Investment & Financial Planning

FCNR Deposit Interest Rates in 2026FCNR Deposit Interest Rates in 2026

Written by Hatim Dudhiyawala

For NRIs, investing in liquid funds is a good option. These funds, while offering accessibility, provide better returns than your savings accounts. With maturity periods of up to 91 days, these liquid debt mutual funds invest in debt and money-market instruments. This makes them a low-risk investment option for NRIs managing their finance across borders.

Further, because of the short lending tenure, among all mutual funds, liquid funds are the safest investment options for NRIs. Still unsure whether to invest in these funds or not? Read the blog to clear up any confusion about the funds and choose the right investment option.

A liquid fund is a specialized type of debt mutual fund. These funds invest in short-term financial instruments with a maximum maturity of 91 days. It offers a balance between returns, safety, and accessibility for NRIs to manage funds across countries.

When you invest in these funds, your money goes into high-quality debt instruments. It includes Certificates of Deposit (CDs), Treasury Bills (T-Bills), Collateralized Lending and Borrowing Obligations (CBLO), and Commercial Papers (CPs). The key objective of these funds is to preserve capital while maintaining high liquidity and offering competitive returns.

Further, these funds concentrate on ultra-short-term securities. Considering this, fund managers certify that the portfolio's average maturity does not exceed 3 months. Compared to other NRI investment options, these significantly reduce both credit and interest rate risk.

In several key aspects, liquid funds function differently from other mutual funds:

This was all about liquid funds. Moving ahead, let's know the reasons why NRIs should invest in these mutual funds.

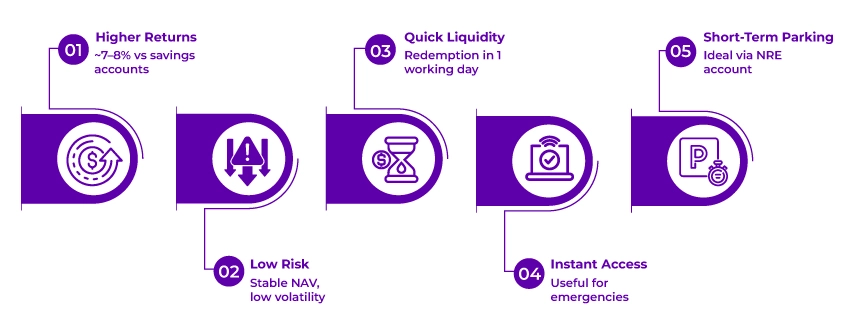

Liquid funds offer several benefits to NRIs that address the unique financial challenges faced by them while managing their funds across borders. Considering this, here are some key reasons why NRIs should invest in liquid funds:

These were some of the key reasons why NRIs should invest in liquid funds. Moving on, let's look at the top-performing liquid funds available to NRIs in India.

Connect with Savetaxs, and start your tax journey hassle-free in India.

The table below showcases the top-performing liquid funds for NRIs and residents:

| Sr. No. | Fund Name | Risk | NAV | Expense Ratio | 3-Year Returns | 5-Year Returns |

|---|---|---|---|---|---|---|

| 1. | Aditya Birla Sun Life Liquid Fund | Moderate | 436.96 | 0.21 | 7.1% | 5.9% |

| 2. | Edelweiss Liquid Fund | Low to Moderate | 3,496.80 | 0.1 | 7.1% | 5.9% |

| 3. | Axis Liquid Direct Fund | Low to Moderate | 3,008.78 | 0.14 | 7.1% | 5.9% |

| 4. | PGIM India Liquid Fund | Low to Moderate | 352.95 | 0.12 | 7.1% | 5.9% |

| 5. | Sundaram Liquid Fund | Low to Moderate | 2,390.56 | 0.13 | 7.1% | 5.9% |

| 6. | Canara Robeco Liquid Fund | Low to Moderate | 3,243.22 | 0.07 | 7.1% | 5.8% |

| 7. | HSBC Liquid Fund | Low to Moderate | 2,695.77 | 0.12 | 7.1% | 5.8% |

| 8. | Nippon India Liquid Fund | Moderate | 6,622.22 | 0.2 | 7.1% | 5.8% |

| 9. | Franklin India Liquid Fund | Low to Moderate | 4,006.71 | 0.13 | 7.1% | 5.8% |

| 10. | Tata Liquid Fund | Low to Moderate | 4,270.66 | 0.2 | 7.1% | 5.8% |

These were some of the top-performing liquid funds available for NRIs to invest in India. Moving ahead, let's know how NRIs can invest in these funds.

