What is a Schedule K-1 Tax Form?

Read More

The IRS Form 1099-R is used to report the distribution income received by the taxpayer from their retirement accounts. It includes profit-sharing plans, annuities, pensions, individual retirement accounts (IRAs), and more. This form helps the IRS track the income received by individuals from their retirement plans.

Are you also receiving money from your retirement account? It means that during the tax season, you will also get this form. But before that, it is vital to have basic information about it. Read on the blog. In this, we have covered all the details of Form 1099-R from what it is to who should file it.

The IRS Form 1099-R is known as "Distributions from annuities, pensions, profit sharing plans, retirement, insurance contracts, or more. As mentioned at the start of the blog, this form is used to report the distribution of retirement benefits. It includes income received from annuities, pensions, or other retirement plans.

Furthermore, the IRS Form 1099-R is an informational return form. You used this form to report income on your federal income tax return. Additional variations of this form include:

Generally, most of the private and public pension plans that are not part of the Civil Service System use the Form 1099-R. Additionally, if you get a distribution of $10 or more from your retirement plan, then surely you will receive Form 1099-R.

This was all about Form 1099-R. Moving ahead, let's know about the different types of distributions included in this form.

Employer-based retirement benefits are generally an extension of compensation. The employer arranged this for the employee. On most of the retirement plan contributions, the income tax is deferred. It means that until the amount is withdrawn, the taxpayer does not pay tax on the contributed funds.

Usually, annuity distributions and pensions are for disabled employees and retired employees. Additionally, in some cases, it may also be received by the beneficiary of a deceased employee.

Furthermore, against the pension plan, if you take a loan, and during the repayment of the loan, you pay interest. In this scenario, the loan will not be considered as a distribution in many cases. However, if you do not make the loan payments on time, Form 1099-R will be issued to you.

In terms of finance, rollovers mean transferring retirement funds from one plan to another without payment of taxes on the transferred money. The specific meaning of rollovers depends on the context it is used. However, it always includes an extension, transfer, or deferral of a financial position or product.

To avoid paying taxes on the funds and possible early distribution penalties, generally, funds should be rolled over within 60 days of distribution into a qualified account. Generally, within 12-month periods, you can only do one indirect rollover. Here, it does not matter how many types of IRA accounts you have.

Furthermore, funds that are distributed directly are taxed at 20% federal income tax withholding. This means that to make up for the 20%, taxpayers need to add additional funds. Additionally, send it to the IRS so that the amount of the rollover can be equal to the total distributed amount.

Also, when a rollover meets all the Internal Revenue Service guidelines, you do not need to pay tax on the distribution. However, you still need to report the amount on your income tax return and state it as a rollover.

Some companies permit employees to take a loan against their pension plans. Generally, the repayment of these loans is done with interest, and they are not counted as distributions. Considering this, Form 1099-R is issued when the repayment of the loan is not made on time.

When this happens, the amount that is not paid is stated as a distribution. Considering this, on Form 1099-R, it is mentioned on the distribution code L. These are deemed taxable income and face early distribution penalties.

Many benefits before the taxpayer turns age 59 1/2, paid off, are considered as early distributions. On early distribution, an extra 10% federal tax is imposed. It is done to prevent the misuse of these retirement funds. Apart from this, a state penalty is also imposed by some states on early distributions.

Furthermore, the additional tax applies to the whole taxable distribution amount, unless there are any exceptions to it. Considering this, some common exceptions include:

Under the qualified domestic relations (divorce) order, if payments are made to another payee, an exception is applicable.

This was all about the income distributions included in this form. Moving ahead, let's know who can file Form 1099-R.

As per the IRS guidelines, an entity that manages any of the below-stated accounts is responsible for filing out the Form 1099-R. This form applies to each distribution that is $10 or more.

Furthermore, like most 1099 Forms, Form 1099-R should also be given to recipients by January 31 of the following tax year. Anyone who gets this form needs to mention the amount stated on the form in their tax return and pay taxes on it.

Moreover, if you receive this form, not all distributions you received from tax-deferred or retirement accounts are subject to tax. An example of it is a direct rollover you receive from a 401(k) plan to the IRS.

This was all about who needs to fill out Form 1099-R. Moving further, let's know what information is stated in this form.

The IRS Form includes the following information. Here we have mentioned a few essential box numbers that often ask tax questions.

It was all about the boxes stated in the Form 1099-R that you generally need to consider. Moving further, let's know the other information stated in this form.

This is the information you will get in Form 1099-R. Moving ahead, let's know about the different types of distribution codes mentioned in this form.

