_1779454749573.webp&w=828&q=75)

NRI Returning to India

Managing Money Before Returning to IndiaManaging Money Before Returning to India

Written by Hatim Dudhiyawala

For decades, the United States (US) has been a top destination for Indians who are seeking higher education, global expansion, and career growth. However, in recent years, many NRIs have decided to return to India. It can be due to any reason, be it emotional, financial, or professional.

Relocating to India from the USA is far more than just buying a plane ticket. You need to handle several things, including tax residency, banking conversions, investment management, fund transfers, and documentation updates.

Taking care of everything carefully while moving back to India from USA is essential to ensure an efficient transition. In this guide, we will walk you through every major aspect of your return that an NRI must consider so that they can plan their move confidently.

The reason behind NRIs planning to migrate from the USA to India may differ widely. Some of them return to be close to their family, while others return to explore India's fast-growing economy, job market, and entrepreneurial landscape.

Here are some of the common reasons that motivate NRIs in the US to move back to India:

Every NRI has a unique story for returning to India; however, what remains common is the importance of financial and legal planning to avoid any surprises in the future.

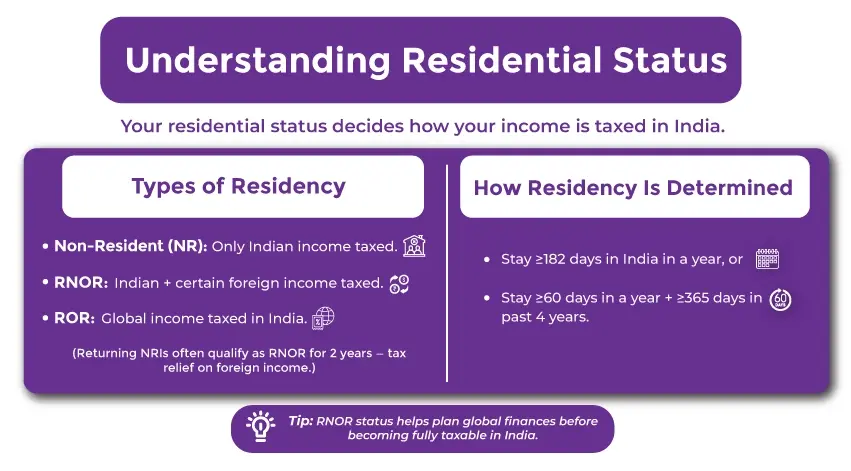

Your residential status in India is the basis for determining how your income (from both India and overseas) will be taxed upon your return to India.

Under the Income Tax Act, an individual is classified as:

Most NRIs returning from the USA qualify as RNOR for up to 2 financial years, providing them with temporary relief from taxation on foreign income.

You will be considered a resident in India if:

The RNOR status in India serves as a transitional phase for those who are moving back to India after spending years in the US. This status will help you restructure your global finances before becoming fully taxable in India.

One of the trickiest parts of returning to India is managing your taxes. The US and India both impose tax on global income. However, the DTAA between the two nations ensures that you don't pay taxes twice on the same income.

Get assistance with a wide range of services tailored to meet the needs of NRIs.

The India-US Double Tax Avoidance Agreement prevents you from being taxed twice. Under this agreement:

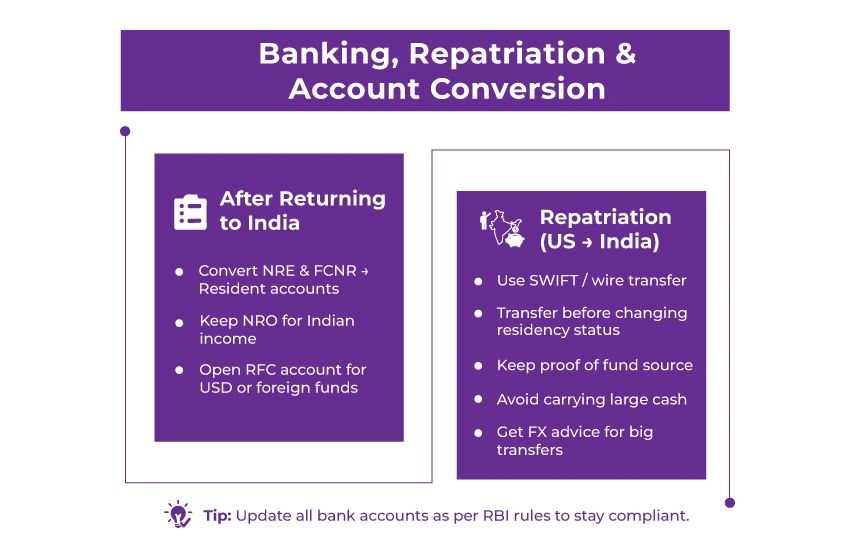

You must update your bank account status in accordance with RBI (Reserve Bank of India) regulations after you permanently move back to India.

