Investment & Financial Planning

FCNR Deposit Interest Rates in 2026FCNR Deposit Interest Rates in 2026

Written by Hatim Dudhiyawala

Everyone, whether it is an Indian resident or an NRI, dreams of generating a substantial monthly income to substitute for or support a salary or other income. This dream can only be fulfilled when earning a meaningful return through a significant corpus for lump sum investment.

Considering this, the financial services industry provides two main routes in this, i.e., monthly income plans (MIPs) and systematic withdrawal plans (SWPs). At first glance, both look the same but are different. Further, to provide you better idea, we have compared the monthly income plan vs SWPs and which is the better option for NRIs. So read on and gather all the information about it, and make the right investment decision.

Monthly Income Plan, popularly known as MIP, is a type of mutual fund that offers regular income to investors by primarily investing in debt instruments with a small portion given to equities. MIPs are like Time Deposits or Fixed Deposits (FDs), where an investor needs to invest in lump sum. However, unlike FDs, where you have to wait for the completion of the minimum duration to receive the interest payment, in MIP, the payment of the interest is done monthly.

Additionally, as MIPs are mutual funds so they do not provide a guarantee of monthly returns and have the risk of investment. It is because when the principal amount is reinvested at the end of the existing MIP, the interest rate may change. Further, as MIPs are not linked to the market, the principal invested amount does not fluctuate.

According to SEBI guidelines, MIPS are denoted as conservative hybrid funds. They generally invest in:

Here, the debt portion aims for stability, and equity tries to increase the returns. Further, like a monthly salary, MIP offers a feeling of regular income, which people are used to. These are suitable options for conservative investors and NRIs looking for moderate returns with fewer risks compared to pure equity funds.

This was all about monthly income plans for NRIs. Moving ahead, now let's know what SWPs are.

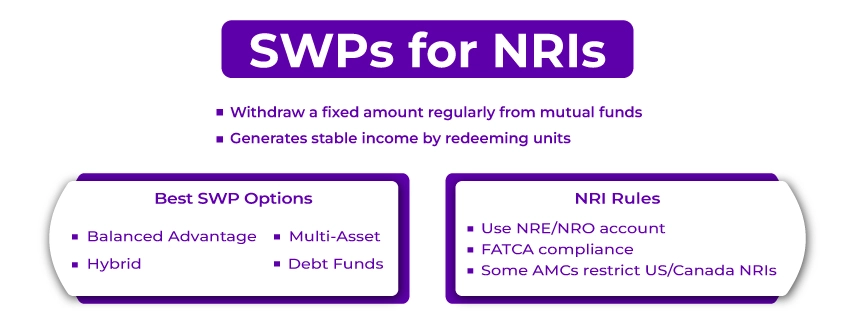

Systematic Withdrawal Plan (SWP), also known as SWP. It is a type of plan that allows you to withdraw incremental or fixed amounts at chosen regular intervals, i.e., quarterly, monthly, or annually, while investing in mutual funds. The SWP is used to create a regular income flow from investments. Further, to generate the desired cash flow, at the selected intervals, you will be redeeming units of the mutual fund.

Further, let's know which mutual funds are the best for SWPs.

Using NRE or NRO Accounts, NRIs can invest in all these categories of mutual funds as per their financial goals, subject to scheme-specific restrictions. Also, NRI investing through SWPs should comply with:

This was all about SWPs for NRIs. Now that you have an understanding of both monthly income plans and SWPs, let's look at the key difference between the plans.

Here is the key difference between monthly income plans and SWPs:

| Basis | Monthly Income Plans (MIP) | Systematic Withdrawal Plan (SWPs) | For NRIs |

|---|---|---|---|

| Income Predictability | Dividends on MIP depend on the fund house's discretion and fund performance. For instance, in one quarter it could be INR 2,000, in the next INR 1,500, and the quarter after it zero. | In the SWP, you can decide on the withdrawal amount. For instance, if you decide the withdrawal amount to be INR 10,000 every month, it means regardless of the market conditions, you every month receive INR 10,0000. | For NRIs covering their EMIs or supporting their family in India, this income predictability is valuable. In this, SWP is the correct option to opt for a regular income. |

| Control and Flexibility | Due to the fixed scheme structure, in MIP, there is limited flexibility. | In SWP, there is total control over the withdrawal amount. Whether you want to decrease, increase, or pause it for a few months, you can do so. | Living overseas means life throws curveballs. For instance, you may receive a bonus, and for six months, you do not need withdrawals from SWP; you can stop it. Further, during an emergency, you need a larger withdrawal amount. Through SWP, you can do so, while MIP does not allow this. |

| Taxation Structure | Income is often taxed on the received dividend/ interest. Additionally, TDS is generally high due to NRI rules. | Tax is only imposed on the capital gain amount. Additionally, for long-term SWPs, tax is often more tax-efficient. | In terms of taxation, SWP is also a better investment choice for NRIs compared to MIP. |

| Income Reliability | It depends on the performance of the scheme and the AMC payout policy. | In SWP, income is highly reliable as investors always preset the withdrawal amount. | From the perspective of income reliability, compared to MIP, SWP is a better investment option for NRIs. |

