_1784618918411.webp&w=828&q=75)

NRI Income Tax Compliance

7 Mistakes That Could Trigger an Income Tax Notice for salaried employees7 Mistakes That Could Trigger an Income Tax Notice for salaried employees

Written by Shubham Jain

Getting a scrutiny notice under section 143(2) means the Income Tax Department has selected your IT return for a detailed investigation. This notice is issued when the assessing officer wants further clarification or supporting documents regarding the return filed.

However, the notice does not directly mean you have avoided taxes; it simply means that the department wants some explanation and clarification regarding what you have filed.

In simpler terms, the notice under Section 143(2) is a scrutiny assessment notice. This means the income tax department has identified certain areas in your ITR that require further verification or clarification.

In this blog, we will understand the basics of the notice and how to respond to it when received.

A notice under section 143(2) means a scrutiny notice. This is issued when the tax department selects your ITR for detailed verification, often due to inconsistencies, mismatches, or specific risk parameters.

However, before issuing a scrutiny notice under section 143(2), the IT department sends an intimation under section 142(1). If the response to that intimation is not sent, or is not satisfactory, then the assessing officer issues the final notice under section 143(2).

The inconsistencies and discrepancies found in one's ITR can stem from any of the following: over-reporting losses, under-reporting income, or claiming deductions to which you are not eligible.

Keep in mind that receiving a scrutiny notice does not necessarily mean you are guilty; it is issued mainly to ensure correct tax reporting and compliance.

As mentioned, Income Tax Notice under Section 143(2) of the Income Tax Act 1961 is issued when the assessing officer identifies a mismatch or discrepancy in your ITR. The following are some situations in which the notice can be issued.

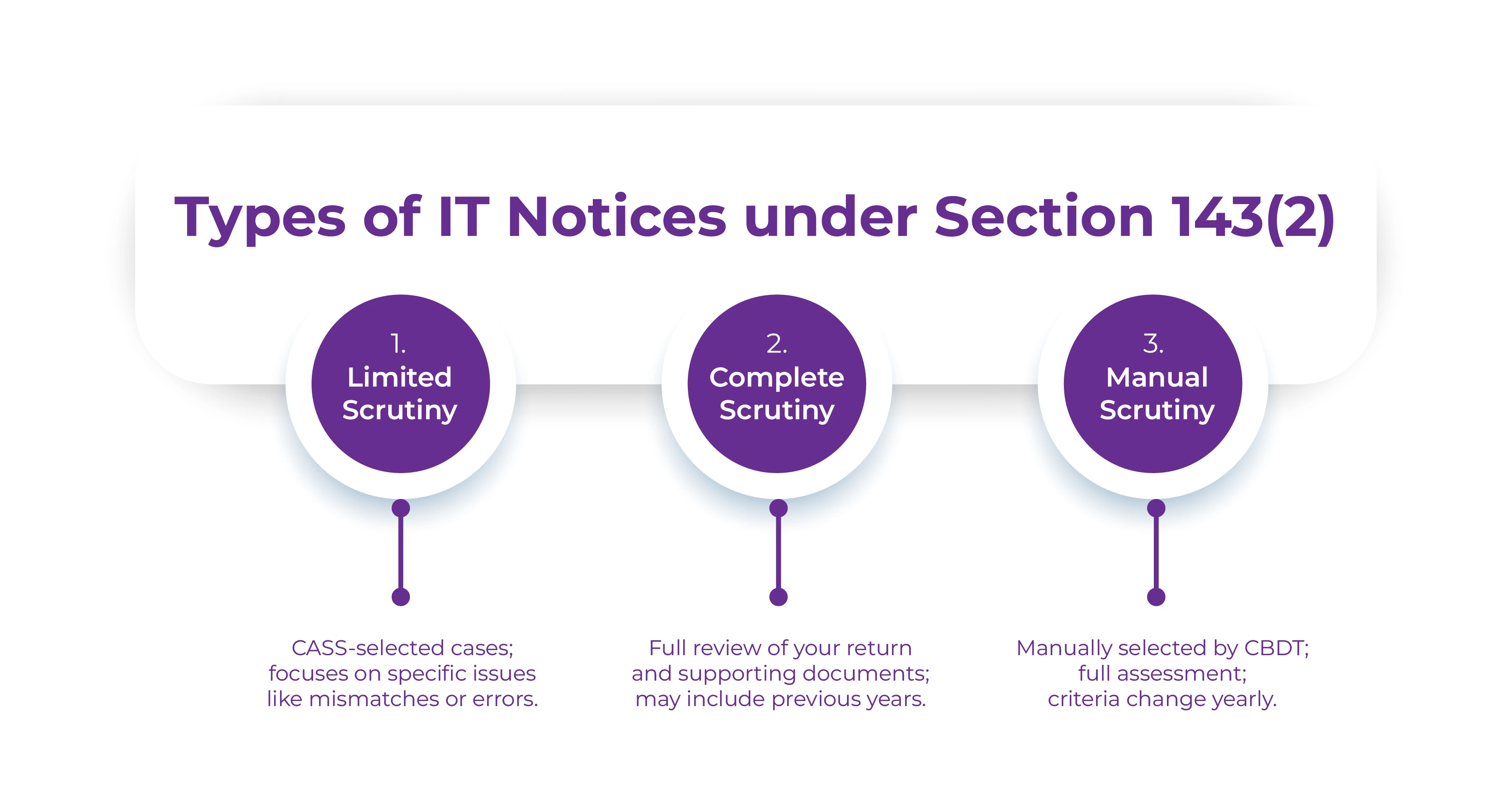

Below is a rundown of the types of notices you can receive under section 143(2) of the Income Tax Act, 1961.

These notices are generally selected through Computer-Assisted Scrutiny Selection (CASS) based on predefined risk parameters.

The assessment here focuses only on specific issues mentioned in the notice, for example foreign tax credit claims, property sale transactions, or certain deductions.

As the name suggests, this involves a comprehensive review of the income tax return filed along with supporting documents. Cases may be selected through CASS, and the assessing officer may also examine previous years’ records where relevant.

Here, selection criteria are defined by the Central Board of Direct Taxes (CBDT). These criteria may change periodically, and such cases undergo detailed examination.

A scrutiny notice under section 143(2) can generally be issued within three months from the end of the financial year in which the income tax return was filed.

For example, if Mr. Mukesh filed his income tax return on 31 July 2025 for FY 2024-25, the assessing officer can issue a notice under section 143(2) only until 30 June 2026.

Faceless assessment is a system through which the Income Tax Department conducts scrutiny assessments electronically. Notices are uploaded directly to the Income Tax portal.

Taxpayers usually receive alerts via email or SMS when notices are issued. Responses can be submitted online through the income tax portal.

The Faceless Assessment system ensures that the tax assessments are conducted online without you having to visit the Income Tax Department in person.

Here are a few things that you must know about a notice issued under section 143(2)

The notice is generally received electronically through the income tax portal and email. In some cases, physical communication may also be sent.

(The exact response requirements depend on the nature of the scrutiny notice.)

After submission, an acknowledgement or transaction reference number is generated.

You should not ignore this notice, as non-compliance may lead to consequences such as:

Generally, assessment orders under scrutiny are required to be completed within 12 months from the end of the relevant assessment year, subject to certain exceptions and extensions as per tax regulations.

Responding to a notice under section 143(2) within the prescribed timeline and accurately is essential. Failure to respond properly may lead to additional tax liabilities, penalties, or prolonged scrutiny.

Hence, NRI taxpayers should consider professional assistance when filing their ITR to reduce the chances of receiving such notices. If you receive one, consulting a tax professional with expertise in Indian tax laws can help ensure proper compliance.

One such expert we can discuss is Savetaxs. Savetaxs has been assisting NRIs with ITR filing in India and other tax-related services for years.

The experts here bring extensive combined experience to help manage tax compliance and optimize financial outcomes.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Shubham Jain is the Founder of SaveTaxs and has extensive experience in Indian and NRI taxation. He advises individuals, NRIs, and businesses on tax filing, tax planning, capital gains, DTAA benefits, fund repatriation, and compliance matters. He regularly writes about taxation and related financial topics. His focus is on making complex tax concepts easy to understand. Through his articles, he helps taxpayers stay informed, avoid common mistakes, and stay compliant with Indian tax laws. See Full Bio

Want to read more? Explore Blogs

_1784617942800.webp&w=828&q=75)

_1784547039242.webp&w=828&q=75)

_1784546974133.webp&w=828&q=75)