Investment & Financial Planning

FCNR Deposit Interest Rates in 2026FCNR Deposit Interest Rates in 2026

Written by Hatim Dudhiyawala

Mutual funds, whether for residents or NRIs, are popular investment options to increase their wealth. Today, investors have a range of equity mutual fund options, and two categories that often come into comparison are multi cap and flexi cap funds. Both the funds across different market capitalizations provide diversified exposure to investors. However, their allocation of assets differs, making each perfect for market scenarios and the needs of investors.

Confused between the two funds? To help you out in this blog, we have done a comparison between the multi-cap and flexi-cap funds. So read on and choose the fund that suits your financial and investment goals.

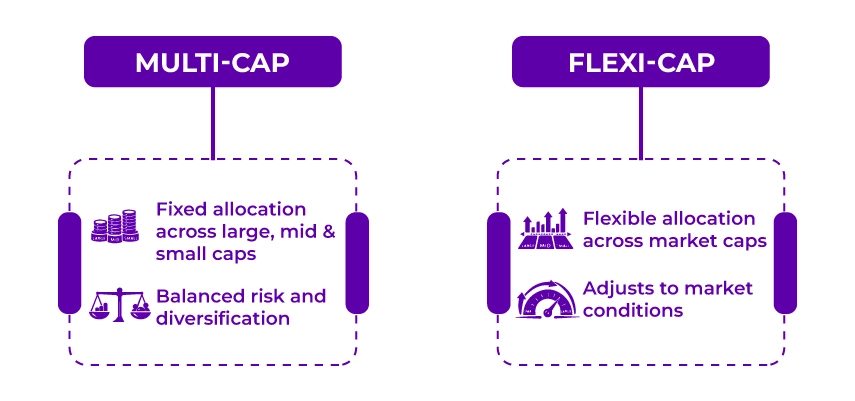

Multi-cap funds are a type of mutual fund that allows investors to invest in several capitalization styles, such as large-cap, mid-cap, and small-cap stocks. Investment in these funds by including companies of several sectors and sizes provides diversification to your portfolio. These funds from large to small-cap stocks spread investment across the market. Further, by balancing exposure to different parts of the market, it reduces the risk.

Additionally, according to the new guidelines of the Securities and Exchange Board of India (SEBI), multi cap funds should hold a minimum of 75% of their assets in equity and equity-related instruments. As per the regulations, the fund manager needs to allocate a minimum of 25% of its assets to large-cap stocks, 25% to mid-cap stocks, and 25% to small-cap stocks.

Also, based on the market conditions, optimizing opportunities and risk management, fund managers have the right to adjust the portfolios. To effectively navigate the market dynamics, these funds offer a well-rounded and flexible investment approach. Since these funds aim to balance return and risk, they are ideal investment options for NRIs with several investment timelines and risk preferences.

So, this was all about multi cap funds. Moving ahead, now let's know about flexi cap funds.

As the name states, flexi cap funds, in terms of investment, are flexible. You can invest in these funds in any market capitalization, i.e., large, mid, or small stocks. These funds provide opportunities to investors to invest across various companies of different capitalization and spread their investments. It further reduces unpredictability and risk.

Additionally, the freedom of asset allocation helps the fund managers to reduce the risk in downturns and increase benefits in bullish markets. This approach provides diversification and flexibility to investors that assist them in effectively managing risk. Further, according to the SEBI guidelines, flexi cap funds should invest a minimum of 65% of their assets in equity and equity-related instruments.

This was all about flexi cap funds. Moving further, let's know about the key differences between the two mutual funds.

With expert guidance, file your ITR on time without any hassle and maximize your returns.

The table below showcases the key differences between the multi cap and flexi cap mutual funds:

| Sr. No. | Particulars | Multi Cap Funds | Flexi Cap Funds |

|---|---|---|---|

| 1. | Meaning | Equity funds that invest across large-cap, mid-cap, and small-cap stocks. | Without any restrictions, equity funds invest across large-cap, mid-cap, and small-cap stocks. |

| 2. | Equity Allocation | 75% of the assets should be allocated to equity and equity-related instruments. | 65% of the assets should be allocated to equity and equity-related instruments. |

| 3. | Asset Allocation Requirement | 25% each to large-cap, mid-cap, and small-cap stocks. | Not needed to follow specific rules and regulations on how to divide the investments among different company sizes. |

| 4. | Suitable For | Investors with a long investment horizon and a higher risk appetite. | Ideal investment option for moderate investors seeking to create wealth over a long time. |

| 5. | Risk Profile | Due to fixed asset allocation to small-cap stocks, the risk profile is high. | Compared to multi-cap funds, flexi-cap funds have less risk due to the active allocation decisions of the fund manager. |

| 6. | Benefits | Across different market caps, it offers potential returns and diversification. | It has the potential for higher returns, offers flexibility, and the capability to adapt to market dynamics. |

| 7. | Taxation Implications | Based on the holding period and types of capital gains, taxation follows applicable norms. | Tax is imposed on the basis of holding periods and capital gains taxation norms. |

These were the key differences between multi cap and flexi cap funds for NRIs. Moving ahead, let's know the tax implications of these funds.

