NRI Income Tax & Compliance

What Is Section 54B Of The Income Tax Act?What Is Section 54B Of The Income Tax Act?

Written by Hatim Dudhiyawala

NRIs can apply for a loan in India to own a residential property. An NRI home loan is a financial tool specifically designed for NRIs who want to purchase, construct, or renovate a residential property in India. These loans are similar to regular home loans but have specific eligibility criteria. It is regulated by the RBI (Reserve Bank of India) to ensure compliance with foreign exchange laws.

Similar to Indian residents, an NRI home loan can cover 70% - 90% of the property's value. The NRI must use their personal funds to pay the remaining balance in INR. In this blog, we will guide you through everything you need to know about an NRI home loan. We will discuss the benefits, eligibility criteria, required documents, interest rates, and much more.

An NRI home loan is a special type of home loan granted to Indian citizens residing abroad. These loans function just like a regular housing loan. If your loan is approved, you will receive a specified amount that you can use to purchase, construct, or renovate a residential property in India.

You can also use it to purchase a plot or fund home improvement projects. However, as per FEMA (Foreign Exchange Management Act) guidelines, an NRI cannot purchase agricultural land, farmhouses, or plantation properties in India with an NRI home loan.

An interest charge will be applied to the amount in accordance with the prevailing rate. You must mandatorily repay the loan amount within the specified tenure. The banks and financial institutions usually allow you to repay the amount through EMI (Equated Monthly Installments) payments. The loan repayment must be made strictly through an NRE (Non-Resident External) account, an NRO (Non-Resident Ordinary) account, or international remittances.

Here are the benefits that an NRI can avail of after taking an NRI home loan:

Before applying for an NRI home loan, make sure you meet the eligibility requirements. Several factors like age, employment type, credit score, work experience, etc. might impact your loan approval. Consider the table below to determine your eligibility:

| Criteria | Eligibility Requirments |

|---|---|

| Age | 23-65 years |

| Educational Qualification | A diploma or degree is required. Also, must have a minimum of three years of overseas experience or one year of professional degree experience. |

| Employment | Salaried or Self-Employment |

| Work Expereince | Minimum 2 years of employment in the current company |

| Minimum Salary | Differs based on the lender |

| Residential Status | NRI (Non-Resident Indian), PIO (Person of Indian Origin), or OCI (Overseas Citizen of India ). |

| Credit Score | 750+ (varies by financial institution) |

| Tenure | Up to 15 years |

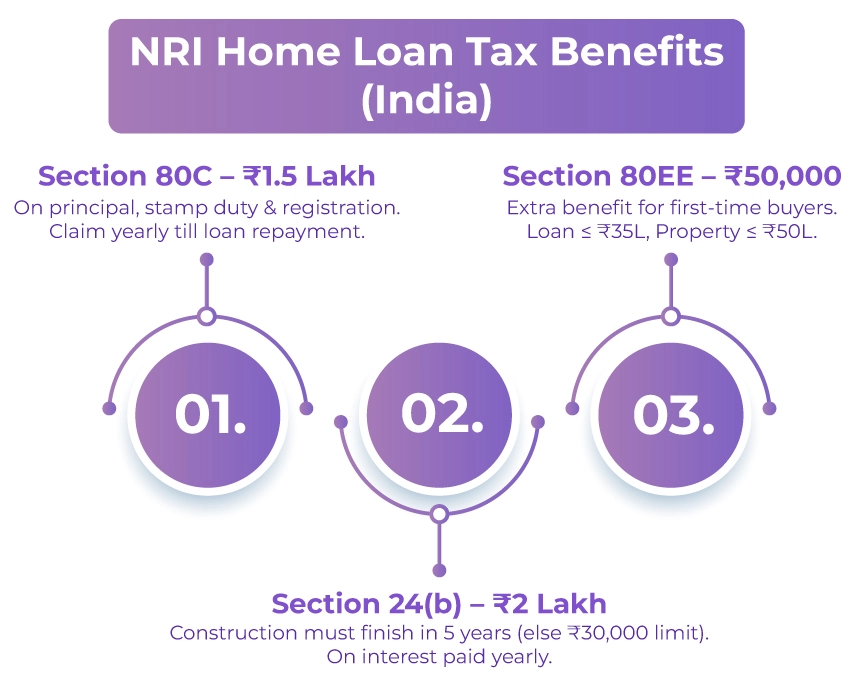

An NRI can enjoy several tax benefits on a home loan in India. You can claim tax deductions with NRI home loans in India under various sections of the IT Act, 1961. These include:

