Investment & Financial Planning

FCNR Deposit Interest Rates in 2026FCNR Deposit Interest Rates in 2026

Written by Hatim Dudhiyawala

Whether you are an NRI or an Indian resident, selecting where to invest your money is not only about numbers. It is personal and driven by hopes for safety, security, growth, and a better future. In this regard, mutual funds and REITs are among the most important and mainstream investment options, offering significant returns.

However, in the REITs vs. mutual funds comparison, opting for the better option depends on your personal preferences, financial goals, and risk tolerance. Further, to assist you in determining which is the better investment option for NRI between REITs and mutual funds, let's first know what they are.

REITs stand for Real Estate Investment Trusts. It is a company that owns, finances, or operates income-generating real estate. These may include shopping malls, self-storage facilities, buildings, hotels, apartments, resorts, warehouses, and loans or mortgages.

Unlike other real estate companies, it does not develop any real estate property to resell it. Instead, it primarily purchases and develops properties to operate them as part of its own investment portfolio. Further, REITs are traded on stock exchanges and purchased and sold like stocks.

This was all about REITs. Moving ahead, let's know the benefits it offers to NRIs.

Here are the following benefits for NRIs investing in REITs:

These were some of the benefits that REITs offer to NRIs. Moving further, now let's know what mutual funds are.

Connect with us, simply file your taxes, and maximize your tax refunds.

A mutual fund is an investment platform that pools money from several investors and invests it in different financial securities like stocks, money market instruments, shares, gold, bonds, and more.

These are operated by investment professionals who issue these funds to earn Capital Gains or revenue for the investors. As an outcome, each shareholder evenly participates in the profit or loss of the funds.

So, this is what mutual funds are. Moving ahead, let's look at the benefits NRIs get from these investments.

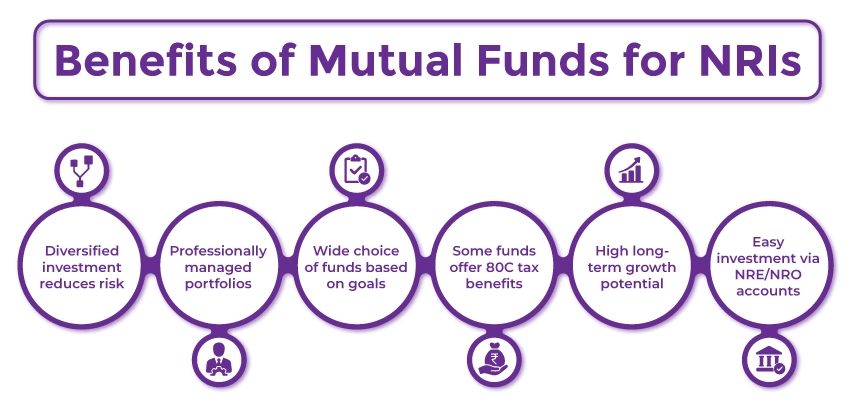

The benefits of mutual funds for NRIs are as follows:

These were the key benefits of mutual funds for NRIs. Now, let's know the key difference between REITs and mutual funds.

The table below showcases the key differences between REITs and mutual funds:

| Features | REITs | Mutual Funds |

|---|---|---|

| Diversification | Only offers investment in real estate. | Provide investment options across several sectors, assets, and regions. |

| Income Potential | Price appreciation + regular dividends | Price appreciation + dividends |

| Liquidity | Very high | High (on-demand redeemable) |

| Growth Potential | Moderate | High |

| Risk | Sector-specific risk | Diversified, lower risk |

| Tax Implications | Dividend income is taxable as per the income tax slab rates; capital gains are taxed as per long-term/ short-term capital gains tax. | Capital gains and dividends are taxed according to the taxation rules of mutual funds. |

| Ease of Investment | Needs DEMAT account | Investment can be made through an NRO/ NRE account |

| Income Distribution | Rent/interest is taxed at 5%. Additionally, on 10%+ on dividends. | Generally, the dividend income earned from mutual funds is taxable. Considering this, 20% TDS is charged for NRIs on dividends. |

| Transparency | With regular disclosure, high transparency. |

With regular disclosures and NAV updates, high transparency. |

| TDS Deduction | Applies to capital gains/ distributions for NRIs. | Applies to dividends/ redemptions for NRIs. |

| Management Style | Managed by professional real estate managers. | Managed by fund managers with expertise in the real estate sector stocks. |

| Entry/ Exit Load | Need to pay brokerage fees and other transaction costs. | Depending on the fund house, it may include an entry/exit load. |

These were the key differences between REITs and mutual funds. Moving further, let's know how NRIs are taxed on REITS and mutual fund investments.

