US Tax Filing and Compliance

Substantial Presence Test Explained: How NRIs Determine US Tax Residency?Substantial Presence Test Explained: How NRIs Determine US Tax Residency?

Written by Shubham Jain

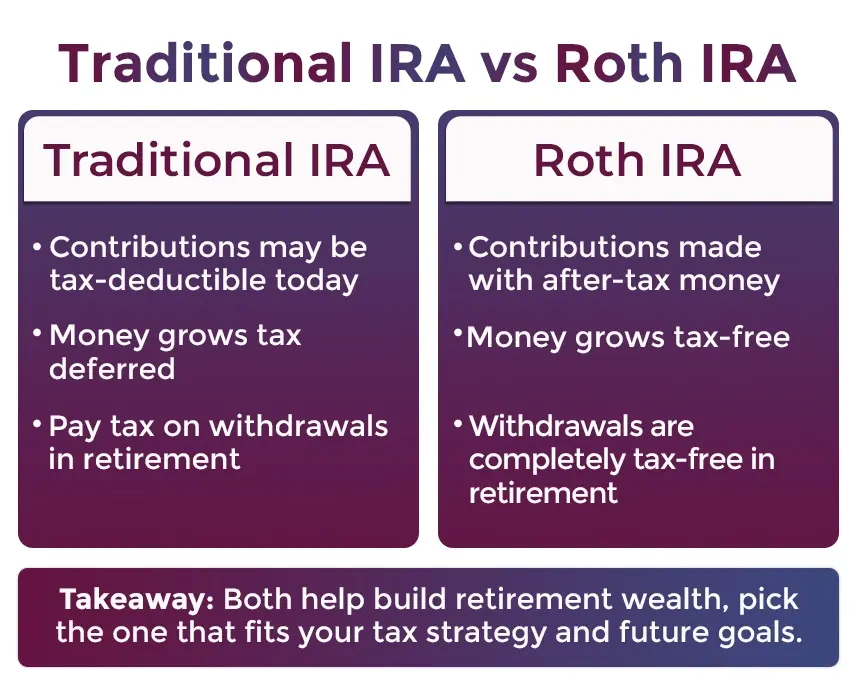

The traditional IRA Tax deduction offers two key benefits to retirement savers. The first is that it offers you a tax deduction on your contributions made towards your IRA accounts. The second benefit is that you do not need to pay tax on your growing investment until you make the withdrawal. Thus, both benefits together reduce your tax liabilities.

However, not every contribution you make towards a traditional IRA offers you tax benefits. It is available to high-income individuals and employees who have a retirement plan at work. Additionally, it depends on your tax filing status. In this blog, you will get all the information about the traditional IRA tax deduction. So, read on and know about them in detail.

Yes, generally, the traditional individual retirement accounts (IRA) are tax-deductible. It helps you to decrease your tax obligations dollar for dollar by your contribution amount made towards an IRA. The IRA traditional tax deduction is available on your federal tax return. When filing it, you can claim the contribution.

However, based on the type of IRA and your financial circumstances, the IRA tax deduction rules vary. For example, compared to Roth IRA contributions, traditional IRA contributions are tax-deductible.

Moving further, let's know about them in more detail.

Compared to the traditional IRA tax deduction, the Roth IRA tax contribution is not tax-deductible. However, in your retirement, Roth IRA contributions offer you several benefits. It includes tax-free withdrawals, tax-free investment growth, and no required minimum distributions (RMDs).

The Roth IRA tax deduction is determined based on your tax filing status and modified adjusted gross income (MAGI).

Like the Roth IRA contribution, the traditional IRA tax deduction depends on your tax filing status and MAGI. Additionally, the traditional IRA contribution limits also depend on whether you or your spouse has a workplace retirement plan. These are the following conditions for it:

This was all about Roth and traditional IRA tax deduction. Moving further, let's know the traditional IRA contribution limits for 2024-2025.

Non-resident aliens can also claim a traditional IRA tax deduction in the US. However, for this, they need to have "Effectively Connected Income" (ECI) in the US. It is because the traditional IRA tax deduction applies to the ECI portion of their gross income. Additionally, the IRA contribution should be made with the earned ECI.

