Investment & Financial Planning

FCNR Deposit Interest Rates in 2026FCNR Deposit Interest Rates in 2026

Written by Hatim Dudhiyawala

For NRIs, NRE Fixed Deposits (FDs) have always remained an easy and safe way to invest in India. With the promise of tax exemption, security, and fixed interest, NRE FDs have remained a popular choice. However, with the change in the global financial landscape, the risk of currency depreciation (INR) and reporting requirements, debt mutual funds have emerged as an alternative for NRIs.

Want to invest in India but are confused between NRE FDs and debt mutual funds? This blog will provide you with a clear and in-depth comparison of both investments and help you choose the one that perfectly matches your financial goals.

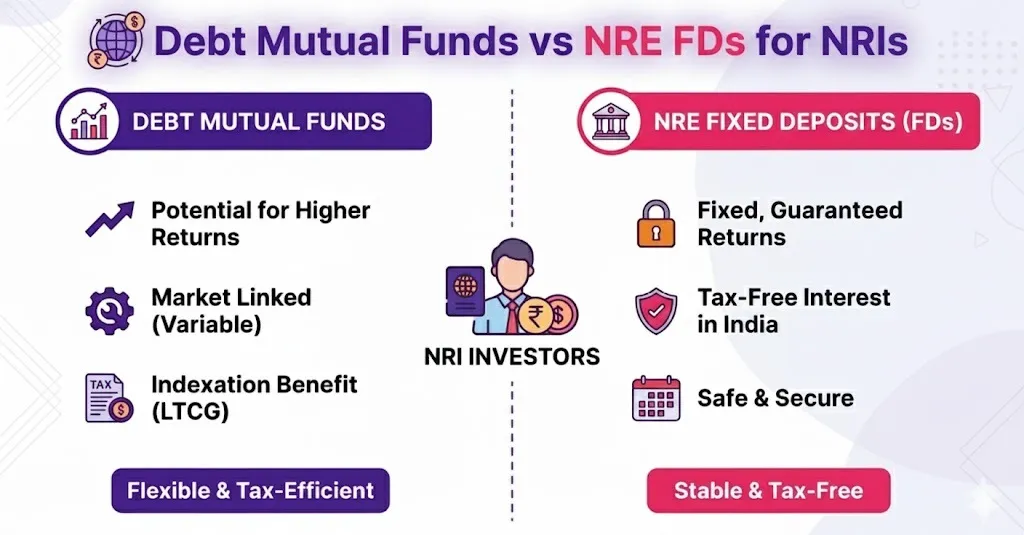

An NRE FD is a type of bank deposit through which NRIs can park their foreign currency earnings in INR and earn interest on them. The earned interest on these FDs is tax-free in India. Additionally, you can transfer the whole amount (principal and interest) to your foreign resident country without any restrictions.

The minimum tenure is one year, and the maximum is 10 years of NRE FDs. Also, depending on the deposited amount and tenure from bank to bank, the interest rates on the FDs vary. Considering this, NRE FDs can offer a maximum of 8% interest.

In simple words, NRE FDs allow you to open an account with an authorized Indian bank, send money from overseas, the bank converts it into Indian rupees, and for 1 to 20 years, you lock it in as a fixed deposit.

This was all about NRE fixed deposits. Moving ahead, let's know about debt mutual funds.

A debt mutual fund is one of the types of mutual funds that invests in fixed securities such as corporate bonds, government bonds, commercial papers, treasury bills, and more. These funds aim to provide a regular income. Additionally, they have the potential for increasing capital.

Further, the debt returns depend on credit quality, interest rates, and maturity of the underlying securities. Also, debt mutual funds are subject to interest rate risk, market risk, and credit risk. Apart from this, depending on the resident country, debt mutual funds are taxed differently.

This was all about debt mutual funds. Moving further, let's know about the key difference between NRE FDs and debt mutual funds.

Simply file your taxes without an issue with the expert guidance of Savetaxs and maximize your returns.