You can claim an annual income deduction of INR 150,000 on your home loan expenses and repayment under section 80C. This includes a one-time deduction for loan registration charges and stamp duty in the year of acquiring the property.

From the following year, the deduction applies to the principal repayment of the home loan. Additionally, you can keep claiming the deduction of INR 150,000 every year under section 80C until you repay the loan completely.

The Government of India provides benefits for first-time homebuyers financing their property through a home loan. Under Section 80EE of the IT Act, you can claim an additional deduction of up to INR 50,000. This one-time deduction applies to Home Loans of up to INR 35 lakhs, with the property value not exceeding INR 50 lakhs.

Under section 24(b), you can claim tax deductions of up to INR 200,000 annually on the interest repayment component of your home loan. Similar to Section 80C, this deduction is available every year until the end of the loan tenure, provided the property construction is completed within five years of loan disbursement; otherwise, the limit is reduced to INR 30,000 annually.

Here are the documents you need to apply for an NRI home loan:

NRI home loan rates are generally the same as those of normal home loan rates. Consider the table below to understand the interest rates as per banks:

| Bank | Interest Rates p.a. (per annum) |

|---|---|

| SBI | 6.90% - 7.50% p.a. |

| Axis Bank | 6.90% - 8.55% p.a. |

| HDFC Ltd. | 6.90% - 8.00% p.a. |

| Canara Bank | 6.90% - 8.90% p.a. |

| Bank of Baroda | 6.85% - 7.20% p.a. |

Generally, lenders issue a loan amount for a specified time window, which is called tenure. The tenure is the time period within which you need to repay the entire loan amount. Usually, an NRI's home loan tenure is between 15 to 30 years; however, it may differ from lender to lender. Furthermore, it may also differ depending on the strength of your application.

An NRI can easily apply for a home loan in India from anywhere in the world, provided they meet the eligibility requirements. Numerous lenders offer competitive interest rates for NRI home loans, so you must review and choose as on your needs. Additionally, the application process is simple and quick.

Now that you know more about how to apply for an NRI housing loan with this comprehensive guide, you can avail the funds required to set up a home base in India. To know more about how your loan will be taxed, eligible deductions, and many other doubts, it's advised to seek guidance from a reputable professional at Savetaxs.

We have an entire team of experts with years of experience and knowledge in this field. They will help you understand your tax liability on the loan amount. Also, they will assist you in determining the deductions you are eligible to claim and guide you regarding fund repatriation. So, contact us right away, and expereince utmost convenience and precision. We are working around the clock across all time zones to provide you with the highest quality service.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Shubham Jain is the Founder of SaveTaxs and has extensive experience in Indian and NRI taxation. He advises individuals, NRIs, and businesses on tax filing, tax planning, capital gains, DTAA benefits, fund repatriation, and compliance matters. He regularly writes about taxation and related financial topics. His focus is on making complex tax concepts easy to understand. Through his articles, he helps taxpayers stay informed, avoid common mistakes, and stay compliant with Indian tax laws. See Full Bio

Want to read more? Explore Blogs

_1782996918646.png&w=828&q=75)

_1782911003992.webp&w=828&q=75)

The total tax savings depend on your loan amount, interest rate, repayment structure, and your tax slab:

It means you can save up to Rs. 3.5 lakh in a financial year. If you fall under the 30% tax slab, the maximum saving can be around Rs. 1.05 lakh per annum.

You can enjoy several tax benefits on your home loan under these sections: