_1784547039242.webp&w=828&q=75)

NRI Income Tax Compliance

30+ Important Income Tax Terms in India You Need to Know30+ Important Income Tax Terms in India You Need to Know

Written by Shubham Jain

For NRIs, the risk of being taxed twice on the same income source is real. However, this risk is mitigated by the network of tax treaties, also known as the Double Taxation Avoidance Agreement, that India has signed with 90+ countries.

The key function of DTAA is to avoid double taxation, help NRIs claim foreign tax credits, and reduce withholding tax rates. Now, the benefits of DTAA aren't automatic; you have to claim them by getting the documentation right and within the appropriate time frame.

This is where many NRIs end up making DTAA claim mistakes. These mistakes are primarily due to a lack of awareness of the compels tax rules, incorrect residency status, and failure to file the appropriate forms to claim DTAA on time.

In this blog, we will discuss common DTAA claim mistakes NRIs make and how to avoid them.

Making DTAA mistakes is not only because NRIs fail to understand the tax laws. It also happens because the entire DTAA claiming process is riddled with loopholes. And to identify these loopholes, you have to be quite mindful, which is why NRIs often seek help from NRI taxation experts with their DTAA process.

And these DTAA mistakes end up costing NRIs, on average, between 15,000 and a lakh of excess tax payments annually.

But not anymore, we will tell you the top seven mistakes that NRIs often end up making, so you don't land in the same place.

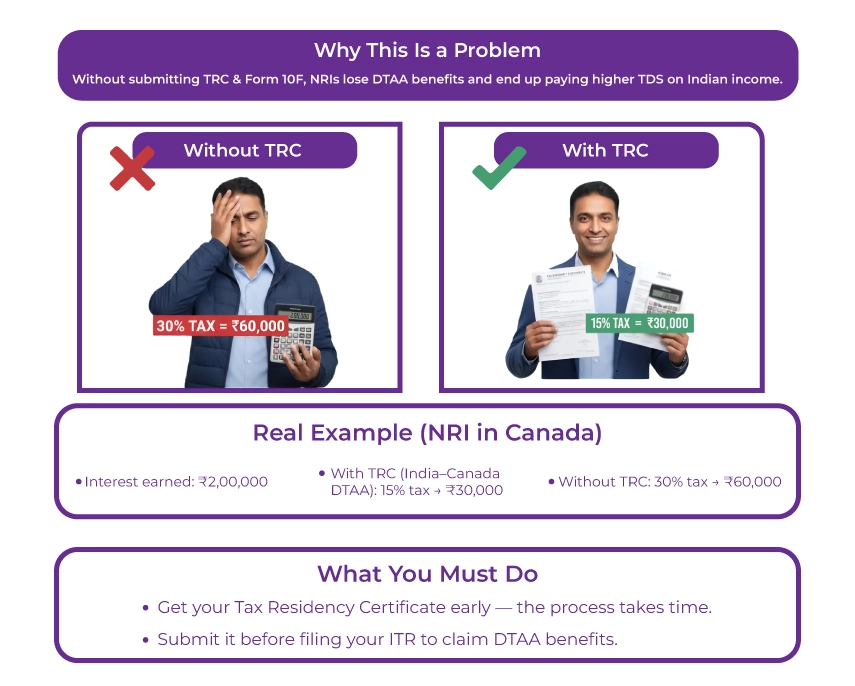

The problem is that if NRIs fail to submit Form 10F and the Tax Residency Certificate (TRC) within the applicable time frame, they lose DTAA benefits and ultimately face higher tax rates in India.

For example, Mr Jayesh, an NRI living in Canada, earned Rs 2 lakh in interest from the Indian fixed deposit. Without TRC, he was liable to pay 30% of the tax, which is Rs 60,000. If he had provided the TRC under the India-Canada DTAA Tax Treaty, he would have been obligated to pay only 15% of the tax, i.e., Rs 30,000.

Hence, ensure you obtain the tax residency certificate, which proves your country of residence for tax purposes and allows you to leverage the benefits of a DTAA.

Get this certificate, as the process takes time, and please ensure to submit it before filing your ITR.

Filing Form 10F is a pretty simple process, but many NRIs still make errors when filing it, leading to rejection of DTAA benefits.

The standard errors here include:

Example: Mr Seema, an NRI living in the United States, ends up filing Form 67, meant for Indian residents, instead of Form 10F, which is required to claim DTAA benefits.

Now that her DTAA claim has been rejected, she has to pay taxes twice on the same income source.

To avoid this mistake, please be very mindful when filing your forms, as a single mistake can cost you thousands in extra taxes.

If in doubt, seek professional help, as NRI taxation experts will handle the entire documentation for you.