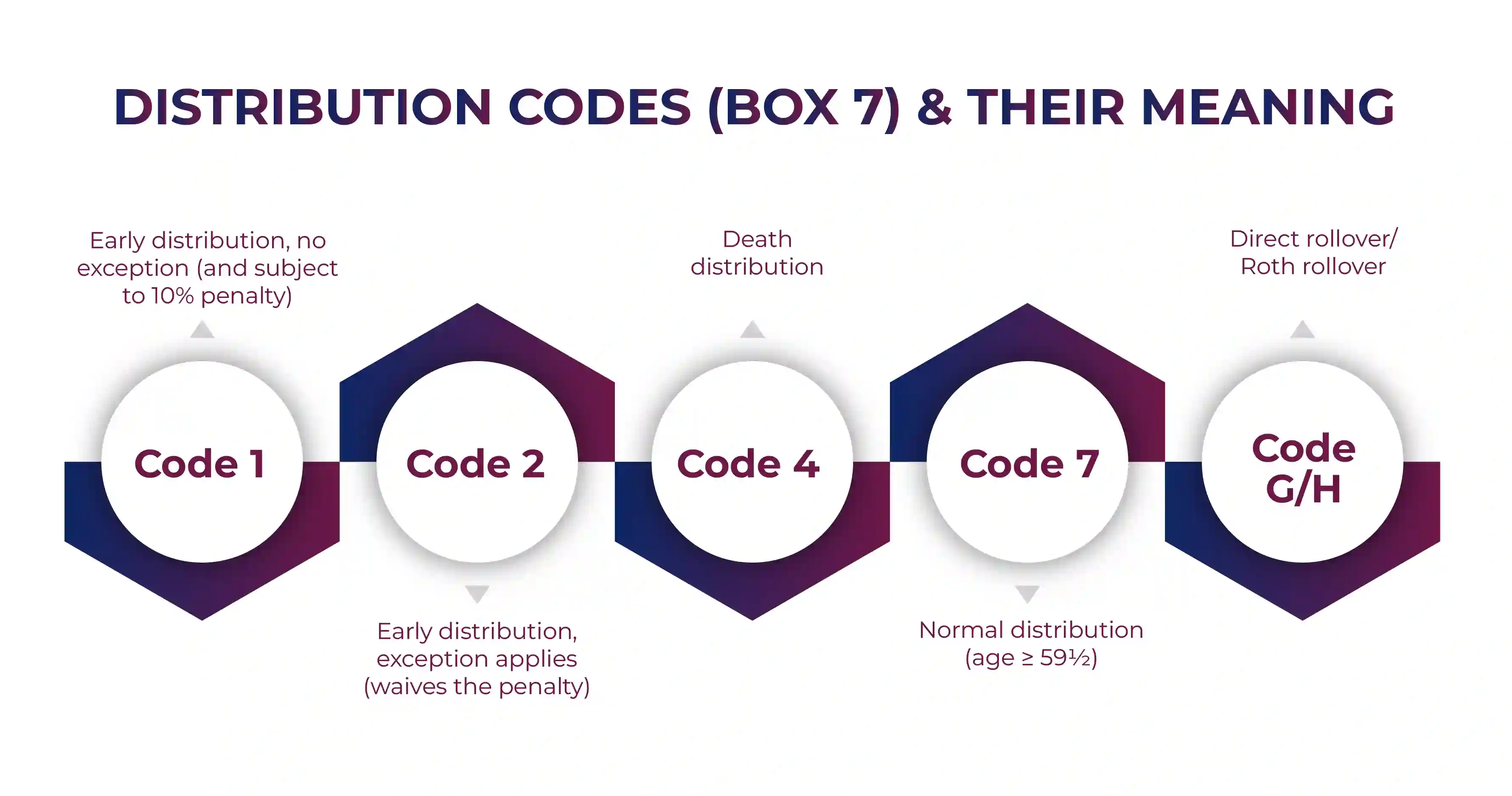

As stated above, there is a code field mentioned in the Form 1099-R. It helps in identifying the distribution type. This is mentioned on Box 7 of the form. Further, let's know about these codes.

Furthermore, based on the amount mentioned in Box 2a of the Form 1099-R, Code 4 is taxable.

The Form 1099-R is an essential tool. It helps in tracking the taxable retirement distribution. Additionally, also certifies that proper tax information is received by the IRS. Here, the complete blog was about this form. From what it is used for to who should file it, all the information is stated in this blog. Hope after reading it, you get all the understanding of this form.

Furthermore, if you still have some confusion related to this form, connect with Savetaxs. The experts in our team will solve all your doubts and provide you clear understanding of this form. They have expertise in US taxation, and if you want can also help you with your tax returns.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Mr Varun is a tax expert with over 13 years of experience in US taxation, accounting, bookkeeping, and payroll. Mr Gupta has prepared and reviewed over 5,000 individual and corporate tax returns for CPA firms and businesses.

Want to read more? Explore Blogs

_1759750925.webp&w=828&q=75)