US Tax Filing and Compliance

Substantial Presence Test Explained: How NRIs Determine US Tax Residency?Substantial Presence Test Explained: How NRIs Determine US Tax Residency?

Written by Shubham Jain

-plan_1761282887.webp&w=3840&q=75)

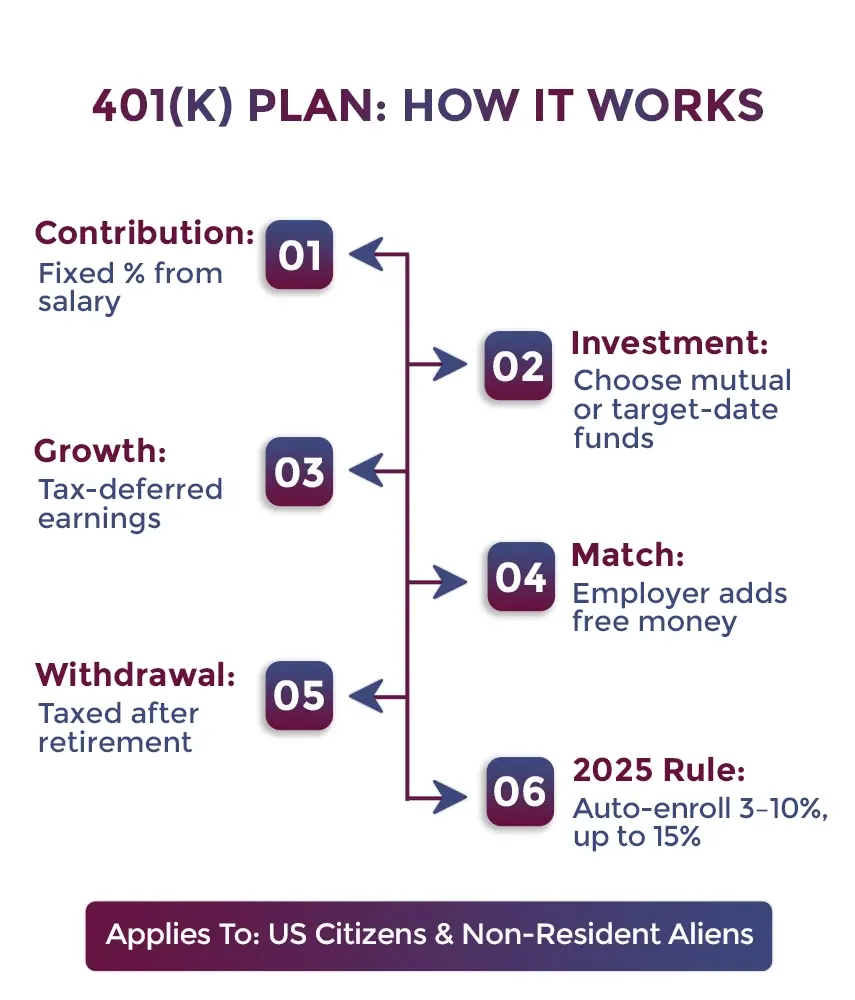

A 401(k) plan is one of the most popular tax-benefit retirement savings plans in the USA. This retirement savings plan is sponsored by US companies for their employees. Additionally, along with the US citizens, the 401(k) plan is also available to non-resident aliens who, while staying there, worked for a US company. While helping employees save for the future, this plan also includes several tax advantages.

Further, here is a quick guide to help you better understand the 401(k) plan, how it works, its different types, withdrawal rules, and more.

A 401(k) plan is a retirement savings plan in the USA that US companies sponsor for their employees. Under this, employees from their income need to contribute a specific amount to an investment plan to save for retirement. Also, the employee makes his contribution to this retirement plan up to a specific limit.

Additionally, this investment plan is also available for non-resident Indians who work for a US company while staying there. Further, the rules, regulations, working, and tax deductions of 401 (k) are the same for both US citizens and non-resident aliens.

So, in simple words, a 401(k) plan is an investment that employees save from their income to use after retirement. Further, let's know how this investment plan works for employers.

Depending on their visa type and residential status, non-resident aliens can also participate and contribute to the 401(k) plan. Like the US citizens, the same withdrawal and contribution rules apply to them, such as withdrawing the amount after turning 59½, and more.

Here is how 401(k) plan works for employers:

Further, with the start of 2025, many employers enrolled their eligible employees at a 3% to 10% contribution rate into the existing 401(k) and 403(b) plans. Until this contribution rate reaches 15%, it will increase annually. It is a change introduced by the Secure 2.0 Act. This plan helps employees save for their retirement.

Additionally, the working of the 401(k) plans remains the same for US citizens and non-resident aliens. Now, moving ahead, let's know the different types of these plans.

The 401(k) plans are generally of two types, i.e., traditional and Roth 401(k). The traditional 401(k) plan is funded with pretax money, while the Roth plan is taxed after contributions. Additionally, the type of plan you choose determines your tax benefits. Also, whether you received it now or after your retirement.