Here, the table below showcases a detailed comparison of REITs and mutual funds taxation for NRIs:

| Features | REITs (for NRIs) | Mutual Funds for NRIs |

|---|---|---|

| Nature of Income | REITs distribute rent, dividends, and interest. Considering this, rent/ interest is generally taxable, and dividends, depending on the underlying SPVs, may or may not be taxable. | From debt schemes and equity, mutual funds generate capital gains and dividends. For NRIs, dividends are taxable. |

| TDS on Income | 5% on interest, 10%+ on dividends depending on rules. Further, TDS also imposes on rent distribution. | 20% imposed on dividends. Additionally, at applicable rates, TDS is also charged on capital gains. |

| Capital Gains Type | Gains generated from selling REITs | Gains earned on the sale/ redemption of mutual fund units. |

| Short-Term Capital Gain Holding Period | <=24 months | Equity: <12 months |

| Long-Term Capital Gain Holding Period | Investments held more than 24 months qualify as LTCG. | Equity Funds: >12 months |

| Debt | 20% with indexation | |

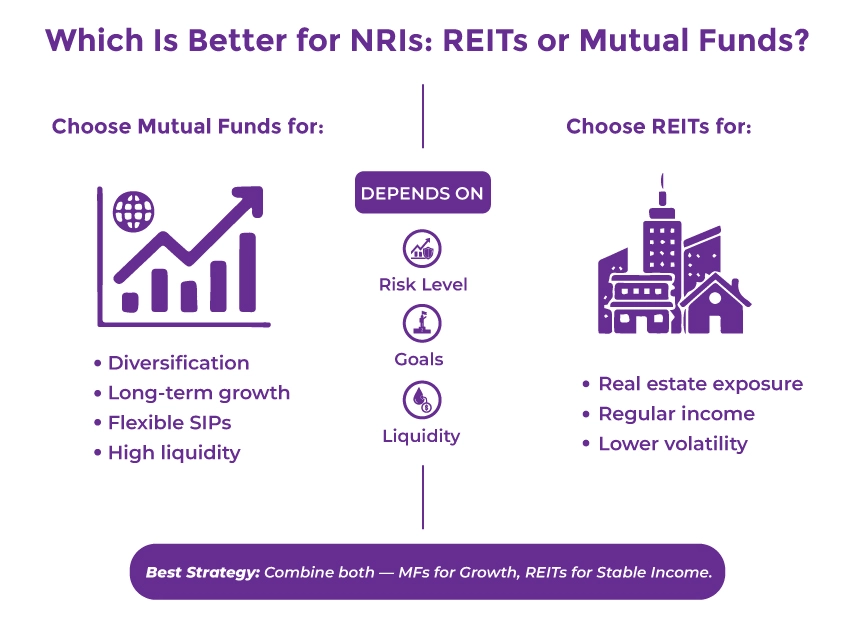

This is how tax is imposed on REITs and mutual funds for NRIs. Moving ahead, now, let's consider the two, i.e., REITs and mutual funds, the better investment option for NRIs.

The investment option for NRIs among REITs and mutual funds depends on their risk tolerance, specific financial goals, liquidity needs, and time horizon. Considering this, mutual funds offer greater flexibility and diversification. Whereas REITs provide a more consistent stream of income with exposure to the real estate sector.

Further, let's know the situations where mutual funds and REITs are better for you.

Further, many financial experts advise a combination of both REITs and mutual funds to build a diversified and resilient portfolio. In this, mutual funds offer liquidity and growth, and REITs provide stable, real estate-associated income.

Our experts will resolve all your queries and guide you with the available NRI banking services in India.

Lastly, both REITs and mutual funds are the best investment options for NRIs in India. Both investments play a key role in NRI financial planning in India. Choosing between the two totally depends on your financial goals, risk tolerance, liquidity needs, and growth potential.

Further, if you need assistance for tax planning in India or require consultancy for banking services, connect with Savetaxs. We have years of experience in the cross-border taxation field. Additionally, we offer personalized solutions as per your financial needs. So, contact us and make your tax journey smooth in India.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Shubham Jain is the Founder of SaveTaxs and has extensive experience in Indian and NRI taxation. He advises individuals, NRIs, and businesses on tax filing, tax planning, capital gains, DTAA benefits, fund repatriation, and compliance matters. He regularly writes about taxation and related financial topics. His focus is on making complex tax concepts easy to understand. Through his articles, he helps taxpayers stay informed, avoid common mistakes, and stay compliant with Indian tax laws. See Full Bio

Want to read more? Explore Blogs

_1781845771869.webp&w=828&q=75)

_1778936280179.webp&w=828&q=75)

_1778936089630.webp&w=828&q=75)