_1777957219922.webp&w=828&q=75)

Debt Funds vs Fixed Deposits : What Should NRIs Choose?

Read More

An NRI can make repatriable and non-repatriable investments in India. NRI investors can invest in India on a repatriation basis, meaning they can transfer the proceeds from investments or sales to their country of residence. On the contrary, in the case of non-repatriable investments, the proceeds of the investment or sale cannot be transferred outside India.

Repatriable and non-repatriable are terms that state how and if you can transfer the returns from your investment back to your home country. In this blog, we will learn more about the difference between repatriable and non-repatriable investments for NRIs.

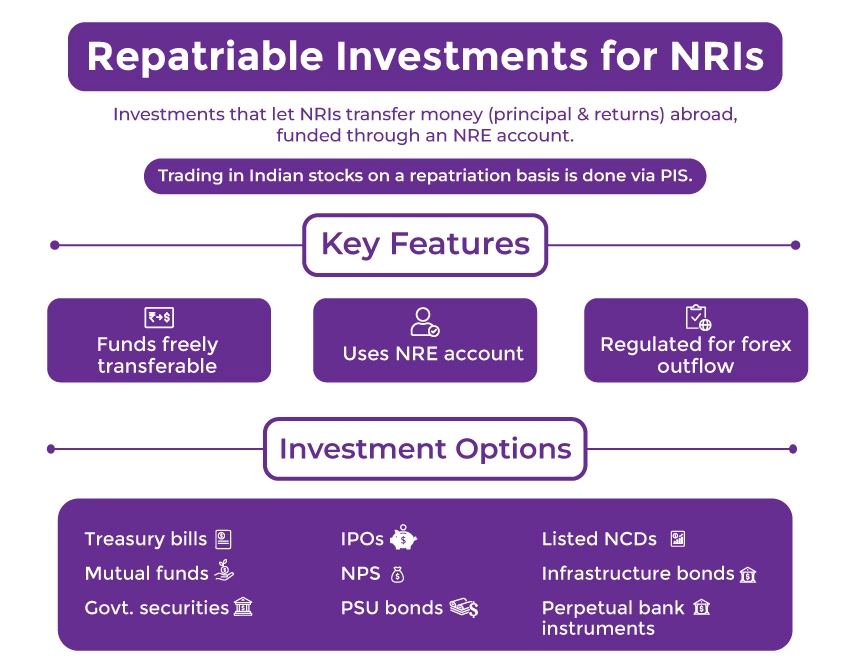

Repatriable investments allow investors to transfer their capital and earnings back to their home country. An NRI can invest in various asset classes in India on a repatriation basis through the funds in their NRE (Non-Resident External) account. NRIs can transfer both the principal amount and the returns earned to their country of residence from these investments, and an NRE account is used for this purpose.

Additionally, NRIs can trade in a recognized Indian stock exchange through PIS on a repatriation basis. PIS (Portfolio Investment Scheme) is an RBI scheme that allows NRIs to invest in the shares of Indian companies by purchasing and selling them using their NRI savings accounts.

Here are some key features of repatriable investment for NRIs:

Investment made using the funds in an NRE account qualifies as a repatriable investment. However, NRIs must use their PIS to invest in Indian equity on a repatriation basis, which requires linking their demat and trading accounts to a PIS-enabled NRE bank account. Such transactions are reported to the RBI. The following are some financial instruments in which an NRI can invest on a repatriation basis:

Get comprehensive support with NRI tax compliance and regulations.

