Child Tax Credit - Meaning, How Does It Work And Who Qualifies

Read More

Do you know that interest is often tax-deductible when it comes to mortgages and taxes? This is true if the loan fulfills the IRS mortgage rules, helping you reduce your taxable income. You might get the option to deduct interest paid on your mortgage and any local or state property taxes you have paid during the year.

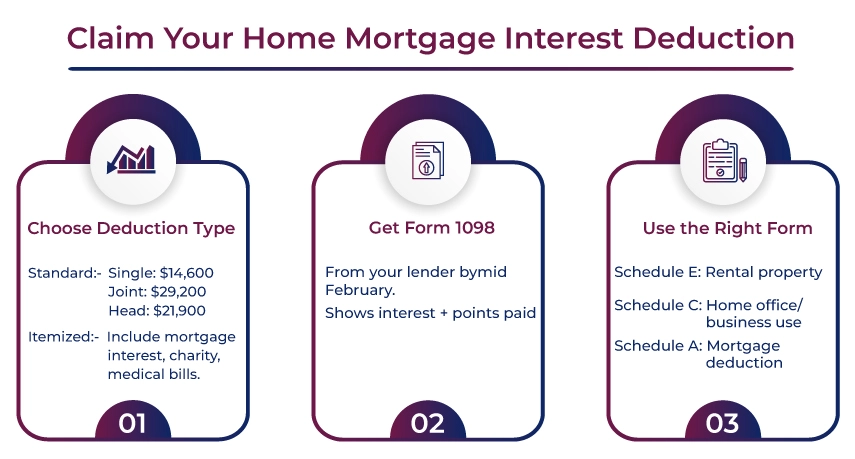

The deductible amount of mortgage interest is reported annually by the mortgage company on Form 1098. If you also wish to maximize your savings, keep reading this blog. We will determine whether you qualify for the deduction and also learn how to claim the mortgage tax deduction.

While repaying a mortgage loan, do you know that most of the payments are interest? Yes, it's true in the first few years. Even after that, the loan's interest can still be a significant portion of your payments. However, if the loan fulfills the IRS mortgage requirements, you can deduct the interest paid by you.

The mortgage company reports the amount of deductible mortgage interest on Form 1098. It is then sent to the homeowners. The federal government offers this tax benefit to homeowners to make homeownership more affordable. However, to claim the mortgage tax deduction, you must itemize deductions.

A non-resident alien (NRA) in the US will qualify to claim a mortgage interest deduction based on whether the income from the property is “effectively connected” with a U.S. trade or business. They must itemize on Form 1040-NR to claim a deduction and are not allowed to take the standard deduction.

When you file a tax return, you get the option to deduct interest from your mortgage payments. However, this option only applies if the loan is secured by your home. Additionally, you must utilize the loan proceeds for the specified purpose. It means the proceeds must have been used to buy, build, or improve your main residence.

Furthermore, it can be used for the other home you own and for personal reasons. Now, renting out your second home to a tenant doesn't count as a personal purpose. Therefore, it doesn't qualify for the mortgage interest deduction on your tax return. However, if you use the rental home as a residence for 15 days or more every year. Also, use it as a residence for over 10% of the days you rent it to tenants. Then, the rental home will qualify for the mortgage interest deduction.

The IRS puts forward numerous limits on the interest amount that you can deduct annually on your tax return. Here are the limits for the mortgage tax deduction:

Mortgage discount points, also known as prepaid interest, are fees that you pay during closing to acquire a lower mortgage rate. Generally, these costs can be deducted in the year you purchase the home. If not, you can subtract them pro rata over the repayment period.

For instance, if you pay $3,000 in points to acquire a lower mortgage rate. Then, you can increase your mortgage interest deduction by $3,000 in the tax year you close on the home.

Follow the steps below to claim your home mortgage interest deduction:

You can pick from numerous deductions if you opt for an itemized deduction. It includes charitable donations and medical expenses. You must fill out additional forms to choose this option. Additionally, you must provide evidence for each deduction. Both types of deduction will reduce your taxability:

Example of mortgage interest deduction decision-making

The decision between itemizing and the standard deduction depends on which offers more savings. Consider opting for a single filer with the following deductions:

The total of these two is $12,000. In this example, opting for the $14,600 standard deduction (2024) would be better. It cuts taxable income by an additional $2,600. However, if the mortgage interest was $13,000 and the charitable contributions were $3,000, the total is $16,000.

In such a case, choosing itemized deductions would be beneficial. It would reduce your tax liability by an additional $1,400 beyond the standard deduction.

The mortgage tax deduction allows homeowners to reduce their taxable income. Under the Tax Cuts and Jobs Act of 2017, the limit on the mortgage interest deduction was reduced from $1 million to $750,000. It means you can now claim the deduction on the first $750,000 of the mortgage instead of the first $1 million.

Remember, it is not a mandatory deduction. However, failing to deduct your mortgage interest can lead to a higher tax liability, as you may lose out on a valuable tax benefit. Also, the financial repercussions depend wholly on whether itemizing their deductions saves them more money.

Furthermore, if you need assistance with your mortgage interest deduction, contact an expert. When it comes to experts, Savetaxs tops the list. We have been helping individuals with their tax-related queries for over a decade now. We assure that your queries will be handled with utmost precision. Our team of experts is working 24*7 across all time zones. So, connect with us right away to avoid having to claim deductions as a stressful thing.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Mr. Ritesh has 20 years of experience in taxation, accounting, business planning, organizational structuring, international trade financing, acquisitions, legal and secretarial services, MIS development, and a host of other areas. Mr Jain is a powerhouse of all things taxation.

Want to read more? Explore Blogs

_1758631896.webp&w=828&q=75)

Below is the limit of mortgage debt that qualifies for the deduction: