NRI Income Tax & Compliance

What Is Section 54B Of The Income Tax Act?What Is Section 54B Of The Income Tax Act?

Written by Hatim Dudhiyawala

As an NRI, maintaining compliance with the rules and regulations governing NRIs is not easy, especially when it comes to cross-border finances. In this, one such scenario is EPF withdrawal for NRIs, where they face issues.

If you are also facing the same situation, then you are on the right page. In this blog, we will help you understand the taxation on PF withdrawal for NRIs. Additionally, the blog discusses the factors affecting NRI PF withdrawals. So, read on and gather all the information about it.

Employee Provident Fund (EPF) is also referred to as Provident Fund (PF), is a retirement cum savings plan for the future that eligible organizations in India offer to their employees. This retirement scheme was introduced by the Indian government in 1952 to ensure that employees have a fixed source of income after retirement. Under this scheme, you and your employer need to contribute 12% of your monthly salary until you retire or leave your job. The PF schemes fulfill three objectives: providing pension benefits, generating wealth, and providing insurance.

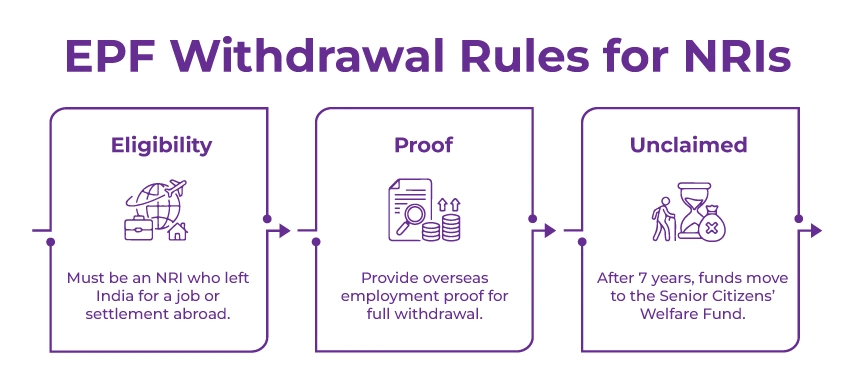

However, once you become a non-resident Indian (NRI), you no longer hold your EPF account. Considering this, you need to withdraw the entire amount from your EPF account immediately. In this scenario, you do not need to wait for the EPF account's completion period.

This was all about your PF, or your retirement account for NRIs. Moving ahead, let's know the EPF withdrawal rules for NRIs.

As mentioned above, after becoming an NRI, you do not need to wait for the completion period to make a withdrawal from your EPF account. However, there are some EPF withdrawal rules NRIs must follow. These are:

These are some of the EPF withdrawal rules for NRIs that must be met to close their EPF account. However, if over seven years you have not claimed your PF amount, it is transferred to the Senior Citizens' Welfare Fund. Additionally, it is difficult to retrieve after that. Moving on, let's look at the taxability of PF withdrawals for NRIs.

The table below provides a quick overview of the taxability of PF withdrawal for NRIs:

| Sr. No. | Scenario | Taxability |

|---|---|---|

| 1. | Before the completion of 5 years of service, the withdrawal amount is < INR 50,000 | No TDS is charged. However, if you fall under the tax bracket, when filing your ITR, you need to mention your PF withdrawal amount in your income. |

| 2. | Before completion of 5 years of employment, the withdrawal amount is > INR 50,000 |

There are two conditions in it:

|

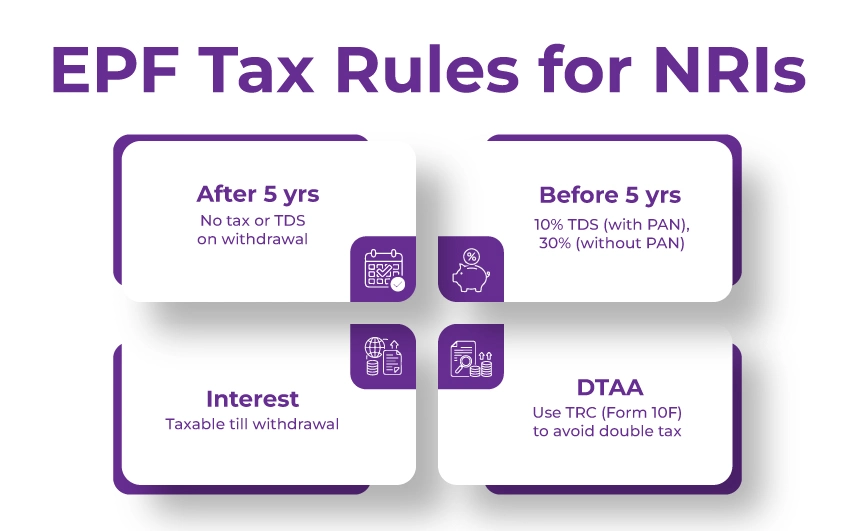

| 3. | PF is withdrawn after completion of five years of employment | No TDS is charged |

