Investment & Financial Planning

FCNR Deposit Interest Rates in 2026FCNR Deposit Interest Rates in 2026

Written by Hatim Dudhiyawala

Investing in Indian mutual funds is an excellent way for NRIs to grow wealth and diversify their portfolio. For this, NRIs need to follow the guidelines set by the Foreign Exchange Management Act 1999 (FEMA). However, navigating these rules can seem difficult. Additionally, violations can result in frozen accounts, penalties, and, in severe cases, legal action.

To help you understand the impact of FEMA rules on NRI mutual fund investments, this blog will provide guidance. It includes which account you should use, what you can and cannot do, how repatriation of funds works, and how to avoid paying penalties. In short, at the end of the blog, you will know by following the FEMA rules how to invest in mutual funds confidently.

The full form of FEMA is the Foreign Exchange Management Act. This act was introduced by the government in 1999, replacing the FERA (Foreign Exchange Regulation Act). Compared to the old act, it has a more liberalized structure for managing foreign exchange in India. In simple words, FEMA is:

Further, as mentioned above, for NRIs investing in mutual funds, FEMA has designed a specific set of rules. Considering this, you cannot use any bank account or invest in any instruments. Additionally, you cannot transfer your money freely without following the requirements.

The primary objective of FEMA is to facilitate external payments and trade while maintaining the orderly development of the foreign exchange market of India. Under FEMA provisions, NRIs are allowed to invest in several financial instruments in India. It includes exchange-traded funds (ETFs), direct stocks, and mutual funds.

However, following the FEMA regulations is vital, such as the submission of the Know Your Customer (KYC) updated documents, and compliance with repatriation limits. Additionally, opening a rupee-dominated Non-Resident External (NRE) or Non-Resident Ordinary (NRO) account.

So, this was all about FEMA basics that every NRI mutual fund investor should know. Moving ahead, let's know the FEMA rules for using NRE & NRO accounts in mutual funds.

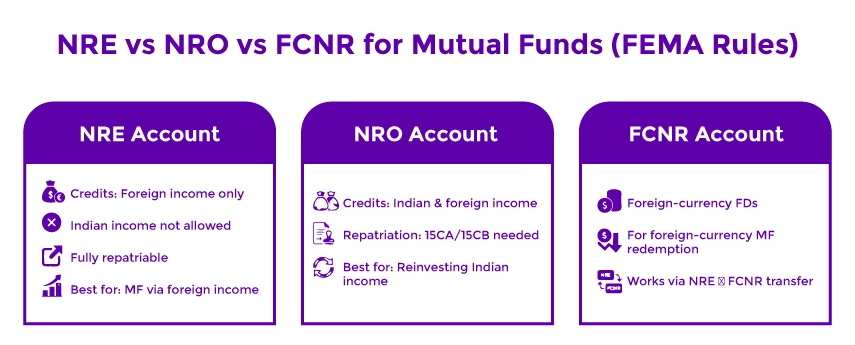

FEMA allows NRIs to open three types of bank accounts, each of which serves a different purpose. Additionally, selecting the wrong one for mutual funds can later create issues.

These were the rules for using NRE & NRO accounts in mutual funds. Selecting the correct account directly affects your documentation, repatriation flexibility, and taxation. This further makes the FEMA compliance vital for smooth investing. Now, moving ahead, let's know the FEMA repartition & rules for mutual fund redemption.

Repatriation can be defined as the process of transferring money from India back to a foreign bank account. For repartition, as well, FEMA has strict rules on how much you can repatriate and under what circumstances.

Further, if you want to repatriate beyond $ 1 million, then FEMA allows you to take special approval from the RBI. It is granted in exceptional circumstances only, such as retirement process, inherited property, and more. However, approvals from the government take months, and it is not guaranteed that you will get it.

These were the FEMA rules for fund repartition. Moving further, let's know about the permitted and restricted mutual fund investments under FEMA.

