_1782391419380.webp&w=828&q=75)

US Tax Filing and Compliance

Missed the Tax Deadline? 3 Reasons to File Your Late Tax Return TodayMissed the Tax Deadline? 3 Reasons to File Your Late Tax Return Today

Written by Hatim Dudhiyawala

-in-the-USA_1762862398.webp&w=3840&q=75)

The TRC is an official document issued by the IRS (Internal Revenue Service), referred to as Form 6166 in the United States. The certificate is used to certify that an individual or an entity is a resident of the US for tax purposes

This certificate is non-negotiable as it allows taxpayers to claim benefits under a DTAA between the U.S. and India (or other nation). Keep reading to learn more about a Tax Residency Certificate in the United States.

The U.S. Tax Residency Certificate (Form 6196) is an official document issued by the IRS. The document certifies that you or your company is a resident of the US for income tax purposes

When claiming the tax treaty benefits, the TRC will serve as documented evidence for foreign tax authorities. An NRI who is seeking to lower their taxability and avail the benefit of the DTAA provision must obtain a TRC

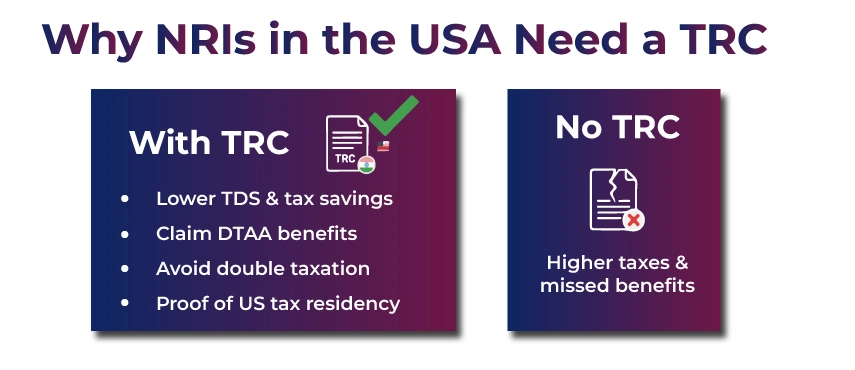

A TRC for NRIs is crucial who wish to claim the benefits of the DTAA treaty. Here are the reasons why an NRI in the USA needs a tax residency certificate:

If you don't have a TRC, you might attract higher tax rates, miss out on significant tax savings, and also lose the opportunity to plan NRI taxation effectively.

You need to fulfill some eligibility requirements to apply for a TRC in the USA. Here are the eligibility criteria for an individual and an entity:

You may qualify if you are:

U.S. entities must:

There are situations when you might not be eligible to apply for a TRC, such as:

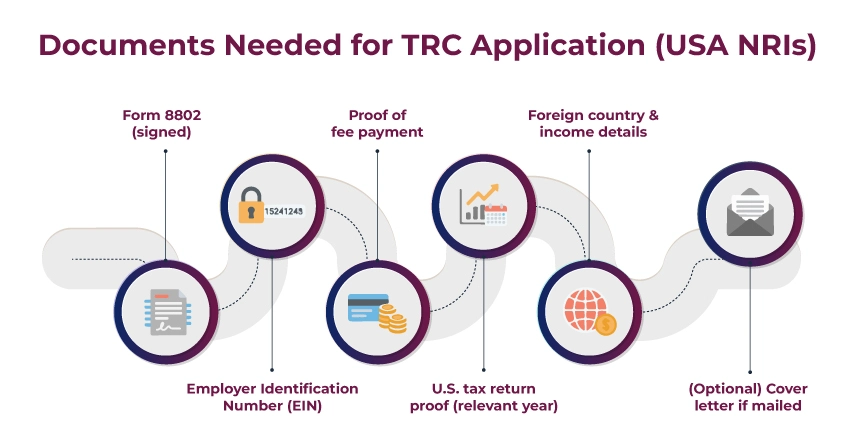

You need to provide some documents to obtain a TRC to verify your identity, confirm your residency for eligibility, and ensure compliance with the legal and tax regulations. Here are the documents you need to submit:

Follow these steps to apply for TRC from the IRS in the United States:

Let's understand how to use a TRC to claim the benefits of DTAA with an example of Suresh.

