Investment & Financial Planning

FCNR Deposit Interest Rates in 2026FCNR Deposit Interest Rates in 2026

Written by Hatim Dudhiyawala

Investing in mutual funds can be a profitable route for Non-Resident Indians (NRIs) looking to grow their wealth while maintaining ties to the Indian financial market. A mutual fund collects money from many investors to invest in various assets like stocks, bonds, and other financial products.

An NRI can invest in mutual funds in India through an NRE (Non-Resident External) and NRO (Non-Resident Ordinary) account. They need an active bank account and a completed KYC to proceed further with NRI investing in mutual funds in India.

NRIs are subject to specific tax rates on gains from Indian mutual funds, which may vary depending on the type of fund and holding period. Additionally, the TDS (Tax Deducted at Source) is mandatory on redemptions for NRIs.

In this blog, we will help you understand how NRIs are taxed on mutual fund gains and the steps to get started with this investment option.

A mutual fund is a collection of money that collects money from many investors and invests in several bonds, stocks, assets, and other money market instruments. It is managed by a professional fund manager who makes the decisions related to investment based on the fund's objectives. The investment made in a mutual fund is not a single share but several shares. It might not necessarily be shares and could be either bonds or other securities as well.

An NRI can also invest in a mutual fund, for which they need to open an NRE (Non-Resident External), an NRO (Non-Resident Ordinary), or an FCNR (Foreign Currency Non-Resident) account.

Additionally, NRIs from the US and Canada may face some restrictions from mutual fund houses due to compliance obligations related to the FATCA (Foreign Account Tax Compliance Act).

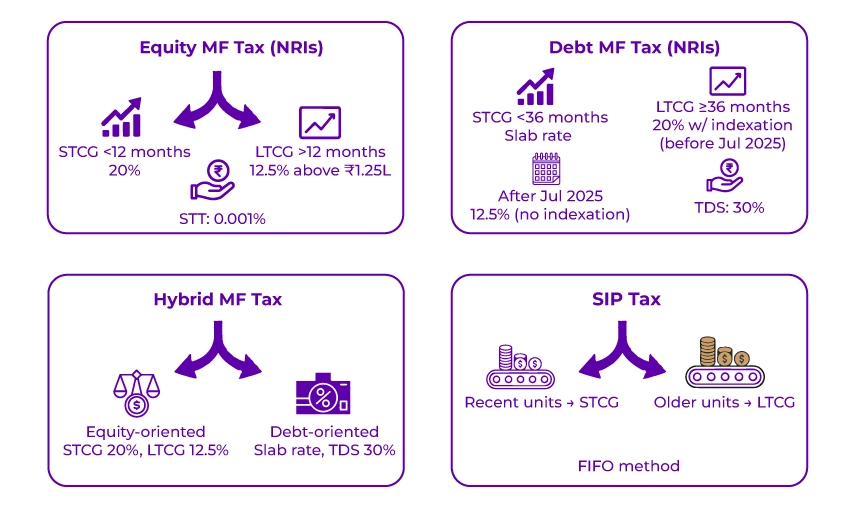

A mutual fund investment scheme must invest at least 65% of its portfolio in domestic equities to be classified as an equity fund. Here is how equity mutual funds will be taxable for NRIs:

Your overall taxable income also includes capital gains from mutual funds. These are taxed as per your applicable income tax slab rate. Debt mutual funds are those that have less than 35% equity exposure. Here is how it is taxed:

File Your NRI ITR with confidence and an expert-backed approach at Savetaxs.

Hybrid mutual fund gains for NRIs are taxed based on the fund's equity allocation: equity-oriented or debt-oriented.

For example, you invested Rs. 10 lakh in an aggressive hybrid fund, and you redeemed it for Rs. 13 lakh after 18 months (Rs. 3 lakh gain). The first Rs. 1.25 lakh gain will be exempt from taxation, and the remaining Rs. 1.75 lakh gain will be taxed at a rate of 12.5%. Overall, the amount would be Rs. 21,875 tax.

All gains are subject to taxation as per your income tax slab rate, regardless of the holding period.

When redeemed, TDS is deducted at a rate of 30% for NRIs as per the Income Tax Act Section 195. Additionally, if your actual tax liability is lower, you are eligible to claim a refund when filing your ITR (Income Tax Returns).

SIPs (Systematic Investment Plan) permit investors to invest a fixed amount regularly in mutual funds. For NRIs, SIP gains are taxed based on the type of mutual fund (equity or debt) and the holding period of each SIP installment. An investor can choose when to invest, like weekly, monthly, quarterly, biannually, or annually.