The tax implications of multi-cap and flexi-cap funds on NRIs are as follows:

| Type of Capital Gain | Holding Period | Tax Rate | Notes for NRIs |

|---|---|---|---|

| Short-Term Capital Gains (STCG) | Less than 12 months | 15% | Tax deducted as source (TDS) is deducted at the time of redemption. |

| Long-Term Capital Gains (LTCG) | More than 12 months | 10% on capital gains more than INR 1,00,000 | TDS is applied during redemption. However, if applicable, NRIs can claim DTAA benefits. |

This was all about the tax implications faced by NRIs in India on multi cap and flexi-cap funds. Moreover, as per the Budget 2024 Amendments, some recent changes have been made, effective from July 23, 2024. It showcases a potential increase in STCG to 20%. Additionally, LTCG at 12.5% on the amount more than INR 1,25,000. The two funds are taxed as equity funds.

Now, moving further, let's know which funds NRIs should choose for investment.

Connect with Savetaxs for expert NRI investment planning and make your savings work for you.

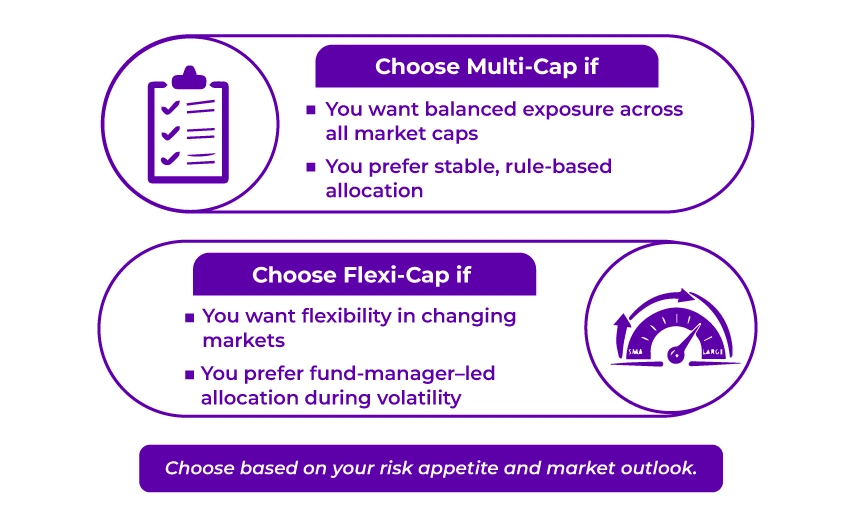

Selecting between multi-cap and flexi-cap funds depends on the financial goals and situation of the NRIs. Considering this, here to help you out, we have mentioned certain situations as per each fund to choose from:

These were some of the circumstances where NRIs can opt for multi-cap or flexi-cap funds.

Lastly, multi-cap funds are a suitable choice for NRI investors who have a long-term investment horizon and a higher risk appetite. It generally offers structured exposure to all market caps, which in bullish markets provide strong returns. On the other hand, felxi cap funds are suitable for NRIs seeking a balanced risk approach, additionally, for those who, during the changing market conditions, value active fund management. Considering this, an NRI should select a fund that matches their investment objectives.

Further, if you still have confusion about which investment option you should choose, connect with Savetaxs. Our financial experts assist you in choosing the right investment as per your financial goals, risk appetite, and time horizon.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Shubham Jain is the Founder of SaveTaxs and has extensive experience in Indian and NRI taxation. He advises individuals, NRIs, and businesses on tax filing, tax planning, capital gains, DTAA benefits, fund repatriation, and compliance matters. He regularly writes about taxation and related financial topics. His focus is on making complex tax concepts easy to understand. Through his articles, he helps taxpayers stay informed, avoid common mistakes, and stay compliant with Indian tax laws. See Full Bio

Want to read more? Explore Blogs

_1781845771869.webp&w=828&q=75)

_1778936280179.webp&w=828&q=75)

_1778936089630.webp&w=828&q=75)