Suresh is an NRI who resides in the US and earns Rs. 10,00,000 in India through investments. Generally, NRIs are taxed at 30% in India, which would be Rs. 3,00,000. Now, since his global income is taxable in the US, which includes his Indian income, also.

So, he will obtain a TRC to claim the benefits of the DTAA to avail reduced tax rates and pay less taxes. Under the India-US DTAA, his interest or investment may be taxed at a lower rate of 10% instead of 30%.

He will obtain a TRC from the US tax authorities to prove his tax residency in the U.S. After that, he will submit the TRC along with Form 10F with his Indian ITR (Income Tax Return) to claim the DTAA benefits. In short,

Submitting a TRC will ensure that Suresh pays reduced tax in India legally and avoids double taxation on the same income.

A TRC (Tax Residency Certificate) is usually valid for one financial year only and must be renewed every year. For example, if you apply for a TRC in 2025 and request a certificate for 2024, then it will remain valid for the entire 2024.

You will have to file Form 8802 every year because Form 6166 is only valid for one year. This will ensure that you keep getting uninterrupted benefits, particularly if you keep receiving foreign income annually.

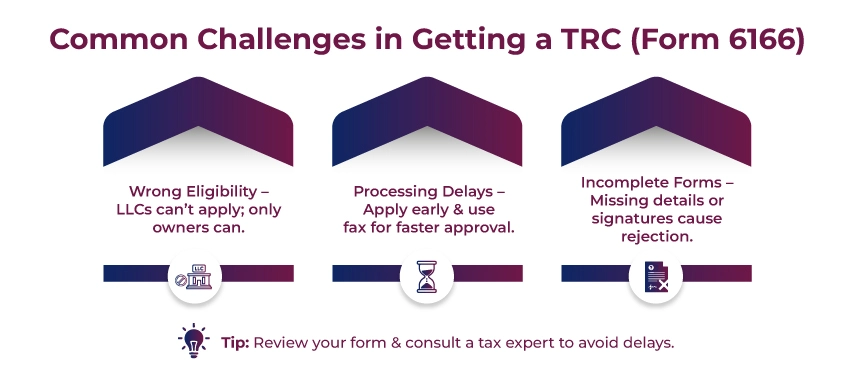

Applying for Form 6166 is straightforward and not difficult. However, an NRI might face some common pitfalls while obtaining a TRC, including:

A lot of LLCs apply for a TRC mistakenly without understanding that disregarded entities are not allowed to apply directly. Instead, their owner is required to do the same.

If you are not sure about your eligibility, you must consult a qualified tax advisor to stay compliant.

Some factors may affect the processing time of your TRC application, including:

How to Avoid: Try to apply early in the year to avoid delays and use fax in case you need the certificate on a specific deadline, and speed is essential.

Missing signatures or sections, not attaching a tax return, can lead to delays or even application rejection.

How to Avoid: Always ensure to cross-check your application before submitting it further.

A TRC is essential for an NRI to lower tax liability and prevent double taxation. Understanding the eligibility criteria, application process, and renewal needs can ensure that NRIs comply with Indian and international tax laws. Form 6166 serves as a passport to international tax savings.

Furthermore, if you are unaware of the TRC requirements and need guidance on NRI taxation, consult the experts at Savetaxs. We have a team of professionals with years of experience in this field, who can help you reduce your tax liability and ensure full compliance

By now, we are serving thousands of clients across the USA, UAE, UK, Australia, and more. So, contact us right away as we are working 24*7 across all time zones to assist NRIs with their financial planning and tax obligations

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Shubham Jain is the Founder of SaveTaxs and has extensive experience in Indian and NRI taxation. He advises individuals, NRIs, and businesses on tax filing, tax planning, capital gains, DTAA benefits, fund repatriation, and compliance matters. He regularly writes about taxation and related financial topics. His focus is on making complex tax concepts easy to understand. Through his articles, he helps taxpayers stay informed, avoid common mistakes, and stay compliant with Indian tax laws. See Full Bio

Want to read more? Explore Blogs

_1782129946793.webp&w=828&q=75)