NRI Income Tax & Compliance

Income Tax E-ProceedingsIncome Tax E-Proceedings

Written by Hatim Dudhiyawala

Section 115F of the Income Tax Act 1961 is designed for Non-resident Indians (NRIs). Under this section, they can claim tax exemption on long-term capital gains (LTCG) from investments made in India. However, NRIs need to fulfill certain conditions.

This blog provides you with all the information about Section 115F and how NRIs can save taxes on their LTCG through it. So, let's start reading.

Section 115F of the Income Tax Act, 1961, is a tax exemption available on long-term capital gains (LTCG) from investments. This section is only available for non-resident Indians (NRIs). It is a highly effective tool for tax planning that helps NRIs in cross-border investment. However, to claim this tax deduction, NRIs need to fulfill the following conditions:

This was all about section 115F of the Income Tax Act, 1961. This section aims to encourage foreign investment in India. Additionally, provide an easy tax regime for NRIs. Moving ahead, let's know who can claim tax exemptions under this section.

As mentioned earlier, the tax exemptions under section 115F on long-term capital gains (LTCG) are only available for NRIs. However, to avail the benefits of this section, they need to fulfill certain conditions. These are as follows:

The above-stated specifications certify that NRIs with passive income from their Indian investments can claim the tax exemption under section 115F. Additionally, the applicable tax rate under this section is 20%. It is more than the tax rates imposed on Indian residents. Moving further, now, let's know what the specific conditions/ requirements are for NRIs to avail tax benefits under this section.

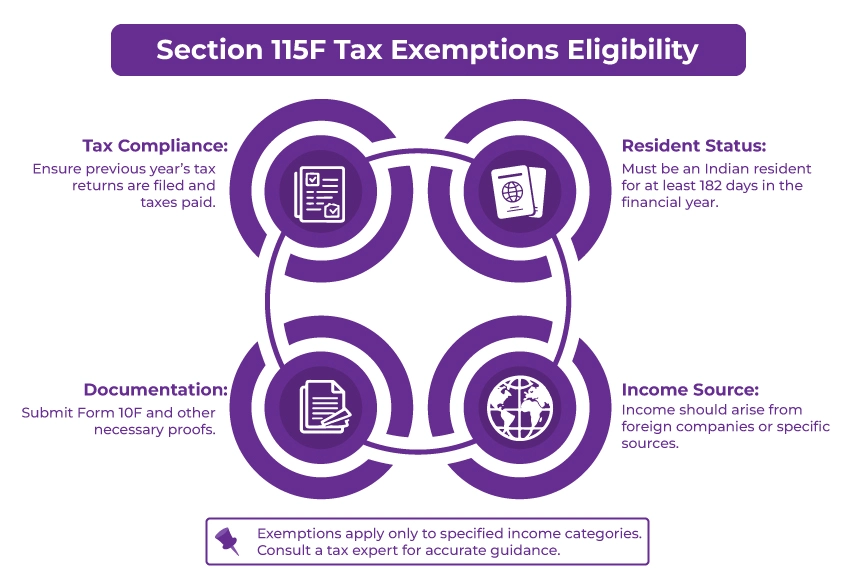

There are four key conditions that NRIs need to fulfill to claim tax exemption under section 115F. These are as follows:

These are the key requirements/ conditions that, as an NRI, you need to fulfill to claim tax exemption under section 115F. Further, during this period, you need to maintain your NRI status. You may also ask for the FIRC certificate, retain bank records, and investment documents to prove your NRI status during the period.

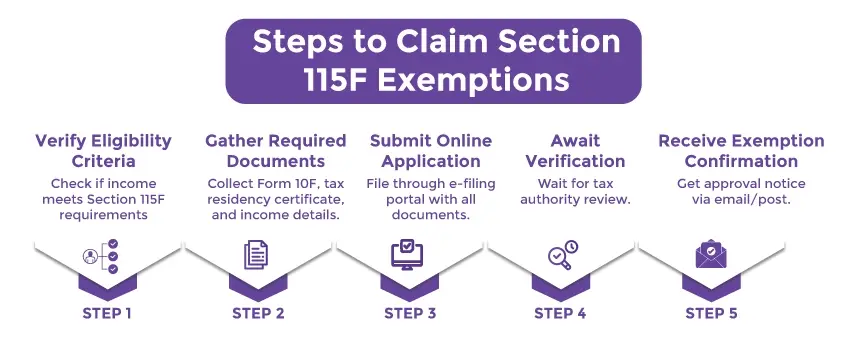

Moving ahead, let's know how to claim the tax exemption under Section 115F.

Follow the steps below to claim the tax exemption under section 115F of the Income Tax Act, 1961:

This is how you can claim a tax exemption under section 115F. Confused? Let's understand with an example.

Suppose a person named Anita is an NRI. Three years back, in India, she purchased listed equity shares of an Indian company, and now she has sold those shares at a value of Rs 6 crore. The original price of these shares during the purchase was Rs 3 crore. Considering this, Anita earned Rs 3 crore as long-term capital gain from these shares.

Further, to claim the tax exemption under section 115F, within four months, she reinvested Rs. 4.5 crore in buying shares of another Indian company. So, this was all the information. Now, let's calculate the tax exemption amount under Section 115F on LTCG.

Formula: Exempt LTCG = (Reinvested amount / Net Sale Value) * Total long-term capital gain

Exempt LTCG = (Rs 4.5 crore / Rs. 6 crore) * Rs 3 crore = Rs. 2.25 crore

Taxable LTCG = (Rs 3 crore - Rs 2.25 crore) = Rs 75 lakh

Saved tax: Assuming post-indexation, the LTCG tax rate is 20% = Rs 2.25 crore * 20% = Rs 40 Lakh

So, this is how using section 115F, NRIs claim tax exemption on their long-term capital gain. Moving further, let's know the ax benefits of this section.

Here is the list of key benefits section 115F of the Income Tax Act, 1961, offers to NRIs:

So, here is how, apart from saving tax, section 115F helps NRIs in India. Moving ahead, let's know the changes stated in Clause 215 in the 2025 Income Tax Bill for this section.

The 2025 Income Tax Bill, using Clause 215, proposes the following updates in Section 115F:

So, these are some of the updates stated under Clause 215 for section 115F.

Lastly, from the above information, it is clear that Section 115F of the Income Tax Act, 1961, is a special tax regime for NRIs who have passive income from Indian investments. This section makes the requirements of tax compliance easier for NRIs. Additionally, provide them with more attractive investment options. Well, it is not a tax evasion but a tax optimization tool for NRIs.

Further, if you are planning to sell your Indian assets, connect with Savetaxs. We have a team of experts who will assist you in maximizing your post-income tax returns. Additionally, if you want, they will also help you with tax planning.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Shubham Jain is the Founder of SaveTaxs and has extensive experience in Indian and NRI taxation. He advises individuals, NRIs, and businesses on tax filing, tax planning, capital gains, DTAA benefits, fund repatriation, and compliance matters. He regularly writes about taxation and related financial topics. His focus is on making complex tax concepts easy to understand. Through his articles, he helps taxpayers stay informed, avoid common mistakes, and stay compliant with Indian tax laws. See Full Bio

Want to read more? Explore Blogs

_1782475363401.webp&w=828&q=75)