Investment & Financial Planning

FCNR Deposit Interest Rates in 2026FCNR Deposit Interest Rates in 2026

Written by Hatim Dudhiyawala

Asset allocation for NRIs involves dividing their investments across various asset classes, such as stocks, bonds, cash, and real estate, strategically to balance risk and reward. This process becomes more complex for NRIs as compared to Indian residents due to the financial considerations involved in managing wealth across borders.

While residents face a single tax system and currency, NRIs must navigate global income, fluctuating foreign exchange rates, diverse regulations, and tax obligations in both India and their resident country. Factors like repatriation rules, investment restrictions, and compliance requirements, such as FATCA, also impact their investment asset allocation.

It is important to find the right balance between Indian and international investments to reduce risk, manage market volatility, and achieve long-term financial stability. Keep reading the blog to know more about how to plan a thoughtful asset allocation investment strategy that supports wealth creation, retirement planning, and maintains connections with India while complying with global regulations.

An NRI is allowed to invest a minimum of 5 to 10% of their income in India. However, the problem here is that how much you invest will be determined based on various factors, like whether you plan to return to India or wish to stay in your country of residence.

You must gradually increase your allocation to Indian assets to prepare for eventual retirement in India. This investment strategy required dynamic asset allocation adjustments as you approach your planned retirement date. Try to focus on high-return equities at first, and after that, prioritize protecting capital and steady income when you get close to retirement.

Investing in Indian markets can be an ideal way to diversify your portfolio across borders if you plan to retire outside India. For diversification and scope for growth, hold 20 to 40% in Indian assets.

Additionally, remember that NRIs from the UK and the Gulf have the option to allocate a significant portion of nearly 20 - 30 % for UK and 40 -50% Gulf to Indian investments. The suggested allocation may vary depending on your country of residence.

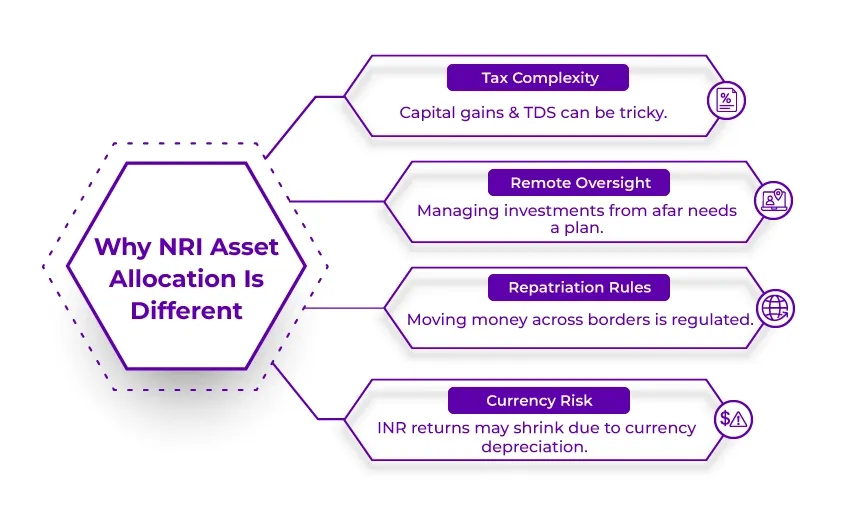

An NRI is liable to manage wealth across two economies that have different currencies, growth cycles, and tax structures. The main challenges faced by NRIs are:

The timeline of your investment significantly impacts your allocation strategy. Here is how it matters:

More than 10 Years to Return

Nearly 5-10 Years to Return

More than 5 Years to Return

Point to Remember: The timeline of your return will significantly impact your asset allocation, be it in 10 years or 5 years. It is important to balance risk and diversify.

Achieve your Indian financial goals with expert investment, insurance, and tax advice.

This builds a lot of confusion amongst NRIs. Remember that you can't avoid currency risk, but you can manage it by accepting it as a part of investment in India.

Indian rupee depreciation is offset by higher Indian GDP growth and mutual fund returns over the decades. Try to diversify across currencies.