Generally, FEMA allows NRI mutual fund investments. However, there are specific restrictions on it. Want to know about the permitted and restricted mutual funds for NRIs? Read the points below and get your answers:

| Mutual Funds NRIs Can Invest In | Investments Prohibited Under FEMA |

|---|---|

| Debt mutual funds | Public Provident Fund (PPF) |

| Index funds | Kisan Vikas Patra (KVP) |

| Equity mutual funds | National Savings Certificates (NSC) |

| Hybrid mutual funds | Agricultural land, farmhouses, plantations |

| Sectoral/ thematic funds | - |

| ELSS (tax-saving funds) | - |

This was all about permitted and restricted mutual fund investments for NRIs under the FEMA regulations. Moving ahead, let's know the mandatory KYC, FATCA & FEMA compliance requirements.

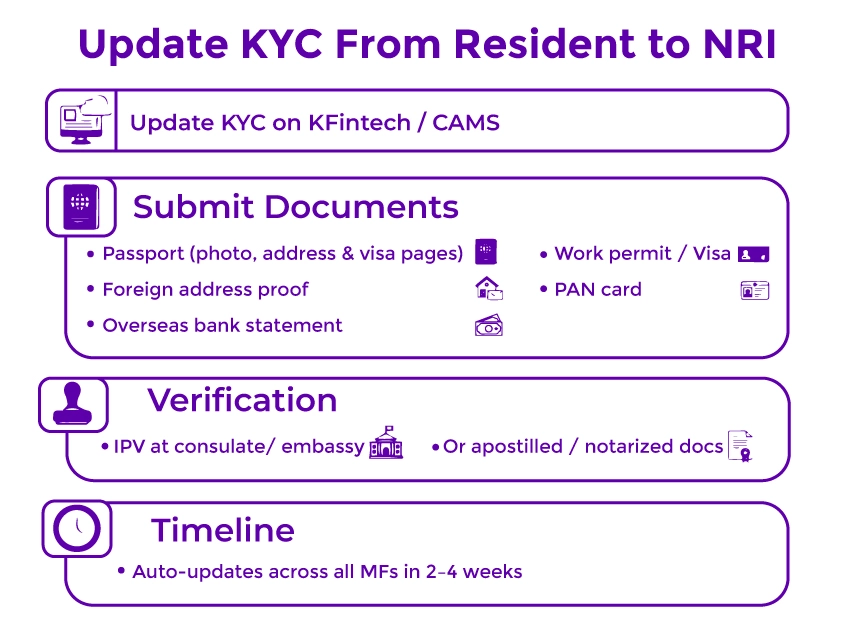

Under the FEMA regulations, NRIs must update their KYC details when their residential status changes. It is not an optional choice but a compliance requirement. Here is what you should do:

Across all your mutual funds in India, through KRAs (KYC Registration Agencies) like KFintech and CAMs, your KYC is centralized. Considering this, when you get NRI status:

Once you update your KYC information with one Asset Management Company (AMC), it automatically shows in all mutual funds you hold. This process generally takes 2-4 weeks.

FATCA, or the Foreign Account Tax Compliance Act, and CRS, or the Common Reporting Standard, are international tax compliance structures. Under it, with 100+ countries, agreements have been signed by India to share financial information. Considering this, when investing in mutual funds, you should declare:

This information is used by AMCs to report your holdings to Indian tax officials, which is further shared with your home country. Further, without a CRS/ FATCA declaration, AMCs do not accept your investment.

Connect with Savetaxs and open an NRE account that matches your financial goals and investments.

Once your Indian savings account is converted to an NRE/ NRO account, you should update this linkage with your every mutual fund folio. Several AMCs allow online account updates. You can do this by following the mentioned steps:

Further, now your redemptions will be credited to your NRE/ NRO account, maintaining FEMA compliance. It is advisable after gaining the NRI status, complete these three steps within 90 days. It is because the longer you delay the process, the higher the risk of frozen transactions or non-compliance penalties.

Now, moving further, let's know about the penalties for FEMA violations.