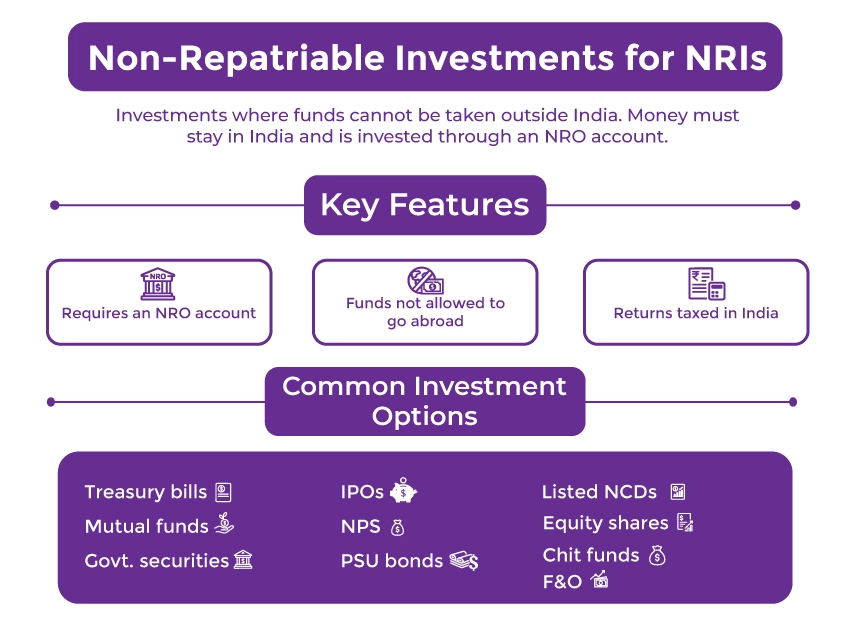

NRI Non-repatriable investments don't allow the transfer of funds outside the country of investment. Funds from these investments must be held within the country where they were earned. Investments made by an NRI in India are treated as domestic investments equivalent to those made by an Indian resident. NRIs can invest in different asset classes in India using their NRO (Non-Resident Ordinary) account. They can use the income earned in India for non-repatriable investments, such as rent, dividends, pension, etc.

Here are some key features of non-repatriable investments in India for NRIs:

Under non-repatriable investments, an NRI faces several restrictions on the transfer of proceeds acquired from the sale or investment. You are not required to seek separate permission from the RBI to trade/invest in Indian equity on a non-repatriable basis until you link your demat and trading account to an NRO account. An NRI can invest in the following financial instruments on a non-repatriation basis:

Get expert NRI financial planning help from Savetaxs.

The key difference between repatriable and non-repatriable investments for NRIs is that repatriable investments allow the investors to transfer both the principal amount and returns to their home country, while NRI non-repatriable investments restrict this transfer. The table below shows the main differences between repatriable and non-repatriable investments in India for NRIs:

| Aspect | Repatriable Investments | Non-Repatriable Investments |

|---|---|---|

| Liquidity and Flexibility | High liquidity and flexibility because you can transfer funds internationally without facing any significant barriers. | Lower liquidity, as funds are held within the local economy. |

| Taxation | Enjoys favourable tax treaties between nations, helping to reduce the tax burden on earnings. | Subject to local taxation, which can be higher and more complex. |

| Account Linked | Linked to an NRE account, which is denominated in foreign currency. | Linked to an NRO account, which is denominated in local currency. |

| Risk Management | Has reduced risk because of currency protection and the benefit of transferring funds in response to economic changes. | Higher risk if the local economy faces instability because you cannot convert them back into your home currency and transfer them out of the host country. |

While repatriable investment offers flexibility and tax benefits, non-repatriable investment offers a financial instrument to manage Indian-sourced income and acquire attractive returns. Consider the following factors when deciding between repatriable and non-repatriable investments for NRIs:

Both repatriable and non-repatriable investments offer various benefits and challenges. Repatriable investments provide the benefit of currency protection and transferring funds internationally. While non-repatriable investments are less flexible but they can be beneficial for those who seek to invest long-term investments within a specific country.

Lastly, before making any decision, it is advised to consult with an expert at Savetaxs to ensure that you make a well-informed choice that aligns with your unique financial situation. We have a team of experts who can offer personalized guidance in navigating everything about repatriable and non-repatriable investments so that you stay compliant. Connect with us right away, as we are working 24*7 across all time zones.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Mr Shaw brings 8 years of experience in auditing and taxation. He has a deep understanding of disciplinary regulations and delivers comprehensive auditing services to businesses and individuals. From financial auditing to tax planning, risk assessment, and financial reporting. Mr Shaw's expertise is impeccable.

Want to read more? Explore Blogs

_1777957047993.png&w=828&q=75)

_1778215729715.webp&w=828&q=75)