The table below with various parameters summarises the key difference between NRE FD and debt mutual funds:

| Sr. No. | Basis | NRE Fixed Deposits (FDs) | Debt Mutual Funds |

|---|---|---|---|

| 1. | Return Potential | NRE FDs offer fixed and guaranteed returns. | Debt mutual funds provide fixed but not guaranteed returns based on the changing market conditions. |

| 2. | Investment | Lump sum | Lump sum or Systematic Investment Plan (SIP) |

| 3. | Interest/ Return | 4.5% to 8% | 8% to 10% |

| 4. | Risk | Low | Low to moderate |

| 5. | Tenure | 1 to 10 years | No minimum investment tenure |

| 6. | Lock-in Period | Duration of the fixed deposit | No lock-in period |

| 7. | Investment Horizon | Short to long-term | Short to medium-term |

| 8. | Minimum Investment | INR 1,000 to INR 20,000, varies from bank to bank | INR 500 |

| 9. | Liquidity | With a penalty, premature withdrawal is allowed | Without penalty, anytime redemption is allowed |

| 10. | Diversification | In a single fixed deposit, a limited investment | Diversified portfolio of debt securities |

| 11. | Taxation | Interest rate is tax-free in India | According to your income slab rate, Capital Gains are taxed |

| 12. | Expense | No additional charges | As the expense ratio, the fees of fund management are charged by the asset management company |

| 13. | Repatriation | You can freely repatriate the principal and interest amount | After the tax payment, principal and capital gains can be repatriated |

| 14. | Currency | Foreign currency earnings in INR | Indian rupees |

| 15. | Deposit Insurance and Credit Guarantee Corporation (DICGC) | Under DICGC, capital + interest valued at INR 5,00,000 can be insured | No insurance available |

| 16. | Loan | Against your FD, you can take a loan | Up to 80% of your investment value, you can take a loan. However, it can vary as per the lender. |

| 17. | Inflation Protection | Limited | Over the long term, it has the potential to beat inflation |

| 18. | Regulatory Body | Regulated by the Reserve Bank of India (RBI) | Debt mutual funds are regulated by the Securities and Exchange Board of India (SEBI) |

These were the key differences between NRE FDs and debt mutual funds for NRIs. Moving ahead, let's know about the NRE FDs vs the debt mutual fund, which is the better investment option for NRIs.

Choosing between NRE FD and debt mutual funds depends on investment horizon, risk appetite, and return expectations. Further, to help you out, here are some guidelines that help you choose the right investment option as per your financial goals:

So, according to your financial goals and mentioned scenarios, you can choose among the NRE FDs and debt mutual funds. Now, moving further, important factors NRIs should consider when choosing NRE FDs or debt mutual funds.

Connect with Savetaxs, and avail expert services on tax, repat, investment, and more.

The choice between NRE FDs and debt mutual funds completely depends on your financial goals, resident country, and taxation laws. Considering this, here are some important factors NRIs should consider while selecting from both the investments:

These are some of the factors that NRIs should consider while choosing between NRE FDs and debt mutual funds.

Lastly, among NRE FD and debt mutual funds for NRIs, which is better, does not have a proper answer. Both have them have their own benefits, features, and drawbacks. While NRE FDs are good for NRIs living in countries that charge zero tax on foreign income, debt mutual funds are a perfect investment that offers after-tax benefits for those who live in tax-paying countries. Considering this, among both the investment options, choose the one that matches your financial goals, risk appetite, tax situation, and return expectations.

Further, if you need any assistance in choosing the right NRI investment option, connect with Savetaxs. With a deep understanding of tax regulations, global compliance requirements, and investment options, our experts help you choose the right investment options. So contact us today and maximize your returns while staying compliant with the tax laws in both India and overseas.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Shubham Jain is the Founder of SaveTaxs and has extensive experience in Indian and NRI taxation. He advises individuals, NRIs, and businesses on tax filing, tax planning, capital gains, DTAA benefits, fund repatriation, and compliance matters. He regularly writes about taxation and related financial topics. His focus is on making complex tax concepts easy to understand. Through his articles, he helps taxpayers stay informed, avoid common mistakes, and stay compliant with Indian tax laws. See Full Bio

Want to read more? Explore Blogs

_1781845771869.webp&w=828&q=75)

_1778936280179.webp&w=828&q=75)

_1778936089630.webp&w=828&q=75)