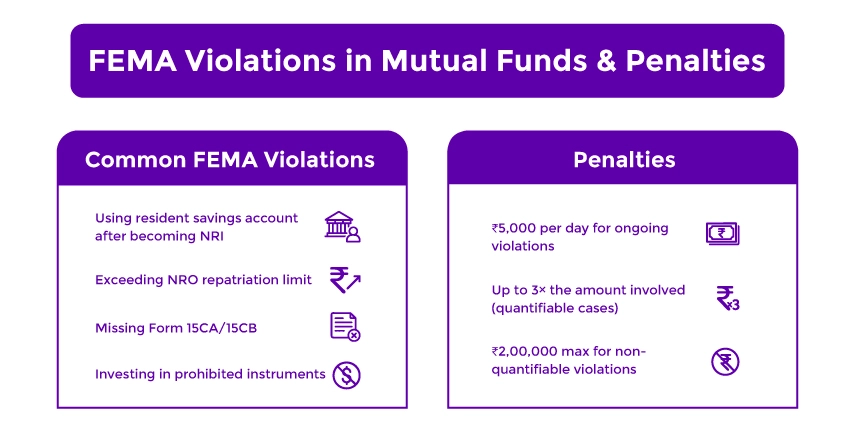

FEMA violations in mutual funds can result in paying significant penalties. The Enforcement Directorate (ED) actively monitors and enforces FEMA regulations. Further, common FEMA violations include:

These were the FEMA violations. Now, let's know the penalties included in it:

This was all about FEMA violations in mutual funds and their penalties. Moving ahead, let's know the role of FEMA in Taxation of NRI mutual fund gains.

Ask anything related to finance and investment with our tax experts and maximize your returns.

Many NRIs often get confused between the FEMA and Indian tax laws. They are different, but they intersect. FEMA manages your foreign exchange transaction, such as which account you hold, repatriation limit, and more. Whereas, the Income Tax Act manages how you will be taxed on interest, capital gains, dividends, and more. Further, as an NRI, both are imposed on you. Here is how they interact for mutual fund gains:

It is taxes according to the Income Tax Act when you redeem your mutual funds:

Further, AMC automatically deducts TDS (Tax Deducted at Source). If you file ITR, you can claim the refunds for your TDS.

When you repatriate your mutual funds through an NRO account:

In case the taxes are not paid and TDS is not deducted, until you clear all your tax dues, the bank will not allow repatriation.

India has signed Double Taxation Avoidance Agreements (DTAA) with 90 countries. So if you paid taxes on your mutual fund gains in India and your resident country, you can claim a tax credit in one country for your paid taxes in the other. Further, it does not change the repatriation limit of FEMA, but it impacts how much you keep after taxes.

Additionally, there is a myth that NRE investments are tax-free. The truth is that only the interest you earn on NRE deposits is tax-free. Considering this, whether you invested through NRE or NRO, identically, mutual fund gains are taxed. So, not saving tax on capital gains, the benefit of NRE is unlimited repatriation of funds.

Lastly, understanding the FEMA rules on NRI mutual fund investments is vital if you want to confidently manage your Indian finances. When you follow FEMA rules, you are not only avoiding penalties, but you are also ensuring that your investments are legal, safe, and completely yours.

Further, if you still have any confusion with FEMA rules on NRI mutual fund investments or need help in opening an NRE/ NRO account, connect with Savetaxs. We have a team of tax professionals to help you solve all your doubts and assist you in opening your NRE bank account.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Shubham Jain is the Founder of SaveTaxs and has extensive experience in Indian and NRI taxation. He advises individuals, NRIs, and businesses on tax filing, tax planning, capital gains, DTAA benefits, fund repatriation, and compliance matters. He regularly writes about taxation and related financial topics. His focus is on making complex tax concepts easy to understand. Through his articles, he helps taxpayers stay informed, avoid common mistakes, and stay compliant with Indian tax laws. See Full Bio

Want to read more? Explore Blogs

_1781845771869.webp&w=828&q=75)

_1778936280179.webp&w=828&q=75)

_1778936089630.webp&w=828&q=75)