Avoid putting 100% of your wealth in INR-denominated assets. Hedge with GIFT City Investments.

To understand it easily, let's consider a real example. Diversified NRIs lost nearly 5-8%, while INR-concentrated portfolios dropped 15-10% during the rupee crisis that occurred in 2013.

Here are some of the Indian assets that you can access to build your NRI portfolio:

Wasted thousands by paying double tax for two years? This mistake highlights why tax planning must involve allocation decisions:

Ensure to check the benefits of the DTAA treaty with your country to improve tax treatment across all asset classes.

The following is a list of some common asset allocation mistakes, along with advice on how to prevent them:

A portfolio that holds an excessively large proportion of assets with returns under the prevailing inflation rate, like cash, risks an effective decline in purchasing power over time. To fight inflation, try adding assets with the potential for larger returns, like stocks and real estate.

Asset allocation in your portfolio might naturally shift from your initial strategy because of market movements. For example, when your stocks perform well, their value can grow to be a much larger portion of your total investments than you originally intended. This shift means that your overall investment risk goes up as more of your money is tied to the performance of those specific stocks.

Try to rebalance your portfolio every six months or every year. Sell those assets that have increased disproportionately and purchase more undervalued assets to reach back to your desired allocation.

Investing a huge amount in a single company, single mutual fund/category, or industry can be a bad idea. Diversification helps in protecting your portfolio from large losses by spreading out your risk.

You must represent a variety of asset types, sectors, and geographical areas in your portfolio. Diversifying your investment will help you reduce the impact that a single underperforming investment will have on your entire portfolio.

When deciding your asset allocation, you must consider your time horizon and the duration for which you wish to invest until you need the money. Although long-term objectives may withstand greater volatility, short-term objectives call for safer and more liquid assets.

Consider your time horizon and invest accordingly. For example, if you are planning for retirement in 20 years, you may afford a larger stock allocation. However, prioritize giving cash and bonds if you are saving for a down payment in two years.

Following the trends and doing what everyone else is doing will result in making bad investment choices. For example, if you invest in a trending asset class or industry that doesn't align with your financial objectives, investing heavily in it may put you in needless danger.

Don't get influenced by the hype: instead, consider your financial strategy and make your decision accordingly. When you invest with discipline, you will likely enjoy long-term success.

Now comes the time for implementation. Here are the steps to follow to build your strategic asset allocation:

Your investment goals determine the time horizon and required returns for your portfolio:

Your risk profile is a mix of your risk tolerance and your risk capacity.

You can reduce concentration risk in a single country's economy by diversifying internationally.

Select the broad categories of investments you will utilize based on your risk profile and goals. Some common asset classes include the following:

Rebalancing means bringing your portfolio back to your original, target asset mix.

For an NRI, understanding strategic asset allocation can be both exciting and challenging. It involves strategic planning and a good knowledge of both the Indian and international investment. It's vital to think about your future, plans, and timelines to build a successful investment portfolio. To achieve a balanced and diversified portfolio that aligns with your financial goals, it is crucial to manage risk effectively and stay compliant with regulations.

Moreover, if you wish to enhance your investment strategy and minimize your tax liability, reach out to an expert at Savetaxs. We have a team of experts who can ensure you stay compliant with all the regulations so that you can invest in India with confidence. Contact us right away and get peace of mind while you invest for the future and build a diversified investment portfolio.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Shubham Jain is the Founder of SaveTaxs and has extensive experience in Indian and NRI taxation. He advises individuals, NRIs, and businesses on tax filing, tax planning, capital gains, DTAA benefits, fund repatriation, and compliance matters. He regularly writes about taxation and related financial topics. His focus is on making complex tax concepts easy to understand. Through his articles, he helps taxpayers stay informed, avoid common mistakes, and stay compliant with Indian tax laws. See Full Bio

Want to read more? Explore Blogs

_1781845771869.webp&w=828&q=75)

_1778936280179.webp&w=828&q=75)

_1778936089630.webp&w=828&q=75)