| 4. | In case of a job change, the transfer of the PF account | No TDS is charged. |

| 5. | Tax charged on interest accumulated from the last date of your job to till the time you withdraw the amount | As per the existing tax rules, it is taxable in India. |

These are some of the scenarios in which NRI PF withdrawals are taxed. Moving ahead, let's discuss the process for EPF withdrawal for NRIs.

There are two ways to make your EPF withdrawal: online or offline. However, before you proceed with your withdrawal, make sure you have your passport and visa ready.

Unless your Universal Account Number (UAN) is linked to your Aadhaar card, you cannot use the online process. Considering this, you can withdraw the entire amount from your EPF account through the UAN unified portal. Additionally, through the Employees' Provident Fund Organization (EPFO) 's UMANG mobile application, you can also make a withdrawal.

Further, when filling out the application form, do not forget to choose "abroad settlement" as the reason for leaving your job. Also, upload the clear scanned copies of your required documents in PDF or JPEG format. Lastly, complete verification using the OTP sent to your email ID or mobile number, and receive the EPF amount in your bank account.

If you are opting for the offline process, first download the EPF withdrawal form from the EPFO website. Additionally, you can ask your employer for this form. Considering this, there are two types of EPF forms available: Aadhaar-based and non-Aadhaar-based.

If your UAN is linked to your Aadhaar card, you can submit the filled form along with the required documents to your nearby EPFO office. If your UAN is not linked to your Aadhaar card, you need your employer's endorsement before submitting the form. Further, as in the online process, choose "abroad settlement" as the reason for leaving your job here as well.

This is how you can make an EPF withdrawal. Further, in both processes, once the verification is done within the next two weeks, your EPF balance is transferred to your bank account.

Now, moving further, let's know about the documents required for EPF withdrawal for NRIs.

To process the EPF withdrawal, NRIs need to submit the following documents:

These are the documents that NRIs need to submit at the time of EPF withdrawal, along with the application form. Moving ahead, let's know the tax scenarios for EPF withdrawal for NRIs.

If the EPF withdrawal is made after five years of constant service, then no tax is charged on withdrawal. However, if the EPF withdrawal is made before five years, TDC is imposed. Additionally, the tax liability is also affected by whether your PF account is linked to your PAN card. Apart from this, if there is a Double Taxation Avoidance Agreement (DTAA) between India and the other country where you reside, let's look at the different tax scenarios for EPF withdrawals for NRIs.

Further, to avoid paying taxes on the EPF withdrawal in two countries, you need to obtain a Tax Residency Certificate (TRC). For this, you need to fill out Form 10F with the income tax department. Once the Form 10FB is submitted, the TRC is issued by the Assessing Officer. Considering this, through TRC, NRI can take the DTAA benefit.

Managing your EPF account with an NRI status is quite difficult. It requires a proper understanding, along with following the EPF withdrawal rules for NRIs. Considering this, staying informed about EPF regulations, potential legislative changes, and tax laws is vital to maximizing the benefits of PF investments and securing your financial future.

Further, if you need more information or legal advice for your PF withdrawal, connect with Savetaxs. We have a team of tax experts who can better guide you on this and answer all your queries. Additionally, they can also assist you with better tax planning.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Shubham Jain is the Founder of SaveTaxs and has extensive experience in Indian and NRI taxation. He advises individuals, NRIs, and businesses on tax filing, tax planning, capital gains, DTAA benefits, fund repatriation, and compliance matters. He regularly writes about taxation and related financial topics. His focus is on making complex tax concepts easy to understand. Through his articles, he helps taxpayers stay informed, avoid common mistakes, and stay compliant with Indian tax laws. See Full Bio

Want to read more? Explore Blogs

_1782996918646.png&w=828&q=75)

_1782911003992.webp&w=828&q=75)