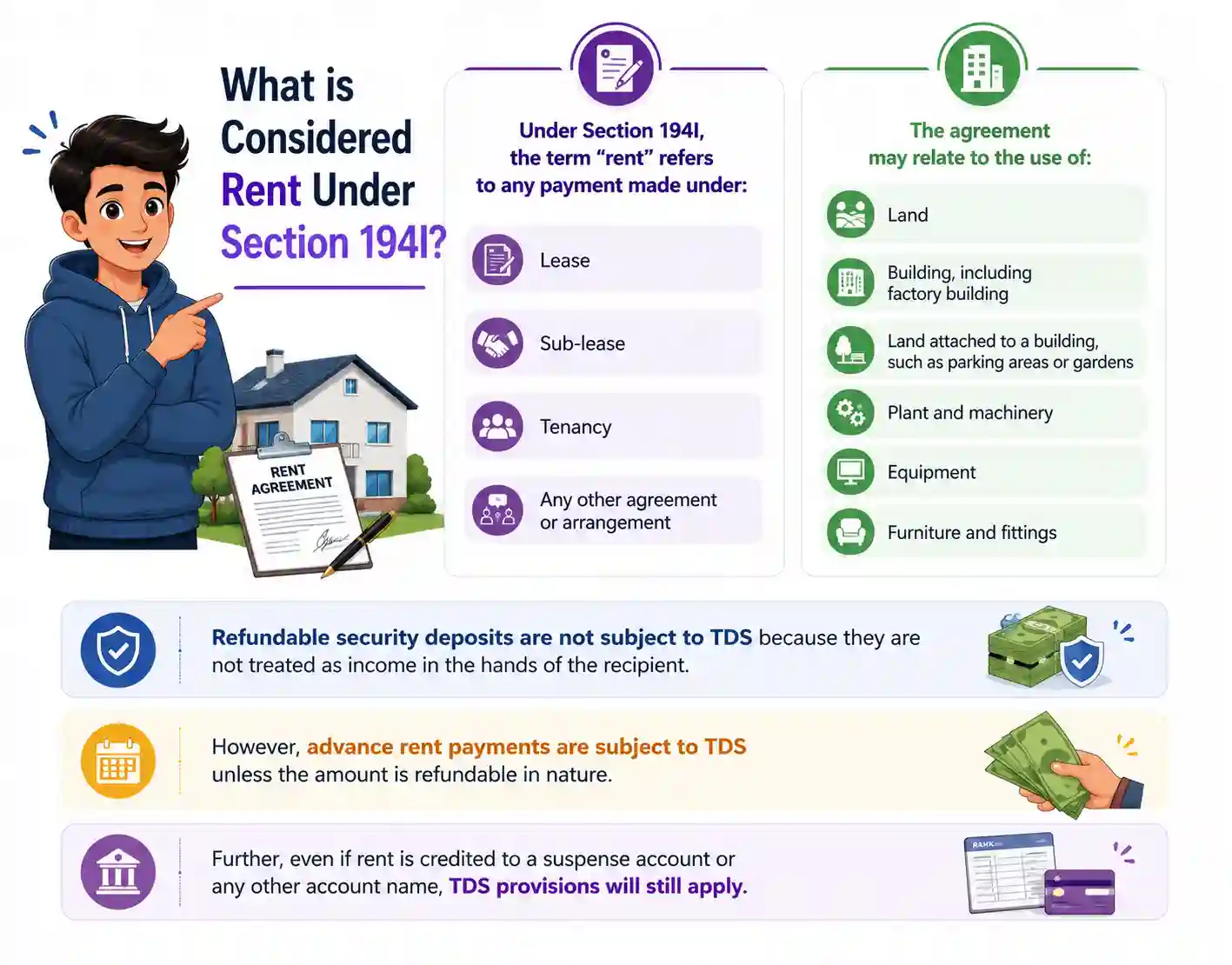

Under Section 194I, the term “rent” refers to any payment made under:

Lease

Sub-lease

Tenancy

Any other agreement or arrangement

The agreement may relate to the use of:

Land

Building, including factory building

Land attached to a building, such as parking areas or gardens

Plant and machinery

Equipment

Furniture and fittings

Refundable security deposits are not subject to TDS because they are not treated as income in the hands of the recipient.

However, advance rent payments are subject to TDS unless the amount is refundable in nature.

Further, even if rent is credited to a suspense account or any other account name, TDS provisions will still apply.

TDS under Section 194I must be deducted by:

Companies

Partnership firms

LLPs

Individuals and HUFs covered under tax audit provisions

The obligation to deduct TDS arises only when the annual rent exceeds Rs. 2,40,000.

Individuals and HUFs not liable for tax audit are generally covered under Section 194IB instead of Section 194I.

TDS must be deducted at the earlier of the following events:

At the time of crediting rent to the payee’s account

At the time of making payment

This means even if the rent is unpaid but credited in the books of accounts, TDS liability may still arise.

No TDS is required under Section 194I if the total rent paid or payable during the financial year does not exceed Rs. 2,40,000.