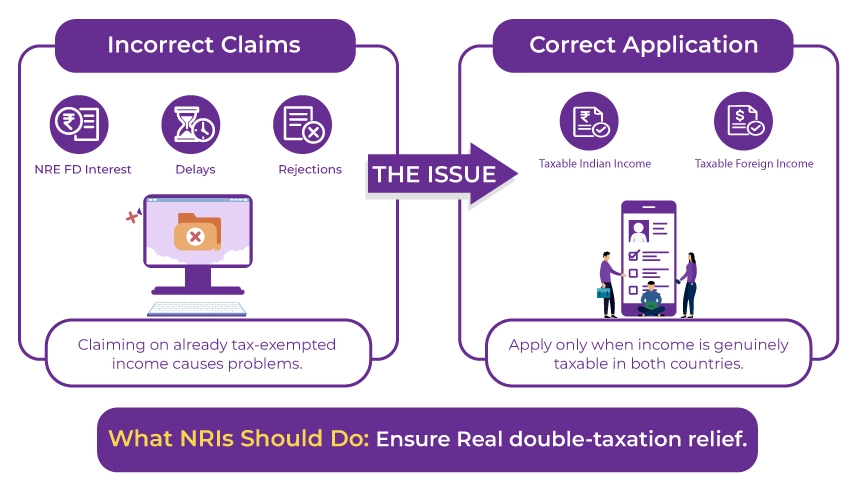

The problem here is that NRIs, at times, file claims for DTAA benefits on income that is already exempt under Indian tax law.

DTAA benefits are meant only for that income source that is taxable for NRIs in both Indian and the NRI's country of residence. Claiming benefits on non-taxable income leads to unnecessary delays, claim rejections, and even scrutiny by the tax department.

Examples for incorrect claims:

Henceforth, NRIs must apply DTAA only when the income is actually taxable in India and also abroad, thereby ensuring the general savings from the avoidance of double taxation.

Filing Form 10F with inaccurate or missing information is like opening the door to penalties, income tax notices, and the possibility of a double taxation avoidance agreement.

Inaccurate filing of the form leads to

To avoid this:

The problem here is that NRIs are unsure of the deadlines and often miss them. Now, missing deadlines means you pay higher taxes.

Timeline Mistakes NRIs Often End Up Making

This is one of the most common DTAA claim mistakes NRIs make: choosing the wrong ITR form. As an NRI, it is essential to know and select the appropriate ITR form based on your income sources and your residential status.

Correct ITR Forms For NRIs

As an NRI, you must never use ITR-1 as it is only for residents.

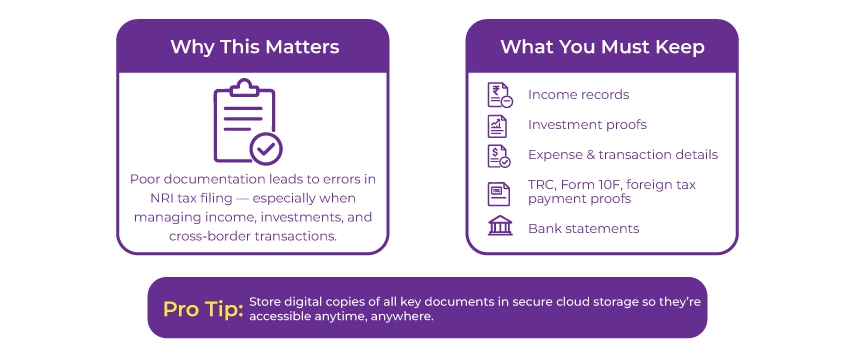

As an NRI managing cross-border finances and taxation, if you don't keep meticulous records of the documents, you are going to make a lot of procedural errors.

Maintaining details and properly documenting is important for NRIs during the tax filing process. Every document, whether your income records, expenses, investments, or other financial transactions, is important.

Here's a tip: Keep digital copies of your TRC, foreign tax payment proof, bank statements, and other related documents in your cloud storage. This ensures your documents are exactly where you are.

As NRI investments in India increase, so does this cross-border taxation. Hence, the DTAA remains the most crucial tool in financial planning for NRIs. To get the most out of the treaty, you need to understand its terms and concepts, get your documents in order, and just be mindful. With all this, you can save a big chunk in taxes as an NRI.

However, it is always advisable for NRIs to consult an NRI taxation professional who is familiar with both Indian and the foreign country's tax laws.

One such expert who can help you with an appropriate DTAA strategy is Savetaxs. We have been assisting NRIs from 90+ countries with their tax filings under their DTAA.

Our experts bring in more than 30 years of experience to the table hence, you can rest assured that your taxes are in the right hands.

Connect with Savetaxs as we serve our clients 24/7 across all time zones.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Shubham Jain is the Founder of SaveTaxs and has extensive experience in Indian and NRI taxation. He advises individuals, NRIs, and businesses on tax filing, tax planning, capital gains, DTAA benefits, fund repatriation, and compliance matters. He regularly writes about taxation and related financial topics. His focus is on making complex tax concepts easy to understand. Through his articles, he helps taxpayers stay informed, avoid common mistakes, and stay compliant with Indian tax laws. See Full Bio

Want to read more? Explore Blogs

_1784546974133.webp&w=828&q=75)

_1784376356528.webp&w=828&q=75)

_1784375756402.webp&w=828&q=75)