_1784547039242.webp&w=828&q=75)

NRI Income Tax Compliance

30+ Important Income Tax Terms in India You Need to Know30+ Important Income Tax Terms in India You Need to Know

Written by Shubham Jain

Understanding the tax deduction at source (TDS) implications when purchasing a property in India from an NRI is essential. This is because these TDS rules can be complex, and failing to comply with them might result in legal complications and penalties.

If the seller is an NRI, the TDS is deducted under Section 195 of the Income Tax Act. This section has different rules from Section 194-IA (resident seller). In this guide, we will cover all the essential information about TDS on property purchases from NRIs.

Whether you are an NRI seller, an NRI buyer, or an Indian resident buying a property from an NRI seller, understanding the TDS regulations will help ensure that the entire property transaction process goes smoothly.

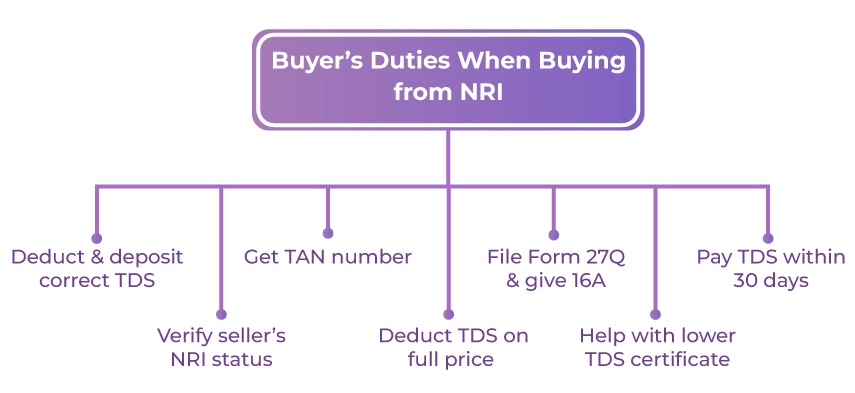

The buyer is responsible for deducting and depositing the correct TDS amount with the Income Tax Department. Along with this, the buyer must verify the seller’s residential status and ensure compliance with foreign exchange regulations.

Here are some important responsibilities for buyers purchasing property from an NRI:

Before buying, confirm whether the seller is a resident indian or a non-resident Indian (NRI). Doing so will help you apply the corrected TDS rate, as the TDS rates for both the resident seller and the non-resident are different.

A Tax Deduction and Collection Account Number (TAN) is mandatory for anyone deducting TDS under Section 195.

Unlike resident transactions, where TDS is deducted only on capital gains, for NRI sellers, TDS is deducted on the entire sale consideration.

The buyer must file Form 27Q and issue Form 16A (TDS certificate) to the seller as proof of TDS deduction.

Buyers may assist the NRI seller in obtaining a Lower Deduction Certificate (LDC). This helps reduce unnecessary TDS deductions.

TDS must be deposited with the Government of India within 30 days from the end of the month of deduction. Delays may attract penalties.

NRIs face higher TDS rates compared to resident Indians. To avoid high deductions, NRIs can apply for a Lower TDS Certificate under Section 197 of the Income Tax Act.

This allows TDS to be deducted only on the capital gains, not on the entire sale value.

Without this certificate, the TDS for NRI property sale is usually deducted at 12.5% to 14.95%, leading to blocked funds and long refund cycles.

To apply for the LDC, an NRI must file Form 13 and submit:

The processing time for an LDC is usually 4 to 6 weeks, so applying early is recommended.

Below is an example showing the TDS calculation where an NRI sells a property in India for ₹3 crore, purchased earlier for ₹1 crore, resulting in a capital gain of ₹2 crore.

Example of tax rates for NRIs on property sale

| Particulars | Amount |

|---|---|

| Sale Price of Property | Rs 3,00,00,000 |

| Capital Gain | Rs 2,00,00,000 |

| LTCG Tax at 12.5% | Rs 25,00,000 |

| Surcharge (10%) | Rs 2,50,000 |

| Cess (4%) | Rs 1,00,000 |

| Total Tax Liability | Rs 29,00,000 |

| TDS Deducted at 14.95% | Rs 44,85,0000 |

| Excess TDS | Rs 15,85,000 |

| Refundable to NRI | Rs 15,85,000 |

In this case, the buyer deducts TDS of ₹44.85 lakh on the full sale price. Since the actual tax liability is ₹29 lakh, the NRI is eligible for a refund of ₹15.85 lakh through ITR filing or by obtaining a Lower TDS Certificate.

To repatriate property sale proceeds outside India, these conditions must be met:

NRIs must complete:

NRIs can repatriate up to USD 1 million per financial year outside India.

Non-compliance with TDS regulations can result in:

Buying property from an NRI seller requires TDS compliance under Section 195 of the Income Tax Act to avoid penalties. Buyers must be aware of the NRI TDS rates, must have a TAN, and should comply with all NRI TDS filing requirements.

However, for expert-backed guidance on TDS on NRI property transactions, TDS planning, or the sale of property by an NRI in India, consult with Savetaxs. Our experts bring more than 30 years of hands-on experience specializing in NRI tax compliance and cross-border property-related matters.

So connect with Savetaxs today as we serve our clients with the best services 24/7 across all time zones.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Shubham Jain is the Founder of SaveTaxs and has extensive experience in Indian and NRI taxation. He advises individuals, NRIs, and businesses on tax filing, tax planning, capital gains, DTAA benefits, fund repatriation, and compliance matters. He regularly writes about taxation and related financial topics. His focus is on making complex tax concepts easy to understand. Through his articles, he helps taxpayers stay informed, avoid common mistakes, and stay compliant with Indian tax laws. See Full Bio

Want to read more? Explore Blogs

_1784546974133.webp&w=828&q=75)

_1784376356528.webp&w=828&q=75)

_1784375756402.webp&w=828&q=75)