Being an NRI, the process of investing in liquid funds includes several straightforward steps that you can complete from overseas.

To invest in liquid funds, you should either have a Non-Resident External (NRE) or Non-Resident Ordinary (NRO) bank account with an Indian bank. In the NRE account, your foreign currency earnings convert to Indian rupees. However, an NRO account manages your income earned within India. This step is important for NRIs, as in India, mutual fund companies cannot accept foreign currency investments.

To invest in liquid mutual funds in India or conduct financial transactions, it is vital to have a PAN card. If you don't have it, first Apply for the PAN Card, then proceed with the investment process.

For all mutual fund investors, it is vital to complete the Know Your Customer (KYC) process. Considering this, you need to provide the following things:

There are two ways by which you can invest in liquid mutual funds, i.e., through the website of the mutual fund or via a registered broker. Considering this, investing directly through the website of the fund house can be cost-effective as it generally charges lower fees. On the other hand, using a broker can provide professional guidance and help you navigate the investment process.

After investing in liquid funds, it is vital to monitor their performance regularly. In this, compare your financial goals to your investments. Monitoring your investments helps you certify that you are on track to fulfill your financial objectives.

This is how NRIs can invest in liquid funds. Moving on, let's look at the tax implications for NRIs.

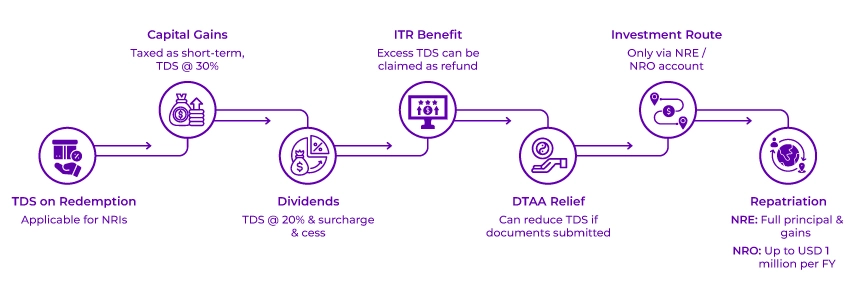

For NRIs, the taxation rules on the liquid funds are the same as for residents. However, Tax Deducted at Source (TDS) is applied at the time of redemption.

Further, using the NRE account, you can fully repatriate the principal and gains amount. However, under the RBI rules for NRI investment, using the NRO account, you can transfer only the capital gain and principal amount up to a specified limit, i.e., USD 1 million per financial year.

Simplify your taxes, investments, and compliance- all in one place with Savetaxs.

Lastly, for NRIs, liquid funds are a superior alternative to traditional savings accounts and fixed deposits. It is because with unfettered access to your invested amount, it combines competitive returns. Additionally, liquid funds are an ideal choice for NRIs seeking immediate financial benefits.

Furthermore, if you need any assistance with your investments in India, contact Savetaxs. We have a team of financial experts who can help you make the right investment decisions. Additionally, they can also help you with your tax obligations in India.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Shubham Jain is the Founder of SaveTaxs and has extensive experience in Indian and NRI taxation. He advises individuals, NRIs, and businesses on tax filing, tax planning, capital gains, DTAA benefits, fund repatriation, and compliance matters. He regularly writes about taxation and related financial topics. His focus is on making complex tax concepts easy to understand. Through his articles, he helps taxpayers stay informed, avoid common mistakes, and stay compliant with Indian tax laws. See Full Bio

Want to read more? Explore Blogs

_1781845771869.webp&w=828&q=75)

_1778936280179.webp&w=828&q=75)

_1778936089630.webp&w=828&q=75)