_1784618918411.webp&w=828&q=75)

NRI Income Tax Compliance

7 Mistakes That Could Trigger an Income Tax Notice for salaried employees7 Mistakes That Could Trigger an Income Tax Notice for salaried employees

Written by Shubham Jain

Upon changing one's status to NRI, many financial and tax regulations change. These changes often lead a new NRI into a state of confusion, uncertainty, and many questions. Among many, one such question that arises most is "Can NRIs continue with a resident savings account"?

In this blog, we will decode this question and provide you with informed insights that help you make informed decisions.

NRIs cannot continue to maintain their regular savings account after acquiring NRI status.

NRIs must immediately convert their regular savings bank account into an NRO account upon a change in residential status.

This conversion is done under the guidelines of the RBI and FEMA to monitor the flow of Indian currency for

When the status of a resident indian changes to a non-resident, they cannot continue with their ordinary resident savings bank account.

The Reserve Bank of India has strictly enforced the regulation requiring NRIs to convert their resident savings bank accounts to non-resident ordinary (NRO) bank accounts or open a specific NRI bank account to carry out any financial transactions in India.

NRIs cannot continue using their regular resident savings accounts due to guidelines from the Reserve Bank of India (RBI) and the Foreign Exchange Management Act (FEMA).

The primary purpose of such regulations is to monitor foreign exchange flows and manage the Indian currency effectively.

Additionally, NRIs cannot use their regular savings account, as hefty penalties await them if they continue to do so. Penalty for not converting to an NRO account is:

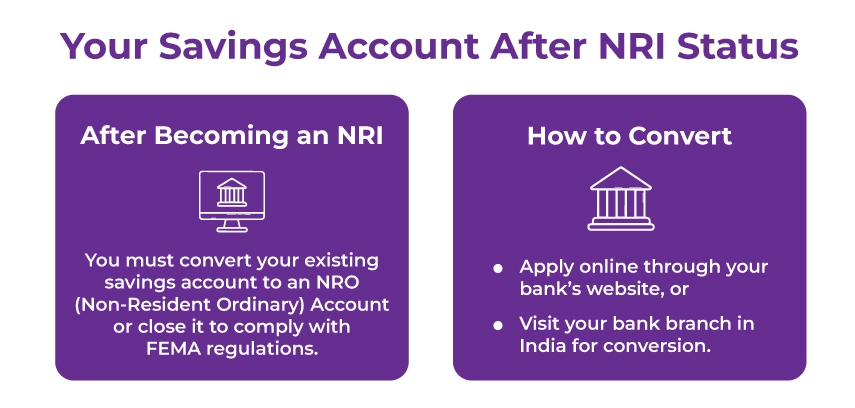

Upon attaining NRI status, an individual must immediately convert their existing savings bank account to an NRO (Non-Resident Ordinary) bank account or close it to comply with FEMA regulations.

This conversion of the bank account is mandatory and should be done either online through the bank's website or in person while in India.

An NRO account (Non-Resident Ordinary Account) is a rupee-denominated account for NRIs to manage income earned in India. This earned income could include rent, dividends, pensions, and other domestic earnings.

In this account, deposits can be made in both Indian and foregin currency, but can be withdrawn only in INR.

An NRE account is a Non-Resident External account, and it is also a rupee-denominated account for NRIs to manage their foregin earnings in India. You can easily repatriate the funds, including both national and interest, back to your country of residence from this account without any restrictions.

Additionally, under the relevant regulations of the Income Tax Act, interest earned on the NRE account is tax-exempt.

The following sections effectively summarize the differences between NRE and NRO bank accounts.

| Basis | NRE Accounts | NRO Accounts |

|---|---|---|

| Defination | An NRE account helps NRIs to park their foreign earning in India in Indian currency. | An NRO account helps NRIs to park their earnings from India in Indian denomination. |

| Taxation | Deposited amounts in NRE accounts are tax-exempt; that is, both the principal amount and the interest earned here are exempt from taxes. | Interest earned on NRO accounts is subject to taxes. |

| Repatriation | Both principal and interest from the NRE account are easily repatriable without limits. | Funds from an NRO account can be repatriated only after applicable taxes are paid. Additionally, the repatriation limit is set at USD 1 million per financial year. |

| Suitable Conditions | You should open an NRE account if you want to maintain or hold your foreign earnings in India in Indian currency. NRE accounts are also a great pick if you want to keep your savings liquid. | As an NRI, if you want to save your earnings from India in Indian currency itself, then an NRO account is needed. |

| Holding Structure | The holding structure of the NRE account is that you can open it with another NRI and close a relative resident Indian. | You can open an NRO account with an NRI as well as any Indian resident. |

To convert your regular savings bank account into an NRO account, please follow the steps below.

Step 1: Connect with the customer care executive at the bank where you have your existing savings account. The bank will provide you with a form to convert your savings account into an NRO account.

In addition, you can download the savings account conversion form from the bank's official website.

Step 2: Fill in all required details in the form, then submit it to the bank. If you have any other accounts with the bank, such as an FD account, a recurring deposit account, or a tax account, please ensure that these details are also provided.

Step 3: Attach all the documents that are required to prove your NRI status. Additionally, your bank may ask you to have your documents attested by the Indian embassy in your new country.

Step 4: Lastly, collect the acknowledgment slip and wait for our bank's confirmation. After a few working days, your resident savings account will be converted to an NRO account.

The following documents are required to convert your existing account to an NRO account with your bank.

However, please note that this list is indicative, and your bank may request additional documents to process your savings account conversion application.

As an NRI, understanding your financial and taxation implications is essential. And with the conversion of your resident account to an NRO account, a lot of information and documentation are missing, which makes the process troublesome and lengthy for many.

Hence, to make things simpler, Savetaxs is here to rescue you. Whether you want to open a new NRO/NRE account or convert your existing one, connect with us, and our experts will help you out.

Savetaxs serves its clients 24/7 across all time zones, so that no client of ours has to wait for their issues to be addressed.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Shubham Jain is the Founder of SaveTaxs and has extensive experience in Indian and NRI taxation. He advises individuals, NRIs, and businesses on tax filing, tax planning, capital gains, DTAA benefits, fund repatriation, and compliance matters. He regularly writes about taxation and related financial topics. His focus is on making complex tax concepts easy to understand. Through his articles, he helps taxpayers stay informed, avoid common mistakes, and stay compliant with Indian tax laws. See Full Bio

Want to read more? Explore Blogs

_1784617942800.webp&w=828&q=75)

_1784547039242.webp&w=828&q=75)

_1784546974133.webp&w=828&q=75)