Further, let's better understand both the 401(k) plans by differentiating them.

| Basis | Traditional 401(k) Plan | Roth 401(k) Plan |

|---|---|---|

| Contribution Limits |

The 401(k) contribution limit is the same for both traditional and Roth. Considering this, in 2025, you can contribute a maximum of $23,500. Additionally, people who are 50 years or older can contribute an additional $7,500 ($31000) as a catch-up contribution. Further, because of the Secure 2.0 Act, people aged between 60 to 63 can catch-up contribution of $11,250. Also, you can make contributions to both retirement plans in the same year as long as your contribution is within the limit. |

|

| Tax treatment of contributions | Contributions are calculated before the tax deduction. This further results in reducing your present adjusted gross income (AGI). | With zero impact on your present adjusted gross income (AGI), contributions are determined after tax deduction. Considering this, the employer-matching dollars should be stated on the pretax account, and when distributed, they should be taxed. |

| Tax treatment of withdrawals | Withdrawals are taxed as ordinary income after retirement. | After retirement, on qualified distributions, no taxes are paid. |

| Withdrawal rules |

Have to pay taxes on withdrawals of earnings and contributions. If the distribution is taken before the age of 59½, unless one of the IRS exceptions is fulfilled, you need to pay tax on it. Further, after a certain age, account holders in a traditional 401(k) plan must take required minimum distributions. |

As long as the IRS does not qualify the distribution, withdrawals of earnings and contributions are not taxed. Considering this, the retirement account should be held for at least five years, and the distribution is:

Also, these retirement plans do not have a minimum distribution. |

These were the key differences between a traditional 401(k) plan and a Roth 401(k) plan. Moving ahead, now let's know the contribution limits of the 401(k) plan for 2025.

Here are the contribution limits of the 401(k) plan for 2025 for US citizens and non-resident aliens:

| Basis | 401(k) Plan Contribution Limits for 2025 |

|---|---|

| Employee Contribution Limit | $23,500 |

| For individuals age 50 and older, the catch-up contribution limit | $7,500 or up to $11,250 for those individuals who are between 60 to 63 years. |

| Maximum employee and employer contribution | Those under 50 years can contribute up to $70,000 (those who are 50 years or older can contribute up to $77,500) or full employee compensation. |

Further, the last day for contributing to the 401(k) plan in 2025 is December 31. Additionally, you can contribute any amount to a 401(k) plan without any income limit restrictions.

Also, compared to individual retirement accounts (IRAs), a 401(k) plan has higher annual contribution limits. The contribution limit of an IRA is $7000, and who are age 50 years or older is $8000 in 2025.

Are you still thinking about how much you should contribute to your 401(k) retirement plan? Then, according to financial experts, you should contribute 10% to 15% of your earned income to your 401(k) plan. If it is more than your income, then, as per your choice, you can contribute the amount.

So, this was all about the contribution limits of the 401(k) plan for 2025. Moving ahead, let's know the 401(k) pros and cons.

The withdrawals rules for 401(k) plan are as follows:

Furthermore, in many cases, taxpayers still have to pay taxes on their early withdrawals from 401(k) plans. Additionally, to invest over time, they have less money.

So, these were the common withdrawal rules for 401(k) plans that you need to follow. Moving further, let's know the required minimum distributions for these retirement plans.

Once you turn 73, then taking withdrawals from your 401(k) plan is not your choice but your right. Here, the required minimum distributions are the amounts you should withdraw from your retirement plan. However, if you are still working and opt to defer until your retirement, this is optional.

Also, you can withdraw an amount more than the minimum limit of the 401(k) plan. As a part of your income, these distributions are taxed when you file your tax returns. Considering this, if you choose the Roth 401(k) plan, then you do not have any required minimum distributions.

This was all about the required minimum distributions. Moving ahead, let's know what happens to your 401(k) plan if you quit your job.

In case you quit your job, then you can take the money from your 401(k) plan with you. Additionally, you can either roll the money into an IRA or a new 401(k) employer plan.

Further, if you are a non-resident alien with a 401(k) plan and planning to return to India, then you can cash out your money from the plan. Additionally, you can roll over your 401(k) plan to an IRA or leave the plan till you turn 59½ to make penalty-free withdrawals.

Lastly, a 401(k) is a retirement plan that employers sponsor for their employees. It helps them save a certain amount for their retirement. Considering this, a specific amount is deducted monthly from the employee's income to contribute to the retirement plan. Additionally, the 401(k) plan has the same rules for residents and non-residents in the US.

Further, the complete blog was about the 401(k) plan. If you still have confusion or want to know more about this plan, connect with Savetaxs. Our experts will solve all your queries related to this plan and provide you with comprehensive details on it.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Shubham Jain is the Founder of SaveTaxs and has extensive experience in Indian and NRI taxation. He advises individuals, NRIs, and businesses on tax filing, tax planning, capital gains, DTAA benefits, fund repatriation, and compliance matters. He regularly writes about taxation and related financial topics. His focus is on making complex tax concepts easy to understand. Through his articles, he helps taxpayers stay informed, avoid common mistakes, and stay compliant with Indian tax laws. See Full Bio

Want to read more? Explore Blogs

_1784032485815.webp&w=828&q=75)