Investment & Financial Planning

FCNR Deposit Interest Rates in 2026FCNR Deposit Interest Rates in 2026

Written by Hatim Dudhiyawala

As an NRI living in the USA, you already know the financial maze you are in. From US state laws to federal taxes, investment options, managing cross-border finances, filing taxes, and staying compliant with the FEMA regulatory framework, handling all this is overwhelming. Henceforth, having a solid financial plan will help you navigate this myriad of complexities like a pro.

Whether you are earning dollars or generating income in India, knowing how to balance both worlds will help you ensure a financially sound future. And this is what we will discuss in this blog.

Here we will see how you, as an NRI, can make a financially compliant plan that fits right in your NRI world.

A financial plan is a structured, systematic process for clearly defining your financial life goals. Such as purchasing a property, funding your child's education, supporting your parents living in India, and managing your retirement corpus in the USA, all while mapping your assets and liabilities in both INR and USD.

Additionally, a financial plan involves creating a roadmap for saving, making tax-efficient investments, optimizing your tax strategy, and protecting your wealth by making sound financial decisions.

For NRIs living in the USA, having a financial plan for you all is way more important than ever because you are governed by US rules and regulations on your global income while also being liable for taxes in India on the revenue generated in India. A solid financial plan will help you avoid being taxed twice on the same income source and manage your finances in both countries.

The complexities for NRIs living in the USA don't end here, as the impact of currency fluctuations, varying investment rules for NRIs, and the question of whether to settle in the USA or return to India must also be considered.

But all of these complexities can easily be resolved with a reliable financial plan. Henceforth, the importance of a financial plan for NRIs is that it helps you secure your future in India and the USA.

With Savetaxs, we help you simplify filing NRI Income Tax in India.

As an NRI, you balance the best of both worlds, which is the USA and India, and this duality comes with an array of financial challenges. These challenges can be cross-border taxation, fluctuating exchange rates, and regulatory compliance.