Once the threshold limit is crossed, TDS becomes applicable on the rent payment as prescribed under the Act.

| Rent Type | TDS Rate |

|---|---|

| Plant, Machinery & Equipment | 2% |

| Land, Building, Furniture & Fittings | 10% |

No surcharge or cess is added to TDS rates under Section 194I for resident payments.

If the landlord does not furnish PAN, TDS may be deducted at 20% under Section 206AA.

When rent is paid to an NRI landlord, Section 195 applies instead of Section 194I.

The following provisions generally apply:

TDS rate: 30% plus surcharge and 4% cess

No minimum threshold limit

DTAA benefits may be available

TAN registration may be required

Form 15CA and Form 15CB compliance may apply in certain cases

Since NRI taxation involves additional compliance requirements, professional assistance is often advisable to avoid penalties or incorrect tax deductions.

Payer: XYZ Pvt. Ltd.

Receiver: Mr. Arjun (Resident Landlord)

Monthly Rent: Rs. 75,000

Since the annual rent exceeds Rs. 2,40,000, XYZ Pvt. Ltd. must deduct TDS under Section 194I.

Annual Rent = Rs. 75,000 × 12 = Rs. 9,00,000

Applicable TDS Rate = 10%

Monthly TDS = Rs. 7,500

Net Rent Paid = Rs. 67,500 per month

TDS under Section 194I may not apply in the following situations:

The tenant is an individual or HUF not covered under tax audit provisions

The payment is covered under Section 194IB instead

Payments between film distributors and exhibitors where there is no renting arrangement for premises

Refundable security deposits paid to the landlord

The recipient of rent income may apply for lower or nil TDS deduction under Section 197 by filing Form 13 before the Assessing Officer.

If the Assessing Officer is satisfied that lower deduction is justified, a certificate may be issued authorizing deduction at a reduced rate or no deduction.

The TDS deducted under Section 194I must generally be deposited within 7 days from the end of the month in which deduction is made.

Due Dates

For deductions made in March: on or before 30th April

For deductions made in other months: within 7 days from the end of the relevant month

Additionally, quarterly TDS returns must also be filed within the prescribed due dates.

Failure to deduct or deposit TDS can result in interest, penalties, and disallowance of expenses.

1% per month from the date on which TDS was deductible until the date it is actually deducted

1.5% per month from the date of deduction until the date of deposit

Income from Letting Out Factory Building: Rent received from factory buildings may sometimes be treated as business income in the hands of the owner. However, TDS under Section 194I may still apply on such payments.

Service Charges Included with Rent: Service charges paid to business centers are generally treated as rent if they are connected with the use of premises or facilities.

Separate Letting of Building and Furniture: Where the building and furniture are rented by different owners, TDS must be deducted separately for each payment made to the respective owners.

Rent Paid Quarterly or Annually: Section 194I does not require rent payments to be monthly. If rent is paid quarterly or annually, TDS should be deducted accordingly at the time of credit or payment.

Cold Storage Facility Charges: Payments made for cold storage facilities may sometimes fall under Section 194C instead of Section 194I, depending on the nature of the contractual arrangement.

Hall Rent Paid by Associations: Associations and entities paying hall rent may also be liable to deduct TDS if the payment exceeds the prescribed threshold limit.

Payments to Hotels for Seminars: Where hotel bills include catering and hall charges together

Catering portion may fall under Section 194C

Hall or premises usage may fall under Section 194I

Advance rent payments are also subject to TDS deduction. However, certain exceptions may apply.

If advance rent relates to multiple financial years, TDS may be proportionately considered.

If the rental agreement gets cancelled later, appropriate adjustments may be required in the tax return.

Form 16A should be issued quarterly for TDS deducted on non-salary payments.

| Particulars | Section 194I | Section 194IB |

|---|---|---|

| Applicable To | Businesses, firms, companies, tax audit cases | Individuals/HUFs not under tax audit |

| Threshold Limit | Rs. 2,40,000 annually | Rs. 50,000 monthly rent |

| TDS Rate | 2% or 10% | 5% |

| TAN Requirement | Required | Not mandatory in certain cases |

Section 194I plays an important role in ensuring tax compliance on rent payments. Businesses, companies, and individuals covered under tax audit provisions must carefully determine whether TDS is applicable based on the type of rent payment, threshold limit, and status of the landlord.

Incorrect deduction, late payment, or non-compliance can lead to penalties, interest, and additional scrutiny from the Income Tax Department.

Further, transactions involving NRI landlords require special attention since TDS provisions under Section 195, DTAA applicability, and additional compliance requirements may also arise.

Understanding these provisions properly can help taxpayers avoid costly compliance errors and ensure smooth tax reporting.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Mr. Ritesh has 20 years of experience in taxation, accounting, business planning, organizational structuring, international trade financing, acquisitions, legal and secretarial services, MIS development, and a host of other areas. Mr Jain is a powerhouse of all things taxation.

Want to read more? Explore Blogs