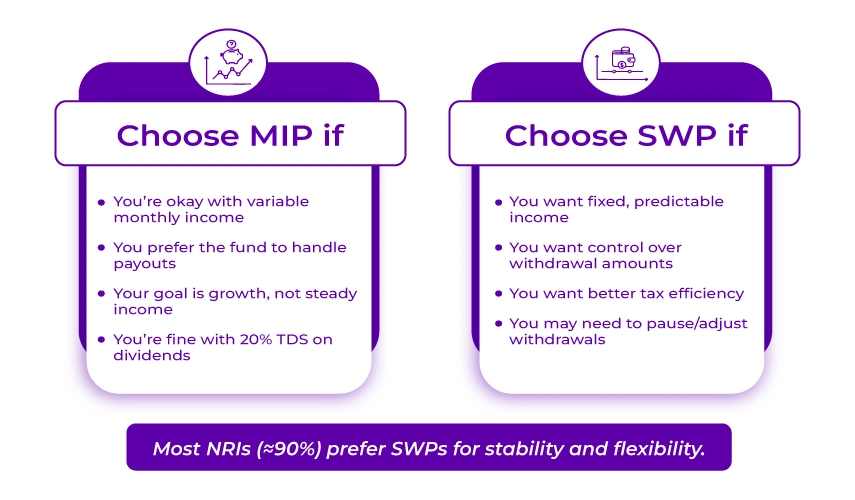

So, from the above monthly income plans vs SWPs, compared to MIP, SWP provides more benefits to NRIs. However, for NRIs who are looking for a basic income option with variable payouts, the MIP is a good investment option. Whereas, for NRIs seeking customizable, consistent, and tax-efficient income, no doubt SWP is the right option to choose.

Moving ahead, let's look at the tax perspective of both investments for NRIs.

Here is how monthly income plans and SWPs of NRIs are taxed in India.

Before April 2020, for investors, there was no taxation imposed on MIP dividends. However, fund houses were liable to pay the Dividend Distribution Tax (DDT) of ~29%. Further, since April 2020, dividends have been added to income, and now they are taxed according to the income slab rate of the individuals. Considering this, for NRIs:

We are a professionally managed company with experience in NRI and cross-border taxation.

The tax on SWP for NRIs depends on the capital gains received by the individual. In this, the best thing is that tax is imposed on the capital gains portion of your withdrawal, not on the complete amount. Confused, let's understand this with an example.

For instance, you have invested INR 10,00,000 in a debt fund, and after 2 years, the value of it is INR 11,05,000. Now, from that amount, you withdraw INR 50,000. Here, your withdrawal has two components:

Further, let's know the NRI taxation on mutual funds:

On MIP and SWP, the TDS rules for NRIs differ significantly:

This is how NRIs pay taxes on MIP and SWP in India. Here, the difference between the two income plans is that, on SWPs, TDS is imposed on the gains amount. Additionally, under this, NRIs can more effectively use the DTAA benefits.

Now, moving further, let's know in the monthly income plan vs SWPs, which plan should NRIs choose?

Opting between the monthly income plans for NRIs and SWPs for NRIs is not about which investment product is good universally. It is about which investment plans match your financial goals, tax profile, and risk appetite. Considering this, let's make this deed simple:

Lastly, between monthly income plans vs SWPs, it is clear that SWPs are a better regular income plan compared to MIPs for NRIs. It is because although MIPs offer a monthly income, but do not guarantee it. However, SWPs, on the other hand, provide NRIs with the predictability, tax efficiency, and control of the withdrawal amount. Further, your investment decision totally depends on your financial goals, life stage, and risk tolerance.

Need assistance in choosing the right investment option in India for NRIs? Connect with Savetaxs. We have a team of financial experts who guide you in opting for the right investment as per your financial goals and tax profile in India.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Shubham Jain is the Founder of SaveTaxs and has extensive experience in Indian and NRI taxation. He advises individuals, NRIs, and businesses on tax filing, tax planning, capital gains, DTAA benefits, fund repatriation, and compliance matters. He regularly writes about taxation and related financial topics. His focus is on making complex tax concepts easy to understand. Through his articles, he helps taxpayers stay informed, avoid common mistakes, and stay compliant with Indian tax laws. See Full Bio

Want to read more? Explore Blogs

_1781845771869.webp&w=828&q=75)

_1778936280179.webp&w=828&q=75)

_1778936089630.webp&w=828&q=75)