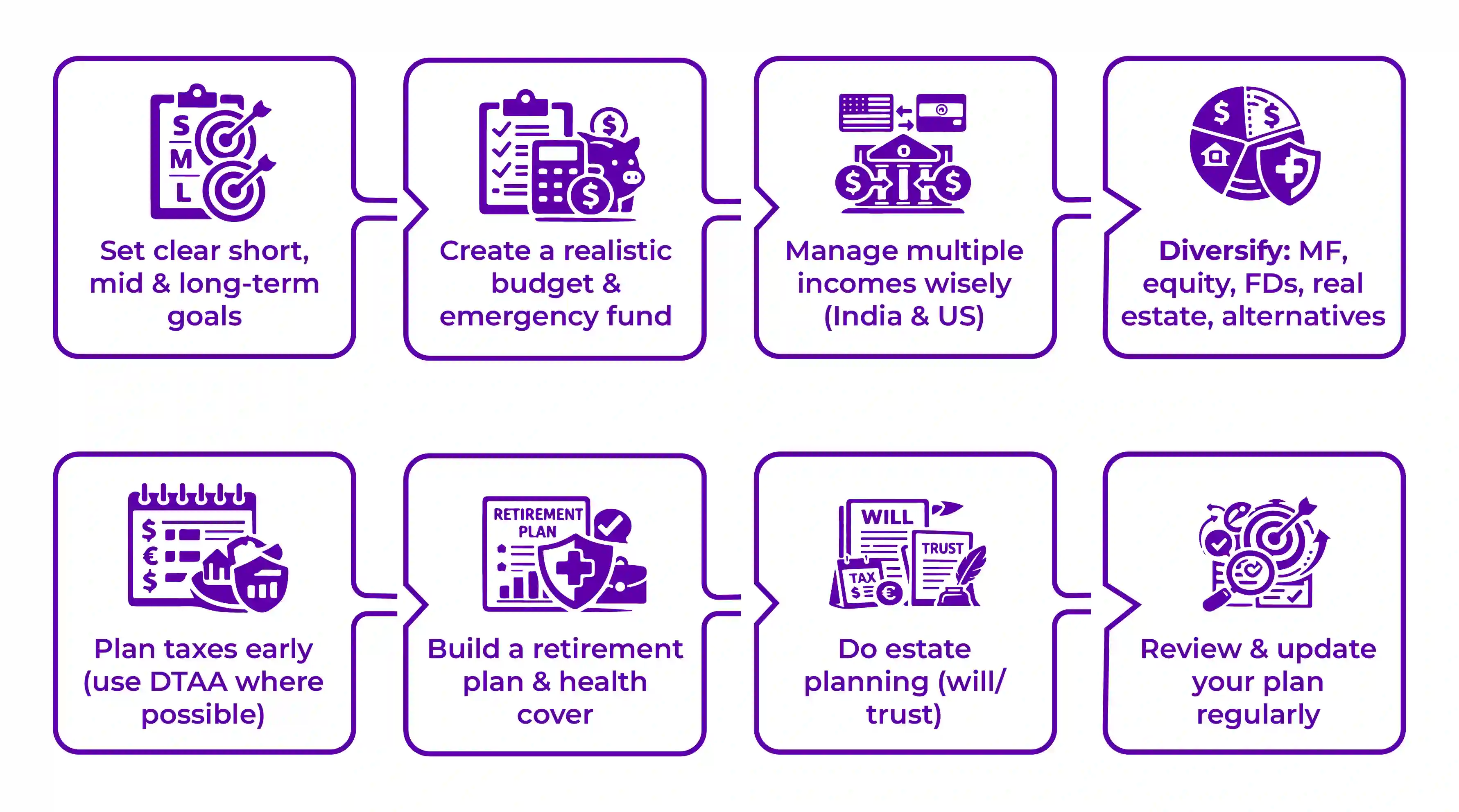

Hence, to help you navigate these economic challenges smoothly, here is a step-by-step method to tailor a financial plan that suits your needs, goals, and stability and safeguards your future wealth.

Setting your life's financial goals clearly is the anchor of your successful financial plan. You must classify your goals into three categories:

This way, you will be able to clearly segregate your goals, which will help you plan more effectively.

Once your goals are clearly defined, you need a budget to bring those goals to life. Hence, planning your budget provides you with a clear picture of your current income, expenses, and savings capacity.

As an NRI, you might have multiple income streams, and managing these effectively is important for optimizing your cash flow and achieving financial stability.

The following are best practices for managing your income.

As we know, diversification is important for minimizing risk and maximizing benefits. The following are the key investment options for NRIs in India to diversify into.

It's better to be proactive than be sorry. As an NRI, managing cross-border tax regulation is important to minimize your tax liabilities and remain compliant with the tax laws.

The following steps outline how to create a proactive, effective tax plan.

Regardless of where any plan is to be, whether in India or the USA, having a sound retirement strategy is essential.

Key Components of Retirement Planning.

NRIs' succession and estate planning ensure that, after you, your wealth is transferred seamlessly across the border, without any legal disputes or tax complications.

For effective succession planning:

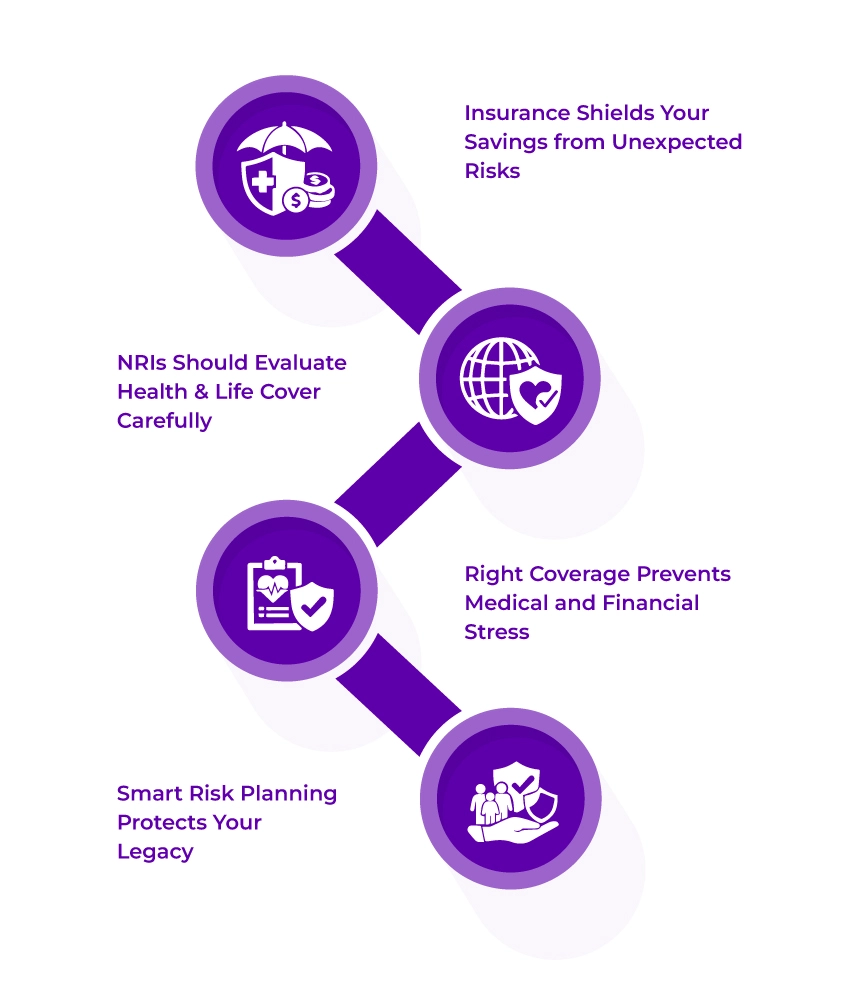

NRIs, you must have adequate insurance to protect you against unforeseen risks in life.

You can opt for

Financial planning for NRIs is an ongoing process that requires you to review your plan annually to stay relevant.

NRI taxation is complicated because you must comply with the tax laws of two countries: India and the USA. The income you earn in India as an NRI is taxable in India. Now, under the US-India double tax avoidance agreement, you can claim relief and legitimately avoid paying tax twice on the same income source.

The India-US taxation treaty sets specific rates: dividends are taxed at 12-25%, interest at 10-15%, and so on. Hence, you must be aware of these rates before you invest. To claim the benefits of the DTAA, NRIs must submit Form 10F and a tax residence certificate from their country of residence.

US Tax Filing: NRIs must report their worldwide income on Form 1040 if they are US tax residents, and nonresident aliens must use Form 1040-NR. For US filing, file your taxes by April 15; however, extensions vary, so don't wait until the last moment.

Indian Tax Filing: In India, how you will be taxed depends entirely on your residence status. File the wrong statutes, and you will end up serving heavy penalties. Indian tax returns are typically due by July 31st.

Also, it's important for NRIs to consult a qualified NRI financial advisor to understand the entire NRI taxation concept in compliance, so that you don't face any legal complications or end up paying more taxes than you should.

Connect with Savetaxs, get expert guidance on crypto taxation, and maximize your refunds.

Wealth creation and traditional investment are two different terms because, in wealth creation, assets are distributed across countries, and future financial goals are split between the US and India.

Here, a balanced approach between the two countries is required to ensure investments are diversified and aligned with long-term objectives. In the US, where building wealth through regulated markets and retirement accounts is common, the NRI benefits from strong global economies and growth opportunities. At the same time, investments in India, be it equity, mutual funds, bonds, or property, must support emotional goals, future relocation plans, and family responsibilities.

Additionally, you must ensure that cross-border investment requires careful planning, as regulations under FEMA, tax differences, repatriation restrictions, and documentation obligations must be understood well in advance of investing.

The cornerstone of financial planning is not just about growing your money, but it's also about protecting it. Having the right insurance and timely risk management ensures that unexpected events do not disrupt your years of savings. NRIs must carefully evaluate their health and life insurance needs depending on their dependents, lifestyle, and income in the United States.

Additionally, having proper medical coverage ensures you don't face financial strain from healthcare costs,

In a nutshell, risk planning and management give you peace of mind and protect your legacy from being destroyed.

Financial planning for NRIs covers all the significant aspects of your life, including personal finances, investments, taxes, retirement estate planning, and more. The importance of having a financial plan for NRIs cannot be understated.

For NRIs, your taxation, investment, repatriation of funds, and inheritance regulations are governed by one or two countries, and having a good NRI compliance financial plan is essential.

However, as an NRI, if you are looking for an expert to strategize your finances for the current financial year, Savetaxs is the name to trust. We have been helping NRIs strategize and curate financial plans to maximize wealth creation, minimize tax liabilities, and ensure economic security for them and their families.

Start your financial planning for NRIs in the USA journey with Savetaxs as we serve our clients 24/7 across all time zones.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Hatim Dudhiyawala is a Certified Public Accountant (CPA) with SaveTaxs and specializes in Indian and NRI taxation. He advises individuals, NRIs, and businesses on income tax filing, capital gains taxation, DTAA benefits, fund repatriation, and tax compliance. With experience in cross-border tax matters, Hatim helps taxpayers understand complex regulations and make informed decisions. Through his articles, he shares practical insights to help readers stay compliant and manage their tax obligations with confidence. See Full Bio

Want to read more? Explore Blogs

_1781845771869.webp&w=828&q=75)

_1778936280179.webp&w=828&q=75)

_1778936089630.webp&w=828&q=75)