When you choose SIPs to invest in a mutual fund, you purchase a fixed number of units with each instalment. Additionally, for unit redemption, there is a first-in-first-out (FIFO) concept. The First in, First out method is the standard and legally required concept for calculating capital gains and associated tax obligations.

For example, if you invest in an equity fund via SIPs for one year and redeem the investment later after 13 months, then:

When redeeming mutual funds, NRIs are subject to TDS (Tax Deducted at Source) as per the specific TDS rate determined by the type of scheme (equity or non-equity) and the duration for which the funds were held. Here is how these are classified as either short-term or long-term gains:

| Particulars | TDS on Short-Term Capital Gains | TDS on Long-Term Capital Gains | TDS on Distributed Income Under IDCW Option |

|---|---|---|---|

| Equity Mutual Funds | 15% | 10% | 20% |

| Other than the Equity-Oriented Fund | 30% |

Listed: 20% with indexation. |

20% |

If the NRI falls under a lower tax slab, TDS is charged at the highest applicable rate. However, they can claim a refund when filing their returns.

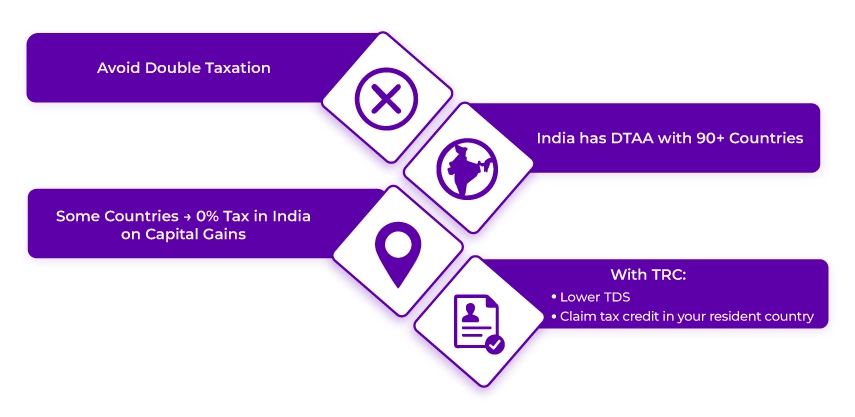

The issue of being taxed twice in India and your country of residency might stress you out. However, this is when the Double Taxation Avoidance Agreement (DTAA) helps. India has signed the DTAA agreement with over 90 countries.

DTAA is a treaty signed between two nations to prevent double taxation of the same income in two different nations for residents. Under the DTAA, gains received from investments made in India are taxed only in one nation, based on the terms of the agreement.

The main provision that permits this tax exemption is called the 'residual clause' in Article 13 of certain DTAAs. Under this clause, capital gains are subject to taxation only in the country of residence of the seller. It means you could potentially enjoy zero tax liability on mutual fund gains in India if you are a tax resident of a country like the Netherlands, Spain, Mauritius, Singapore, the UAE, or Portugal.

By submitting a Tax Residency Certificate (TRC), you can either:

Get customized assistance to understand and comply with all your NRI tax obligations.

NRIs who invest in Indian mutual funds have the option to repatriate their funds to their country of residence. However, repatriation is subject to compliance with the FEMA (Foreign Exchange Management Act) regulations and special guidelines issued by the RBI (Reserve Bank of India). Here are the repatriation limits based on the type of bank account used to invest:

An NRI Investing in mutual funds involves understanding specific tax rules and regulations. You can benefit from these investment opportunities effectively by using the right accounts and following the accurate process. It will help you diversify your portfolio, get access to India's high-growth potential economy, and have a regulated investment process.

Additionally, to improve your investment strategies and ensure compliance with Indian tax laws and international regulations, it's advisable to consult a tax expert. Talking about experts and Savetaxs tops the list. We have a team of experts who assist NRIs in managing their tax obligations and financial planning. They can ensure that you stay informed of your residency status and tax obligations associated with it. Contact us right away and avoid facing any penalties or legal repercussions due to non-compliance.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Shubham Jain is the Founder of SaveTaxs and has extensive experience in Indian and NRI taxation. He advises individuals, NRIs, and businesses on tax filing, tax planning, capital gains, DTAA benefits, fund repatriation, and compliance matters. He regularly writes about taxation and related financial topics. His focus is on making complex tax concepts easy to understand. Through his articles, he helps taxpayers stay informed, avoid common mistakes, and stay compliant with Indian tax laws. See Full Bio

Want to read more? Explore Blogs

_1781845771869.webp&w=828&q=75)

_1778936280179.webp&w=828&q=75)

_1778936089630.webp&w=828&q=75)