Once you become a resident:

RFC accounts are specifically useful for those who might receive income or visit the US again in the future.

Repatriation is the legal transfer of your US funds to India. Here is how you can do it easily:

Consider seeking guidance from a financial advisor for foreign exchange if you plan to transfer large funds.

Returning NRIs might have assets in both India and the United States. It can include properties, retirement accounts, and stock market investments. To avoid penalties and ensure compliance, you need to handle these accounts accurately:

If you own a property in the US, you can:

Make sure to keep records of property transactions, mortgage closures, and tax filings to report the income accurately.

Numerous NRIs hold 401 (k) or IRA accounts, so here is what they need to know:

Explore India's growing investment landscape after you settle back in India:

Ensure to update all your investments in PAN, Aadhar, and KYC records after a change in your residency status

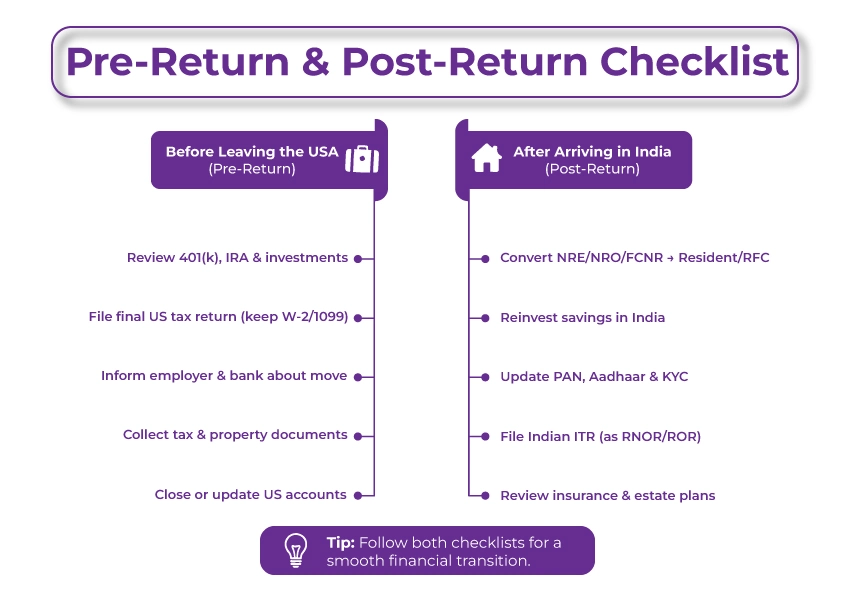

Consider these pre-return and post-return checklists to ensure accuracy and compliance before leaving the US and after arriving in India:

Consider this checklist and do everything accordingly to ensure that every aspect of your financial and legal transition is handled in a systematic manner.

Although returning to India from the USA can be exciting, NRIs might often face several challenges, including:

Avoid being stuck on taxes and confused about investments. Contact our experts right away and simplify your tax and financial issues.

The transition from the USA to India marks an essential personal and financial milestone. It can be made easier with proper planning, tax understanding, and regulatory compliance. Ensure to update your banking and investments, transfer funds through official channels, and plan your taxes carefully.

A well-planned return to India allows you to focus on what's really important. Furthermore, seeking expert assistance from Savetaxs can eliminate most of the challenges and make this transition easy.

At Savetaxs, we have a team of experts dedicated to assisting NRIs with their tax obligations and financial planning. They will ensure you stay compliant and well-prepared with everything when moving back to India from the USA and starting a new chapter back home. So, contact our team anytime, as we are actively working 24*7 across all time zones.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Shubham Jain is the Founder of SaveTaxs and has extensive experience in Indian and NRI taxation. He advises individuals, NRIs, and businesses on tax filing, tax planning, capital gains, DTAA benefits, fund repatriation, and compliance matters. He regularly writes about taxation and related financial topics. His focus is on making complex tax concepts easy to understand. Through his articles, he helps taxpayers stay informed, avoid common mistakes, and stay compliant with Indian tax laws. See Full Bio

Want to read more? Explore Blogs

_1778504462654.webp&w=828&q=75)

_1777726294138.webp&w=828&q=75)

_1771668297202.webp&w=828&q=75)