Since every year the IRS updates the tax deduction limits for most tax filers. Considering this, it is vital to know the taxpayer whether or not their contribution amount is deductible or not based on their income or filing status for the year. Here, the table below shows the 2024 and 2025 traditional IRA deduction limits:

| Tax Deductibility of Traditional IRA Contributions for Tax Year 2024- 2025 | |||

|---|---|---|---|

| Status | Modified Adjusted Gross Income (MAGI) 2025 | Modified Adjusted Gross Income (MAGI) 2024 | Traditional IRA Tax Deduction Allowed |

|

Single |

$79,000 or less |

$77,000 or less |

Complete tax deduction on IRA contribution of up to $7000. Additionally, if yoy are 50 years or older, you receive $800 tax deduction. |

|

Between $79,000 and $89,000 |

Between $77,000 and $87,000 |

Based on your modified adjusted gross income (MAGI) partial tax deduction is available. |

|

|

$89,000 or more |

$87,000 or more |

No tax deduction. |

|

|

Married filing jointly and have a retirement plan at work |

$126,000 or less |

$123,000 or less |

Up to $7000 full tax deduction is available on an IRA traditional contribution. Also, if you are 50 years or older, you can claim up to $8000 tax deduction. |

|

Between $126,000 and $146,000 |

Between $123,000 and $143,000 |

Depending on your modified adjusted gross income (MAGI), a partial tax deduction is available. |

|

|

$146,000 or more |

$143,000 or more |

No tax deduction. |

|

|

Married filing jointly, and the spouse has a retirement plan at work |

$236,000 or less |

$230,000 or less |

You can claim a full deduction of up to $7000 on your contribution. Further, if you are 50 years or older, you can claim up to $8000 on your traditional IRA tax contribution. |

|

Between $236,000 and $246,000 |

Between $230,000 and $240,000 |

Depending on your modified adjusted gross income (MAGI), a partial tax contribution amount is deductible. |

|

|

$246,000 or more |

$240,000 or more |

No tax deduction available. |

|

|

Married filing separately |

Less than $10,000 |

Less than $10,000 |

The partial tax amount is available on your IRA tax contribution based on your modified adjusted gross income. |

|

$10,000 or more |

$10,000 or more |

No tax deduction is available on an IRA contribution. |

|

Here, the deducted amount limit does not impact your annual contribution amount. However, you cannot claim more tax deductions than your contribution to the IRA that year.

Additionally, when choosing an IRA, you should not completely concentrate on whether the contribution is tax-deductible or not. You should also consider other factors. It includes liquidity needs, RMDs, future income projections, legacy goals, and taxes on withdrawals.

This was all about the traditional IRA contribution tax deduction limits of 2024 and 2025. Moving further, let's know what is SEP-IRA contributions tax deduction.

A Simplified Employee Pension (SEP) helps business owners, self-employed individuals, or freelance workers to contribute to a SEP-IRA plan. Further, the contributions to these accounts up to the contribution limit are tax-deductible.

Considering this, the yearly SEP-IRA contribution limits differ from Roth and traditional IRA tax deductions. Additionally, the tax deduction limit of SEP-IRA contribution is the lesser of:

So, it was all about the SEP-IRA contribution tax deduction available for self-employed individuals, business owners, and freelance workers. Moving ahead, let's know how much tax you can save from your IRA contributions.

The traditional IRA tax deduction depends on several factors. It includes:

These were some of the factors that impact your traditional IRA tax deduction savings. Moving further, let's look at the alternatives to the traditional IRA tax.

If you cannot take advantage of the traditional IRA tax deduction, there are other retirement savings options also available. These are as follows:

Considering the above information, if you do not qualify for a traditional IRA tax deduction, you can claim from any of the retirement options.

Lastly, the traditional IRA tax deduction helps you save taxes on your contributions you made to your retirement plan. However, unlike the contribution, the tax deduction is not available for everyone. Several factors, like your tax filing status and income level, decide whether you qualify for it or not.

Here, the complete blog was all about the traditional IRA tax deduction and its contribution limits. Further, if you need any assistance in claiming these tax deductions, connect with Savetaxs. We have a team of tax experts who, with their knowledge, help you claim the deduction and boost your tax savings.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Shubham Jain is the Founder of SaveTaxs and has extensive experience in Indian and NRI taxation. He advises individuals, NRIs, and businesses on tax filing, tax planning, capital gains, DTAA benefits, fund repatriation, and compliance matters. He regularly writes about taxation and related financial topics. His focus is on making complex tax concepts easy to understand. Through his articles, he helps taxpayers stay informed, avoid common mistakes, and stay compliant with Indian tax laws. See Full Bio

Want to read more? Explore Blogs

_1784032485815.webp&w=828&q=75)